Beyond Borders: The ASEAN+3 Blueprint for the Digital Financial Frontier

The global financial landscape is currently navigating a period of profound structural flux, and nowhere is this more evident than in the historic corridors of Osaka, Japan. Recently, this city—long celebrated as a cornerstone of Japanese commerce and culture—played host to a joint seminar convened by the ASEAN+3 Macroeconomic Research Office (AMRO) and the International Monetary Fund (IMF), a strategic summit of the region’s most influential financial architects. Central bankers, senior policy makers, and private sector experts gathered to confront the dualities of digitized money, seeking a path that balances "transformative potential" with the immutable requirements of national stability.

Mr. Kenichi Nishikata, Deputy Vice Minister for the Ministry of Finance of Japan, set a sobering tone for the proceedings. While acknowledging that the advent of tokenized money—specifically central bank digital currencies (CBDCs) and stablecoins—could catalyze regional economic integration, he issued a stark warning regarding the risk of "currency substitution." To illustrate the gravity of this threat to monetary sovereignty, Nishikata employed a striking linguistic metaphor. He compared national currencies to local languages; just as a community that abandons its native tongue for a dominant foreign language finds it nearly impossible to revitalize that extinct speech, a nation that allows its citizens to abandon local tender for foreign-denominated digital assets risks a permanent loss of monetary policy transmission. Once the "language" of a local currency is lost to a dominant digital interloper, the central bank loses its voice in managing the economy.

The consensus emerging from Osaka is defined by a central tension: the region is caught between the drive for deeper financial integration and the existential need for sound governance. As digital payments become faster and more borderless, the risks of money laundering, terrorist financing, and the circumvention of capital flow management measures intensify. The "Osaka Consensus" suggests that while innovation is inevitable, it must be tethered to macroeconomic discipline. This post evaluates whether these innovations represent a genuine paradigm shift for the ASEAN+3 region—an area now accounting for 28% of total global final demand—or merely a high-tech iteration of the legacy risks that have long haunted international finance.

1. The Stablecoin Dilemma: Regulatory Arbitrage and the Race to the Bottom

Stablecoins have made a swift and disruptive transition from the speculative periphery of crypto-trading to the center of the global cross-border payment debate. Originally designed as liquidity "parking spots" for traders, assets like USDT and USDC are now being evaluated as potential instruments for real-world retail and commercial transactions. However, as the IMF’s Tatsuya Sugihara and Professor Kenji Ueda of the University of Tokyo noted, this evolution brings systemic questions to the fore: are stablecoins a true game-changer, or are they simply "old wine in new digital bottles" carrying familiar, unmitigated risks?

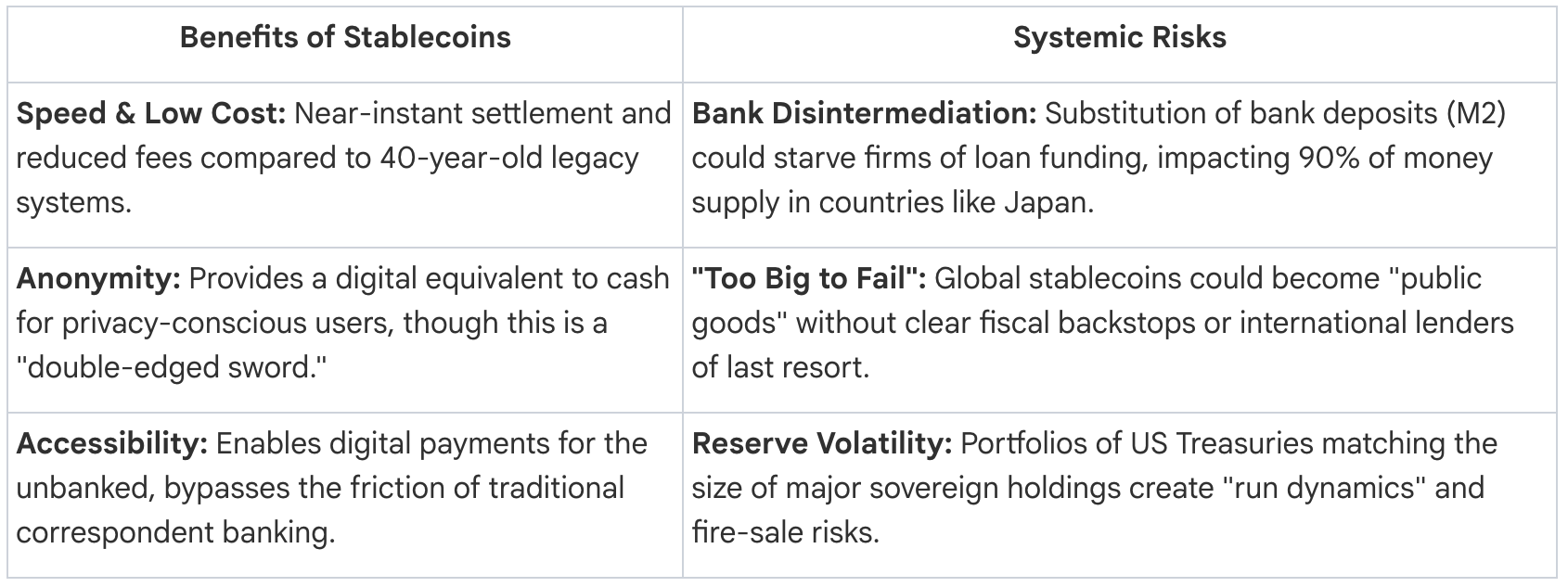

To understand the stakes, we must weigh the immediate efficiencies against the potential for systemic contagion.

Comparison of Stablecoin Dynamics

The most pressing concern for regulators is the "Regulatory Arbitrage" problem identified by Peter Goodrich of the Financial Stability Board (FSB). Because stablecoins are inherently borderless, issuers can easily "pick up and move" to jurisdictions with lighter-touch regulations if they find their home supervisor too stringent. This creates a "race to the bottom," where the global financial system is only as strong as its weakest link. Goodrich revealed a startling lack of progress: in an October 2023 implementation review of 29 jurisdictions, only five had made significant progress on stablecoin frameworks, and only two had fully implemented the FSB’s recommendations.

This fragmentation leads to what Goodrich termed the "multi-jurisdictional issuance problem." A single, fungible token might be issued in the US, Europe, and Japan, appearing identical on the blockchain. However, the regulatory reality is a hodgepodge; different countries may impose conflicting rules regarding redemption periods or the physical location of reserve assets. This makes it nearly impossible for a single national authority to manage liquidity.

The "So What?" for the ASEAN+3 region is profound. Current tools, such as the IOSCO Multilateral Memorandum of Understanding (MMOU), were designed for sharing enforcement data on market abuse, not for the proactive, real-time sharing of supervisory data necessary to maintain global financial stability. Without a harmonized framework, the region remains vulnerable to digital dollarization and capital flights that central banks will be powerless to stop.

2. The Shadows of Digital Cash: P2P Risks and FATF Standards

The evolution of financial crime has kept pace with technological advancement, shifting the focus from physical suitcases of cash to the "unhosted wallets" of the digital age. This shift into the shadows of Peer-to-Peer (P2P) transactions represents a fundamental challenge to the current regulatory framework, which has traditionally relied on intermediaries to act as gatekeepers.

Mr. Takahide Habuchi, representing the Financial Action Task Force (FATF), emphasized that stablecoins, due to their price stability, are far more attractive to criminals, terrorists, and sanction evaders than volatile crypto-assets like Bitcoin. He noted that in spite of our technological prowess, we still don't know the true size of the P2P market—estimates range wildly from 10% to 70% of total transactions. To counter this "black box" of finance, he outlined a multi-layered defense strategy:

- Implementation of the "Travel Rule": Ensuring that the identity of the sender and receiver "travels" with the transaction, preventing anonymous cross-border hops.

- Blockchain Analytics: Leveraging the transparency of the ledger to distinguish between innocent privacy-seekers and illicit actors through network analysis.

- Pre-Launch Controls: Preventing the issuance of assets that do not have "AML/CFT by design" built into their core protocols.

- Smart Contract "Burn and Freeze": Requiring issuers to maintain the technical capability to freeze or destroy tokens held by sanctioned entities, effectively neutralizing the asset.

The FATF philosophy rejects the notion that regulation is a handbrake on growth. Instead, Habuchi argued for "Responsible Innovation," where robust regulation increases industry trust and enhances predictability. By addressing the risks of unhosted wallets before they reach systemic scale, policy makers can ensure that digital cash does not become a permanent sanctuary for the proceeds of crime.

3. The Retail Revolution: QR Codes and the Death of Cash in ASEAN

While the debate over stablecoins remains partly theoretical, a retail revolution is already underway across ASEAN. Real-time payment systems and QR code linkages have entered a "structural growth phase," driven by the region's massive economic footprint. The ASEAN+3 market accounts for 28% of total global final demand—exceeding the US at 26%—with trade nearing 50% of its GDP. Furthermore, Julian Hung of Grab noted that 75-80% of APAC outbound travel stays within the region, creating a massive, captive market for cross-border retail payments.

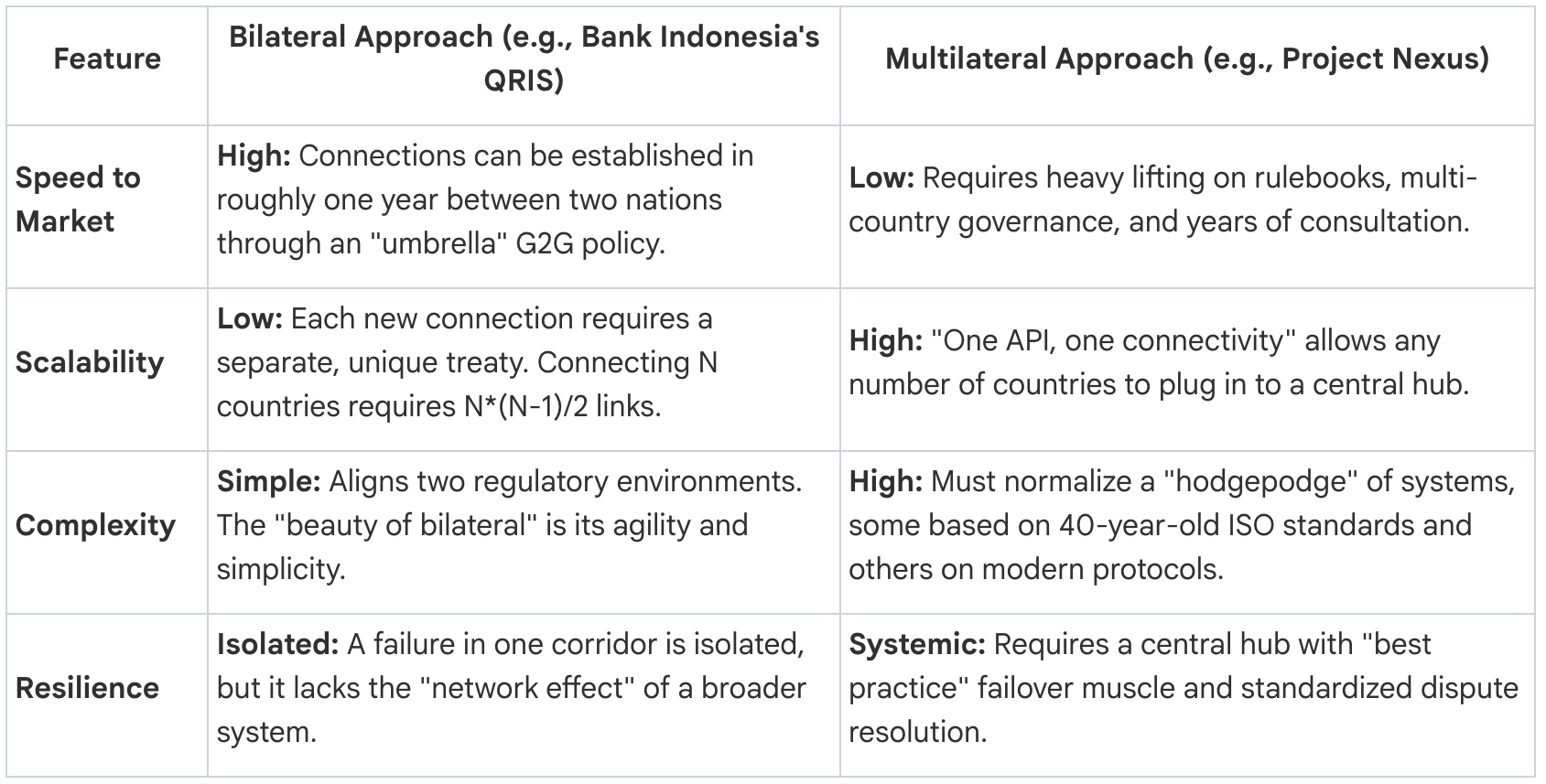

The region currently finds itself at a crossroads between two distinct models of connectivity: the Bilateral and the Multilateral approaches.

Comparison of Payment Connectivity Models

The private sector perspective from Grab underscored the economic impact of these "digital rails." For "micro-merchants" who traditionally could not afford the high Merchant Discount Rates (MDR) of foreign credit cards—which range from 2% to 6%—QR linkages allow them to accept cashless payments from tourists with minimal overhead.

However, technical connectivity is only half the battle. The "So What?" of this revolution lies in the "trust gap." Consumers are hesitant to link their direct bank accounts to a QR code if they lack the fraud protection and chargeback frameworks they enjoy with traditional credit cards. Julian Hung argued that without a robust, standardized rulebook—similar to what Project Nexus aims to provide—technical interoperability will fail to reach mass adoption. People do not want to use a system where they are "one scam away" from an empty bank account.

4. The CBDC Reality Check: Moving from Retail Hype to Wholesale Utility

The initial mania surrounding Central Bank Digital Currencies (CBDCs) is cooling, replaced by a more pragmatic focus on utility. Andrew McCormack, leading Project Nexus, offered a blunt, "skeptical view" on retail CBDCs. He suggested that "reinventing money" is a "strange use of time" and energy when existing fast-payment systems can be upgraded to achieve the same retail goals. For many, the retail CBDC was a "thought exercise" that catalyzed the modernization of traditional rails, but whose actual implementation is fraught with the risk of disintermediating the very banks that fund the economy.

The true frontier, according to the Osaka discussions, is "Wholesale Utility." While retail payments are flashy, the "real elephant in the room" for cross-border finance is FX settlement and the T+2 settlement cycle. Wholesale CBDCs offer a way to settle high-value transactions in real-time, reducing the need for expensive pre-funding.

Furthermore, the "Wholesale Advantage" is a matter of safety. McCormack noted that the "blast radius" of a wholesale settlement system is significantly smaller and more manageable than a retail system involving 30 million merchants and 60 million users. In a wholesale environment, you have a "fighting chance" of reimagining the clearing house without triggering a systemic collapse of consumer trust.

For the private sector, the way forward may be the "Sandwich Model" for tokenized money. As Julian Hung explained, this model allows value to move on-chain "under the hood" for speed and transparency, while users interact with trusted, traditional interfaces like the Grab wallet. This approach provides the benefits of blockchain—speed, programmability, and liquidity—without requiring the consumer to understand the complexities of digital assets, while allowing regulators to maintain strict control over the fiat on- and off-ramps.

5. Conclusion: Navigating the Intersection of Policy and Technology

The overarching takeaway from the AMRO-IMF seminar is that the future of the ASEAN+3 financial ecosystem will not be determined by technology alone, but by the policy choices and international cooperation that surround it. The "Osaka Consensus" acknowledges that the region is a "global incubator" for finance, but warns that innovation without governance is a recipe for instability.

For ASEAN+3 policy makers, the strategic imperatives are clear:

- Sound Macroeconomic Discipline: Strengthening the value and trust of local currencies is the only true defense against digital dollarization and "currency competition" from hard-currency stablecoins.

- Proactive Information Sharing: Moving beyond legacy enforcement frameworks to share real-time supervisory data on financial stability and liquidity risks.

- Public-Private Partnerships: Ensuring that infrastructure like Project Nexus or national QR standards are accessible to both traditional banks and fintech players to level the playing field for micro-merchants.

- Operational Resilience: Developing the "operating muscle" to handle cyber threats and fraud in an instant-payment world where the speed of transactions matches the speed of light.

The ASEAN+3 region is currently crafting the blueprint for the digital financial frontier. By leading the world in QR connectivity and pioneering multilateral settlement rulebooks, the region is moving toward a more integrated, resilient, and inclusive digital ecosystem. The road from Osaka is long, but the direction is set: the future of finance is no longer just digital—it is borderless, and it is being built in Asia.