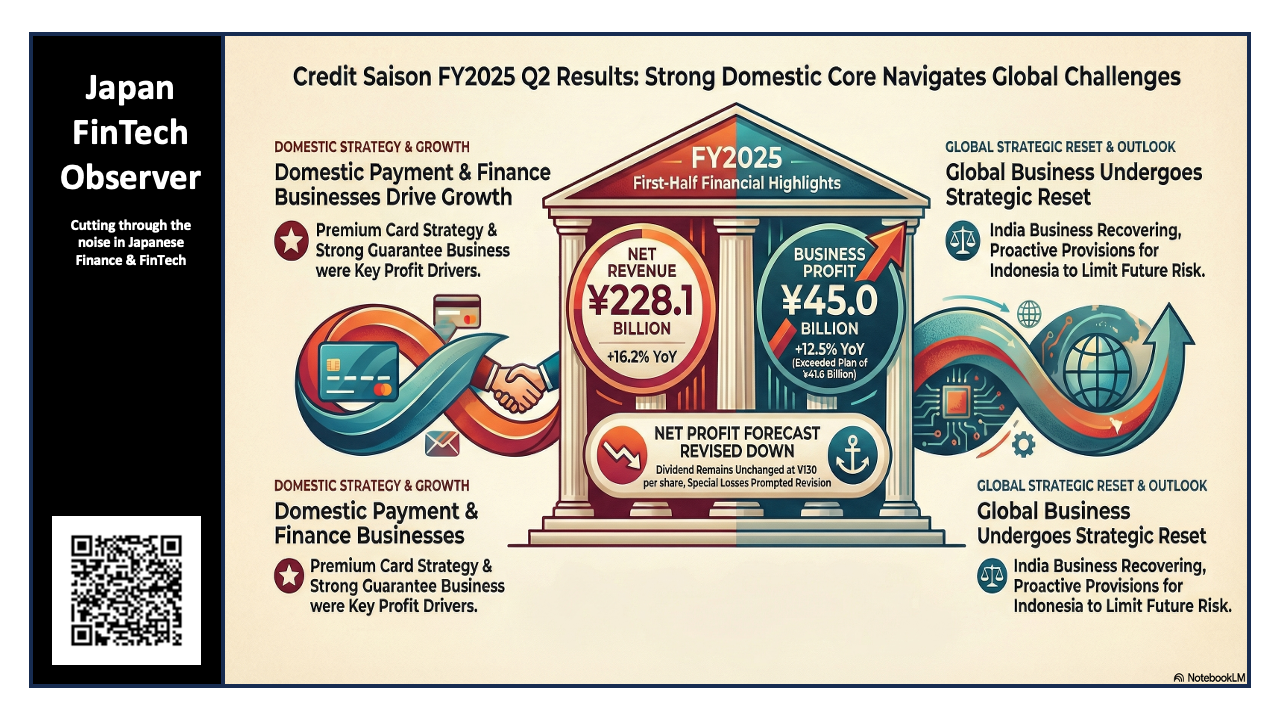

Credit Saison Second Quarter Financial Results

Credit Saison's financial results for the first half of fiscal year 2025 (H1 FY25) present a dual narrative that is crucial for investors to understand. On one hand, the company's core domestic operations demonstrated remarkable strength, driving business profit well beyond internal targets. On the other hand, a series of special, non-recurring losses weighed on the bottom line, resulting in a slight year-on-year decline in net profit attributable to shareholders. This divergence underscores the resilience of the underlying business while highlighting the impact of discrete strategic decisions and market-specific challenges.

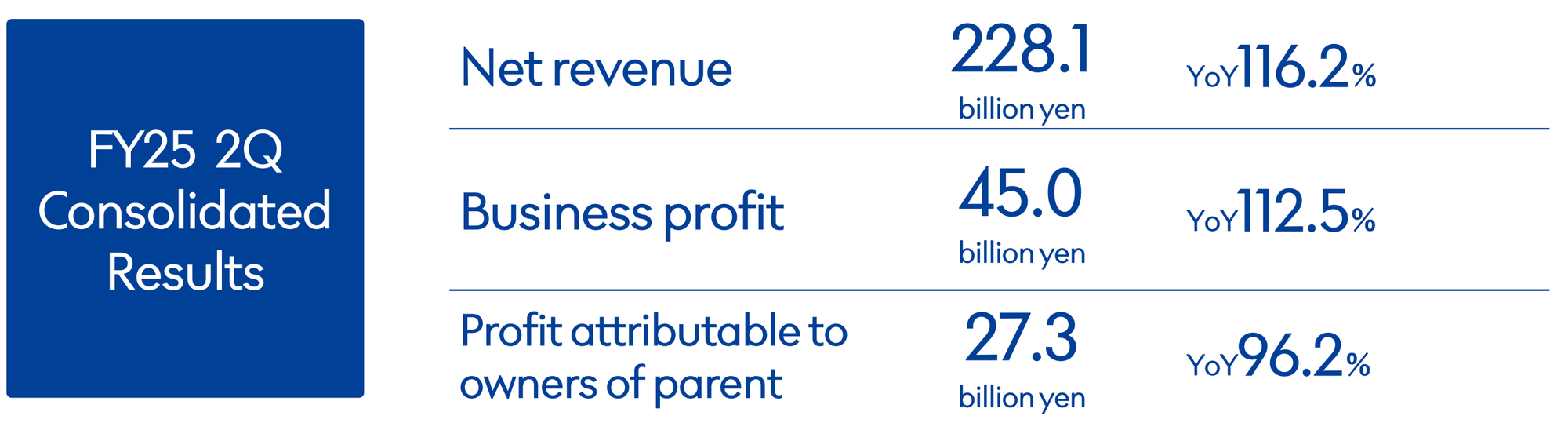

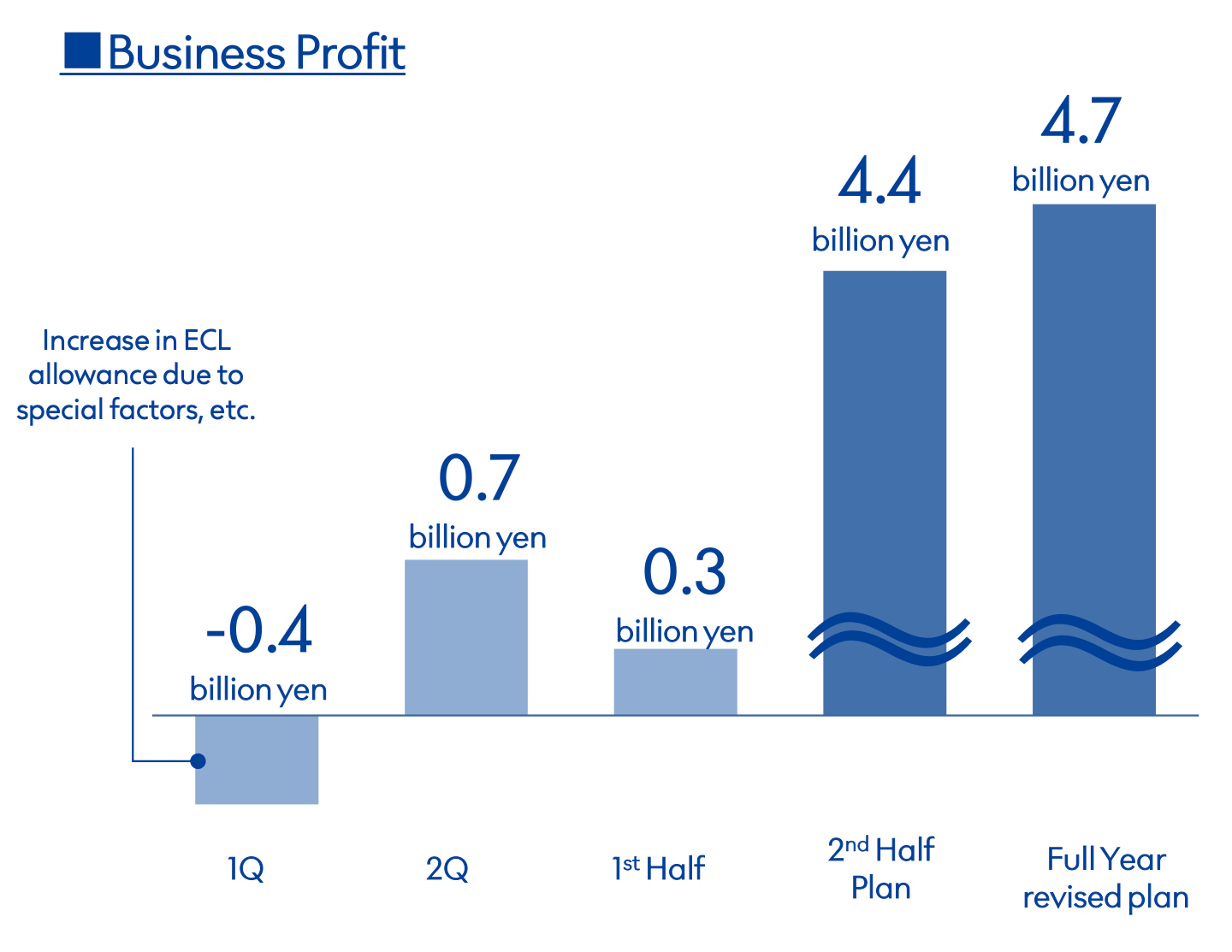

For the six months ended September 30, 2025, Credit Saison reported robust top-line growth and a significant increase in business profit, a key metric for measuring the performance of its ordinary operations. However, this strength was not fully reflected in the final net profit figure due to the aforementioned special items.

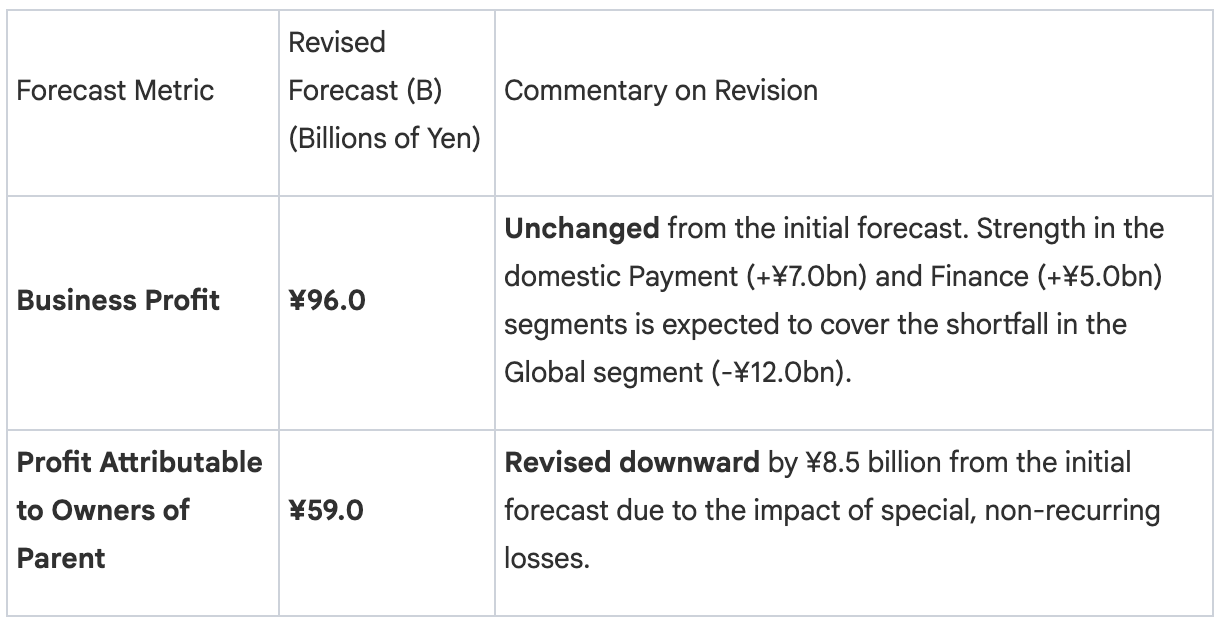

The 12.5% YoY growth in Business Profit was a standout achievement, exceeding the company's internal plan of approximately ¥41.0 billion. This outperformance was fueled by the exceptional results within the domestic Payment and Finance segments. In stark contrast, the 3.8% decline in Profit Attributable to Owners of Parent was a direct consequence of special losses that were not factored into the initial forecast. These primarily included a loss on the sale of shares in affiliated companies recognized in the first half, as well as planned losses associated with the strategic withdrawal from the amusement business operated by subsidiary Concerto.

This high-level overview necessitates a more granular examination of the individual business segments to fully appreciate the sources of strength that are sustaining the company's profitability and to understand the nature of the challenges it is actively managing.

Domestic Business Segments: The Engine of Profitability

Credit Saison's domestic Payment and Finance segments serve as the foundational engine of its current financial strength. The robust, double-digit profit growth in these core businesses provides the stability and financial capacity for the company to navigate temporary challenges in other areas, most notably its Global business. Their consistent performance validates key strategic initiatives and reinforces their role as the primary drivers of shareholder value.

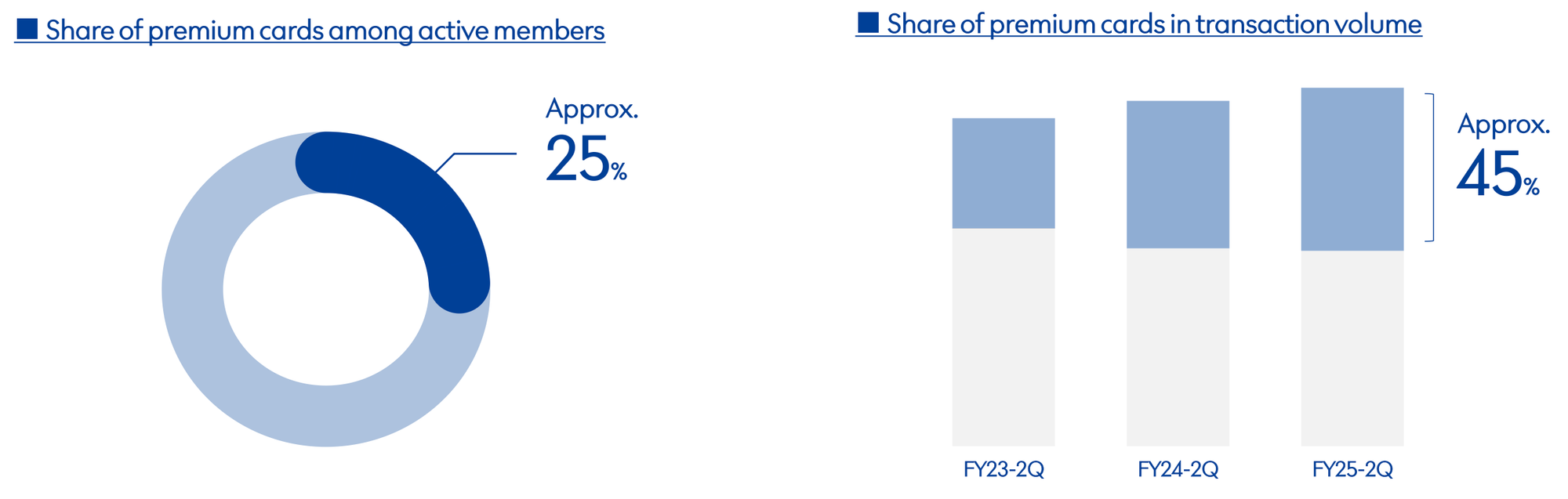

Payment Business: "Premium Strategy" Drives Profitability

The Payment Business delivered an exceptional performance, with Business Profit soaring to ¥17.1 billion, a remarkable 26.4% increase year-on-year. This success is a direct result of the company's "Premium Strategy," which focuses on higher-value, fee-based products such as gold cards, business cards, and cards for small and medium-sized enterprises (SMEs). This strategic shift is proving highly effective in improving per-member profitability and enhancing the quality of revenue streams.

The tangible success of this strategy is evident in several key metrics:

- Share of premium cards among active members: Approximately 25%

- Share of premium cards in transaction volume: Approximately 45%

- Growth in high-margin revenue: Revenue from revolving and installment payments has shown consistent growth, reaching ¥18.3 billion in the second quarter of FY25.

Finance Business: Consistent and Diversified Growth

The Finance Business also demonstrated strong momentum, posting a Business Profit of ¥20.4 billion, a 17.7% increase year-on-year. This consistent growth is supported by a diversified portfolio of financial services that are performing well in the current economic environment.

Key contributors to the segment's strong performance include:

- Subsidiary and Affiliate Strength: The credit guarantee and real estate finance businesses were driven by subsidiary Saison Fundex (contributing ¥8.1 billion to business profit, a YoY increase of ¥2.17 billion) and favorable profit contributions from equity-method affiliate Suruga Bank (contributing ¥3.26 billion, a YoY increase of ¥0.48 billion).

- Favorable Interest Rate Environment: In a rising interest rate environment, the company has benefited from increased revenue from its portfolio of variable-rate products.

While the domestic businesses provide a powerful and stable foundation, the company's international operations are navigating a more complex and challenging landscape.

Global Business Segment: Navigating Headwinds and Pivoting to Recovery

The Global Business segment's performance in the first half was a tale of two markets, characterized by significant headwinds in Indonesia that overshadowed positive recovery signals from India. This segment remains a strategic priority for long-term growth, but its current results reflect a business in a phase of consolidation and risk management as it builds a more sustainable foundation for the future.

The Indonesian Challenge: Increased Credit Provisions

The Global Business segment recorded an overall business loss of ¥4.6 billion for H1 FY25. This loss was almost entirely driven by issues in the Indonesian market, where the company booked an increased allowance for expected credit losses (ECL) of approximately ¥4.7 billion. Management attributed this to a "deterioration in the P2P lending market and the emergence of risk at some business partners." Management noted this was a "quite conservative" provision, made to address systematic market risks and build a clean foundation for FY2026 and beyond. Importantly, management has communicated that most of these provisions are expected to be recorded within the current fiscal year, and the impact on profits from FY2026 onward is expected to be limited.

India's Recovery and Strategic Pivot

In contrast to the difficulties in Indonesia, the India business has turned a corner, returning to profitability in the second quarter and shifting to a clear recovery trend. The strategic focus in India is now on expanding direct lending through its Branch Lending and Embedded Finance channels. The company aims for these direct lending models to eventually comprise 50% of its total receivables balance. Encouragingly, management expects credit costs in India to decline in the second half of the fiscal year, signaling growing confidence in the portfolio's quality and risk management framework.

Impact on Long-Term Targets

Due to the significant challenges encountered, particularly in Indonesia, the achievement of the medium-term management plan's target of ¥20 billion in business profit from the Global Business is now expected to be delayed by one to two years. This resets near-term expectations for the segment's contribution to overall corporate growth.

The operational challenges in the Global segment and the strength of the domestic business provide crucial context for the company's revised full-year financial forecasts and its unwavering commitment to its capital allocation policy.

FY2025 Forecast and Capital Policy: Signaling Confidence

A company's full-year forecast and its capital policy are powerful signals to investors, reflecting management's confidence in the business outlook and its commitment to shareholder returns. Despite downward revisions to its net profit forecast, Credit Saison's decisions to maintain its business profit target and dividend forecast underscore a belief in the resilience of its core operations.

Revised Full-Year FY2025 Forecast

The company has revised its consolidated forecast for FY2025 (ending March 31, 2026). While the core business profit target remains unchanged, the forecast for net profit attributable to owners has been lowered to account for special losses.

Commitment to Shareholder Returns

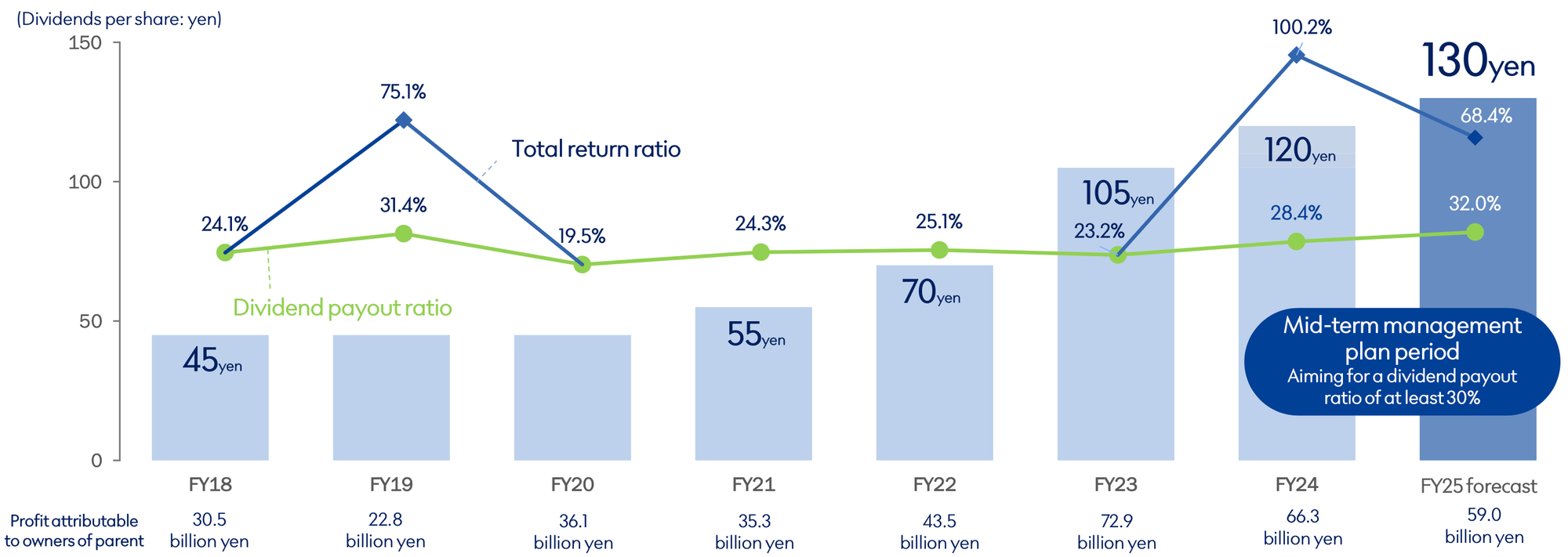

In a strong signal of confidence, and despite the downward revision to net profit, the company's dividend forecast remains unchanged at ¥130 per share. This decision, in the face of a net profit downgrade, is a particularly strong signal of management's conviction in the earnings power of the core domestic segments and its commitment to a predictable shareholder return policy. This aligns with the company's stated policy of maintaining a target dividend payout ratio of at least 30%.

Furthermore, the company has made significant progress on other key capital policy initiatives designed to enhance shareholder value.

- Share Buybacks: The company has completed the planned ¥70.0 billion of share buybacks outlined for the medium-term management period (FY24-26) as of October 1, 2025.

- Cross-Shareholdings Reduction: As of September 30, 2025, the company has achieved a 61.8% progress rate on its target for reducing cross-shareholdings during the medium-term plan.

This disciplined approach to capital allocation, combined with the performance of the various business segments, informs a balanced investment thesis for Credit Saison.

Investment Thesis: A Balanced View

Credit Saison presents a compelling investment case centered on a highly resilient and profitable domestic core business that is successfully funding a strategic, albeit currently challenged, international expansion. Management has demonstrated a clear commitment to enhancing shareholder value through a successful premium strategy, disciplined capital returns, and a forward-looking digital transformation. However, investors must balance this against the execution risks in the Global Business and the impact of non-recurring charges on near-term profitability.

Strengths | Risks & Headwinds |

Dominant Domestic Core: Payment and Finance segments show strong, double-digit profit growth, providing a stable foundation. | Global Business Execution: Significant losses in Indonesia require careful management to contain the impact to FY25 as planned. |

Successful Premium Strategy: Proven ability to improve profitability and revenue quality by focusing on higher-value customers. | Delayed Global Targets: The ¥20 billion profit target for the Global Business is delayed by 1-2 years, impacting the medium-term growth story. |

Disciplined Shareholder Returns: Maintained dividend forecast and completed a ¥70.0 billion buyback program, signaling strong confidence from management. | Domestic Credit Quality: Non-consolidated 90+ day delinquency rates remain elevated, and the company has slightly increased its credit cost forecast. |

Digital & AI Transformation: The CSAX strategy demonstrates a forward-looking approach to improving long-term cost efficiency and competitiveness. | Amusement Business Exit: Planned withdrawal from the Concerto Inc. amusement business will result in a special loss of approximately ¥6.0 billion, impacting FY25 net profit. |

Key Catalysts to Monitor

Moving forward, investors should monitor the following key catalysts, which will be critical in determining the company's trajectory and unlocking further shareholder value:

- Turnaround in Global Business Profitability: Successful containment of Indonesian losses and continued recovery momentum in India in the second half of FY25 and beyond will be crucial for validating the long-term international growth narrative.

- Sustained Momentum in Premium Strategy: Continued growth in revolving and installment balances and per-member profitability in the Payment segment will demonstrate the durability of this core profit driver.

- Execution of CSAX Strategy: The realization of tangible cost savings and operational efficiencies from the AI transformation initiative will be a key indicator of future margin expansion. The company is targeting a cumulative reduction of 3 million work hours by 2027.