Debt Sustainability in Japan

Japan combines the highest public debt ratio among advanced economies with a fiscal framework that has struggled to anchor fiscal policy. As monetary policy normalizes and interest rates rise, concerns about debt sustainability have intensified.

In a recent Bruegel Working Paper, the authors assess Japan’s debt dynamics using stochastic debt sustainability analysis, and examine the institutional foundations of its fiscal framework.

They show that debt outcomes are highly sensitive to growth assumptions. Under plausible baseline scenarios, debt does not stabilize without sustained primary surpluses and even optimistic growth assumptions require fiscal adjustment relative to the current structural primary balance.

Japan’s challenge is institutional as well as economic: weak enforcement of fiscal rules and the absence of independent oversight undermine credibility. Strengthening fiscal institutions, particularly through an independent fiscal council, could support debt stabilization.

1. Executive Mandate: The End of the "Low-Yield Cushion"

Japan has reached a structural inflection point that demands an immediate departure from the fiscal complacency of the last three decades. The normalization of monetary policy—highlighted by the policy interest rate reaching 0.75 percent in January 2026—has effectively dismantled the "low-yield cushion" that previously permitted the maintenance of the world’s highest debt ratio. The authors project a transition from a favorable interest-growth differential (r < g) to a positive differential (r > g), where debt-servicing costs (r) will begin to outpace economic expansion (g).

The urgency of this shift is underscored by the Takaichi administration’s late-2025 stimulus package. This $135 billion expansionary measure, the largest since the pandemic, directly conflicted with the Bank of Japan’s tightening cycle, triggering an immediate surge in 10-year JGB yields. This market reaction signals that investors are no longer willing to ignore Japan’s fiscal trajectory.

Key Risk Indicators

- 2024 Debt-to-GDP Ratio: 222% (Gross financial liabilities).

- Monetary Normalization: Policy interest rate at 0.75% (Jan 2026); 10-year JGB yields exceeding historical 0.5% ceilings.

- Fiscal-Monetary Conflict: $135 bn Takaichi stimulus package (Nov 2025) heightening market sensitivity and yield volatility.

Current institutional safeguards are insufficient for this new era. Market confidence now rests on Japan’s ability to transition from ad-hoc crisis management to a rigorous, independent fiscal architecture.

2. Analytical Diagnostic: The High Sensitivity of Debt Sustainability

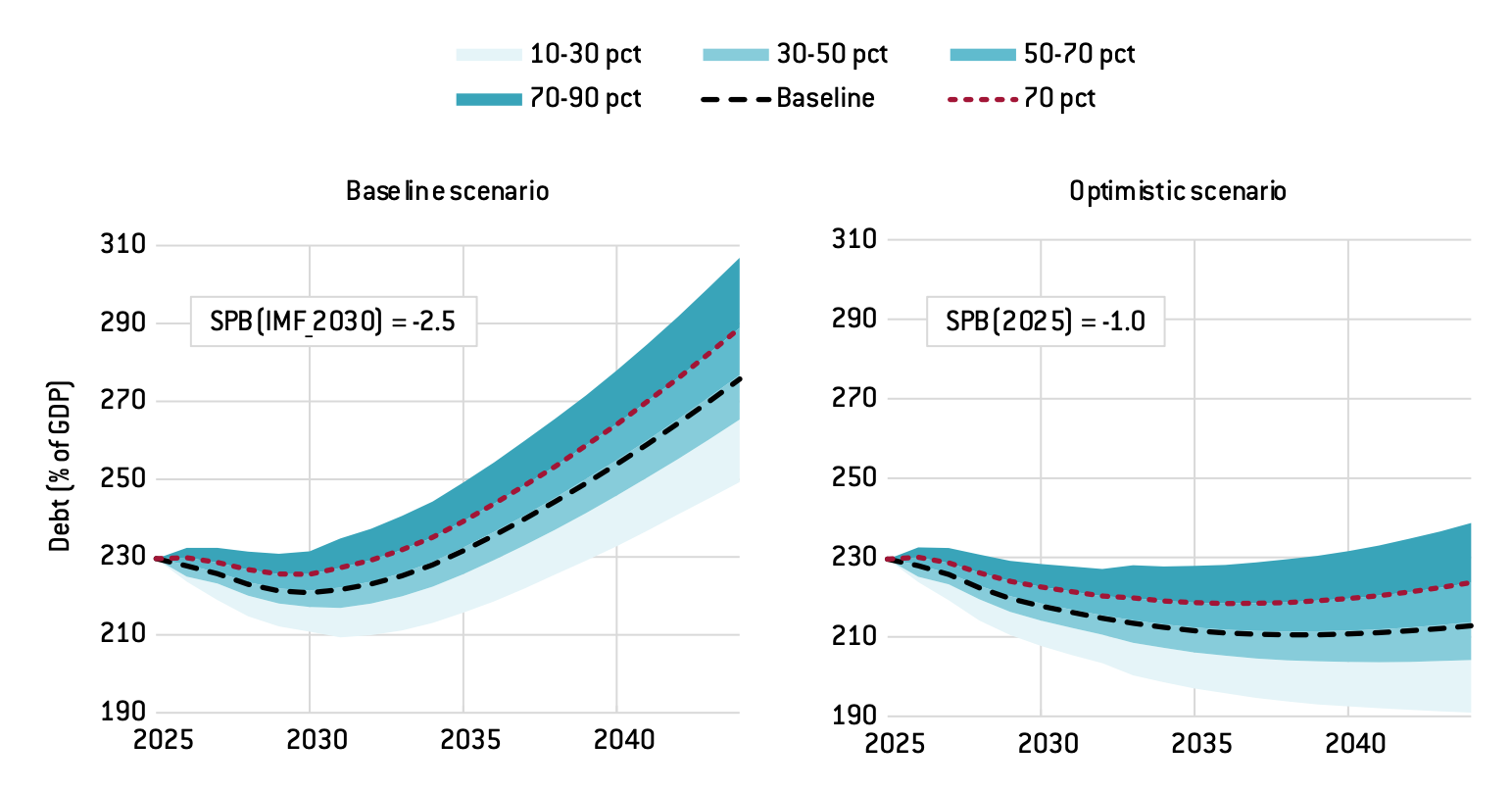

Debt Sustainability Analysis (DSA) is a sensitive projection of long-term solvency. In Japan, the current trajectory is unsustainable even under relatively favorable conditions. The authors treat debt as "stable" only if the slope of the 70th percentile stochastic forecast—the threshold used to account for adverse shocks—becomes flat for the final five years of the 20-year projection horizon.

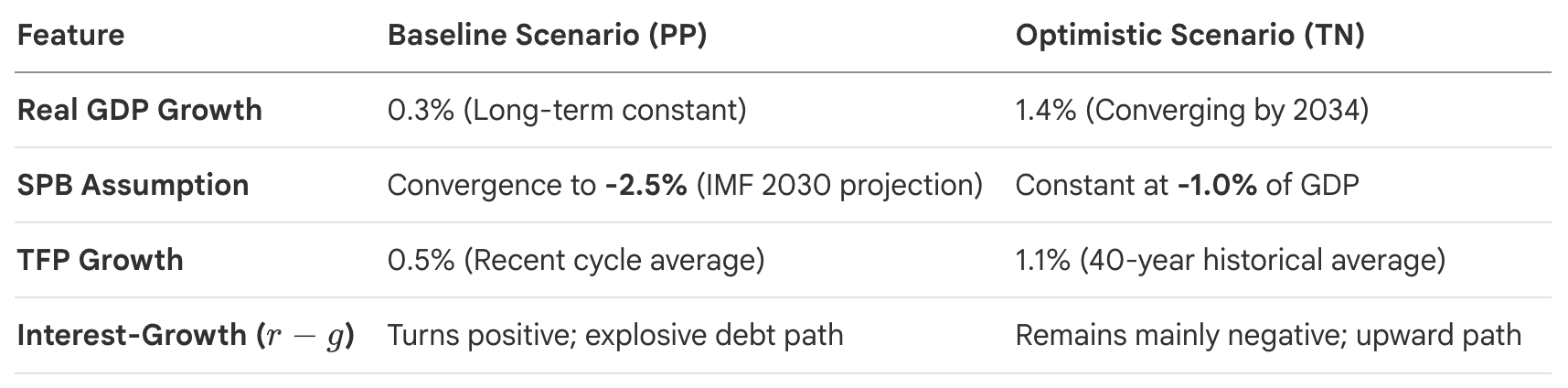

Under this rigorous standard, current policies fail. The authors' diagnostic compares the Baseline Scenario (PP - Projection of Past Trend) against the Optimistic Scenario (TN - Transferring to a New Economic Stage).

Stochastic simulations reveal that even in the Optimistic (TN) case, debt eventually rises because the primary balance remains in a persistent deficit. The temporary decline in debt ratios seen in early years is merely a vestige of maturing low-yield debt; as new debt is issued at market rates, the trajectory turns sharply upward.

The "Net Debt" Fallacy and Risk-Premium Backing

Critics often point to Japan’s net debt (~96%) and substantial financial assets to downplay fiscal risks. However, these assets do not provide a true buffer. Japan’s sovereign balance sheet functions as a leveraged investment position. These assets possess a "pro-cyclical" risk-premium backing: their value tends to decline precisely when economic conditions worsen and the government's financing needs are highest. Selling these assets to reduce gross debt would also eliminate the dividend streams currently supporting the budget, offering no escape from the fundamental need for structural primary balance (SPB) adjustment.

3. The Institutional Conflict: Addressing the "Optimism Bias" in Forecasting

Japan’s recurring failure to stabilize debt is rooted in a "forecasting-policy loop." Currently, the Cabinet Office—a branch of the executive—produces the macroeconomic forecasts that justify the budget. This creates an inherent "bias towards optimism," where growth assumptions are inflated to avoid the political cost of fiscal consolidation.

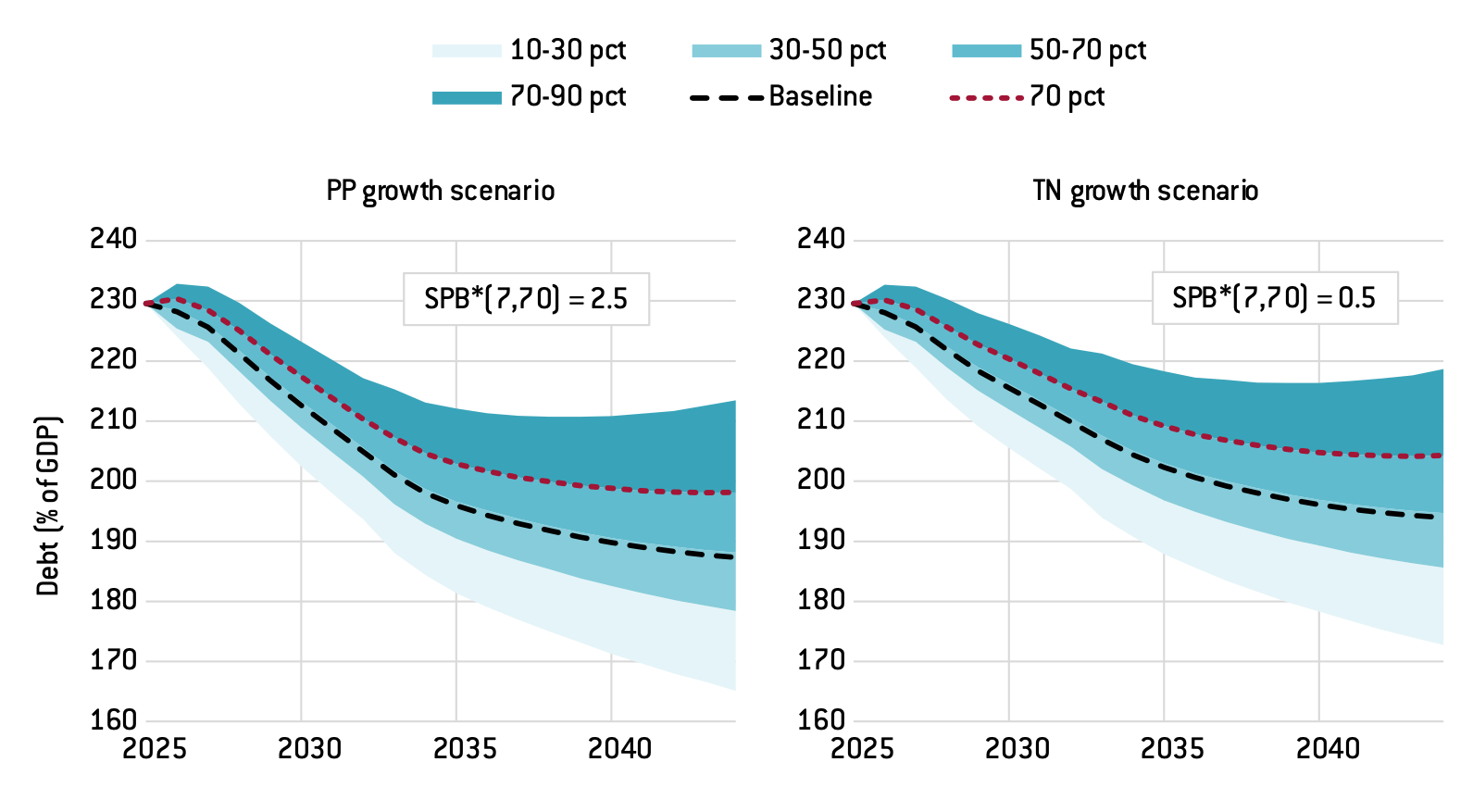

To achieve debt stability (70th percentile flat slope), Japan must shift from its current structural primary deficit to a sustained surplus.

- Required SPB Surplus: +0.5% (Optimistic TN) to +2.5% (Baseline PP).

- Implicit Adjustment Need: 1.5% to 3.5% of GDP relative to the current 2025 stance (-1.0% SPB).

Even under the most optimistic growth assumptions, a primary surplus of at least 0.5% is mandatory.

This data confirms that "growth alone" cannot solve the debt crisis. The lack of independent verification allows the government to delay necessary adjustments, undermining the credibility of Japan’s fiscal commitments in the eyes of global markets.

4. Historical Precedents: The Failure of Rigid Rules and Ad-Hoc Bypasses

Japan’s history demonstrates that fiscal rules without "structured flexibility" are destined for abandonment. The Public Finance Act (Article IV) ostensibly requires expenditures to be financed by revenues, yet it contains a loophole for "construction bonds" for public investment. For decades, this has been bypassed by "special legislation" to issue deficit-financing bonds, making the exception the rule.

Chronological Institutional Failures

- 1997 Fiscal Structural Reform Act: Aimed for a deficit below 3% by 2005. It lacked an escape clause and was suspended within one year following the 1997 financial crisis and a subsequent pivot to stimulus.

- 2006 Reform: Targeted a primary surplus by the early 2010s; abandoned following the Global Financial Crisis and a change in government.

- 2010 Expenditure Rule: Introduced a surplus target for 2020; shelved after an administration change and the adoption of the "three arrows" of Abenomics.

The lesson is clear: rigid rules collapse under shocks, leading to total suspension. A durable framework requires a middle ground between total rigidity and ad-hoc survival.

5. Policy Proposal I: The Independent Fiscal Council (IFC)

Japan is an outlier among G7 nations, lacking a formal independent oversight body (a distinction shared only with Australia and New Zealand). While the Council on Economic and Fiscal Policy (CEFP) exists, it is a Cabinet-level body chaired by the Prime Minister and tasked with policy formulation. It cannot serve as a watchdog over the very government that leads it.

The authors propose a truly Independent Fiscal Council (IFC) with a mandate to either produce or formally endorse the macroeconomic forecasts used in the budget.

The Four Pillars of IFC Independence

- Statutory Mandate: A permanent legal agency tasked with assessing fiscal plans against long-term sustainability and the 70th percentile stability criteria.

- Professional Expertise: Appointments based on economic rigor rather than ministry representation or party affiliation.

- Timely Information Access: Statutory rights to internal Ministry of Finance and Cabinet Office data.

- Public Visibility: A requirement to issue public reports to the National Diet, shaping the transparency of the fiscal debate.

6. Policy Proposal II: Adaptive, Rule-Based Escape Clauses

To prevent the total "shelving" of fiscal rules during crises (as seen in 1998), Japan must codify Adaptive, Rule-Based Escape Clauses. These clauses do not weaken the framework; they preserve it by providing a transparent, predefined path for deviation during exceptional shocks.

Design Framework for the Escape Clause

- Activation Transparency: Limited to clearly defined shocks (severe recessions, financial crises, or major natural disasters).

- Independent Assessment (The IFC’s Role): The IFC must "call the ball"—providing the independent certification that activation criteria are met and setting the timeline for the return to the rule-based path.

- Limited Duration: Deviations must be temporary, with a mandatory sunset provision to ensure a return to fiscal discipline once the shock subsides.

This creates a "virtuous cycle": the IFC provides the "truth" in the numbers, while the escape clauses provide the "valve" for crises, ensuring the framework remains intact through economic cycles.

7. Conclusion: A New Fiscal Social Contract

Japan can no longer rely on the historical anomaly of zero-cost borrowing. The transition to normalized interest rates means that debt sustainability is now as much an institutional challenge as an economic one.

Japan must move from "ad-hoc survival" to strategic institutionalism. By separating forecasting from policy-making through an Independent Fiscal Council and replacing ad-hoc bond legislation with structured escape clauses, Japan can restore its fiscal credibility. The 1.5% to 3.5% GDP adjustment needed for stabilization is a monumental task, but it is a necessary one to secure market confidence and protect the national interest in an era of rising yields. The "low-yield cushion" has been pulled away; the time for institutional architecture has arrived.