FSA Tightens Supervision of “Asset-Intensive” Reinsurance to Bolster Solvency

Japan’s Financial Services Agency (FSA) is significantly expanding its regulatory framework for insurance companies, with the proposed revisions to the "Comprehensive Guidelines for Supervision of Insurance Companies" signaling a heightened focus on the economic reality of reinsurance contracts, particularly "asset-intensive" structures that have become increasingly common in the industry.

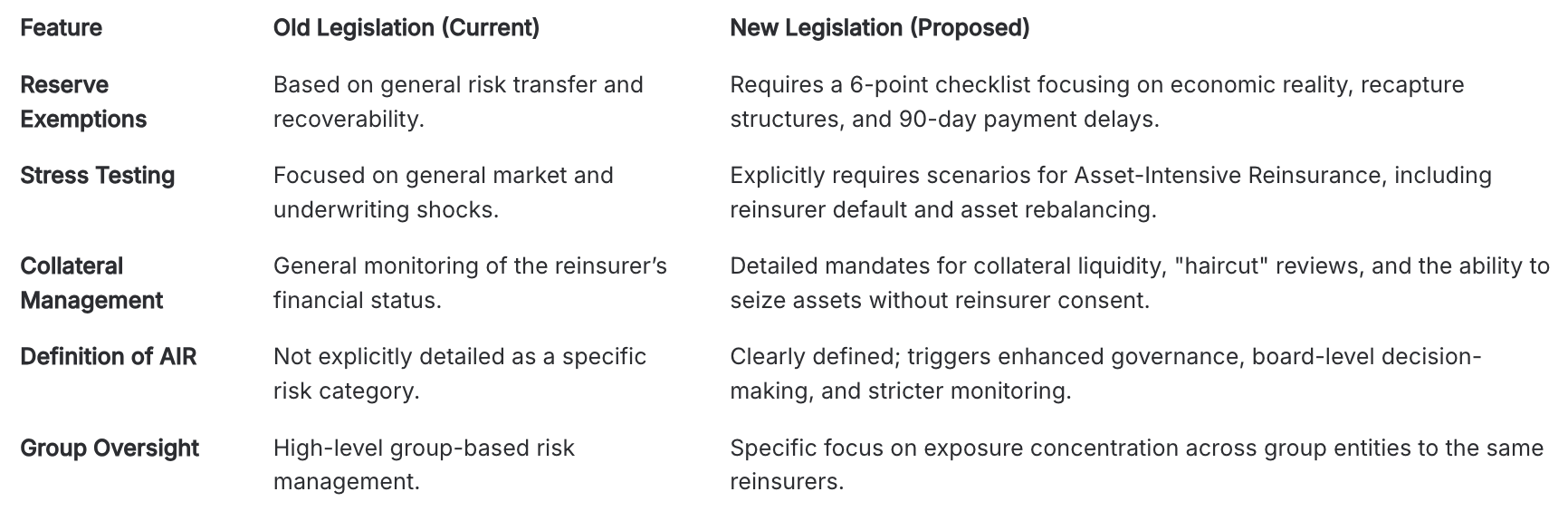

Under the existing guidelines, insurers could opt not to set up policy reserves for the portion of a contract ceded to a reinsurer based on a high-level assessment of risk transfer and recoverability.

The revised guidelines introduce a strict checklist to determine if a contract truly transfers risk. Insurers must now evaluate whether the reinsurer has undue discretion that could impair the economic value of the ceding company’s stake. Furthermore, the regulator will scrutinize "recapture" clauses—where an insurer takes back the risk and assets—and transactions primarily intended for financing rather than genuine risk transfer. If a settlement is delayed by more than 90 days, the validity of the reserve exemption may be called into question.

Focus on Asset-Intensive Reinsurance (AIR)

The most substantial updates target "Asset-Intensive Reinsurance," defined in the text as arrangements where both insurance liabilities and their corresponding assets are transferred to a reinsurer, who then assumes both the investment and underwriting risks.

The FSA now mandates that stress tests specifically account for AIR. These tests must simulate "reverse stress" scenarios, such as the simultaneous failure of multiple reinsurers or a sudden deterioration in the economic environment affecting the ceding company’s solvency margin. Insurers are expected to have "crisis response plans" ready, detailing how they would rebalance assets or replenish reserves if a recapture event is triggered.

Rigorous Collateral and Recapture Governance

The revisions transition from a general oversight of reinsurers to a prescriptive management of collateral and legal rights. Key changes include:

- Collateral Quality: Insurers must establish clear investment guidelines for collateral assets, including credit rating floors, liquidity requirements, and concentration limits.

- Operational Control: The ceding company must ensure it can execute collateral claims or asset withdrawals without the reinsurer’s consent if specific "triggers" (such as a decline in collateral value or a delay in payments) are met.

- Recapture Strategy: Companies must have a formal policy for "early recapture" if a reinsurer’s financial health declines, including plans to manage the liquidity and market risk of assets returned to their books.

Group-Wide Concentration Risk

The regulator is also addressing "concentration risk" at the group level. The new guidelines require management to monitor whether multiple subsidiaries within the same insurance group are ceding risk to the same or similar reinsurers. This is intended to prevent a "domino effect" where the failure of a single large offshore reinsurer could destabilize an entire Japanese domestic insurance group.

Summary of Key Differences

These changes reflect a global trend among regulators to look past the "form" of reinsurance contracts to their "substance." By demanding that Japanese insurers treat reinsurance as a complex investment-underwriting hybrid rather than a simple hedge, the FSA is aiming to ensure that the industry's solvency remains robust even in the face of offshore counterparty volatility.