FUNDINNO’s Reports Revenue Dip in First Earnings as Public Company

In the high-stakes arena of private equity and venture capital, timing is everything. For FUNDINNO (TSE Growth: 462A), Japan’s premier digital platform for unlisted equities, the timing of mega-deals has resulted in a sluggish first quarter for the fiscal year ending October 2026. However, to judge the company solely by its Q1 top-line revenue would be to miss a profound structural shift occurring beneath the surface—a shift punctuated by a landmark IPO that validates the company's entire business model.

In its earnings presentation released on March 13, 2026, FUNDINNO reported Q1 operating revenue of 410 million yen, representing a year-over-year decline. Operating profit also slipped into negative territory, registering a loss of 181 million yen.

Yet, the tone of FUNDINNO CEO Yuki Shibahara during the earnings call was anything but panicked. The company maintained a fiercely bullish full-year forecast, projecting operating revenue to surge 55.6% to 3.89 billion yen, with operating profit expected to skyrocket 430.1% to 1.13 billion yen.

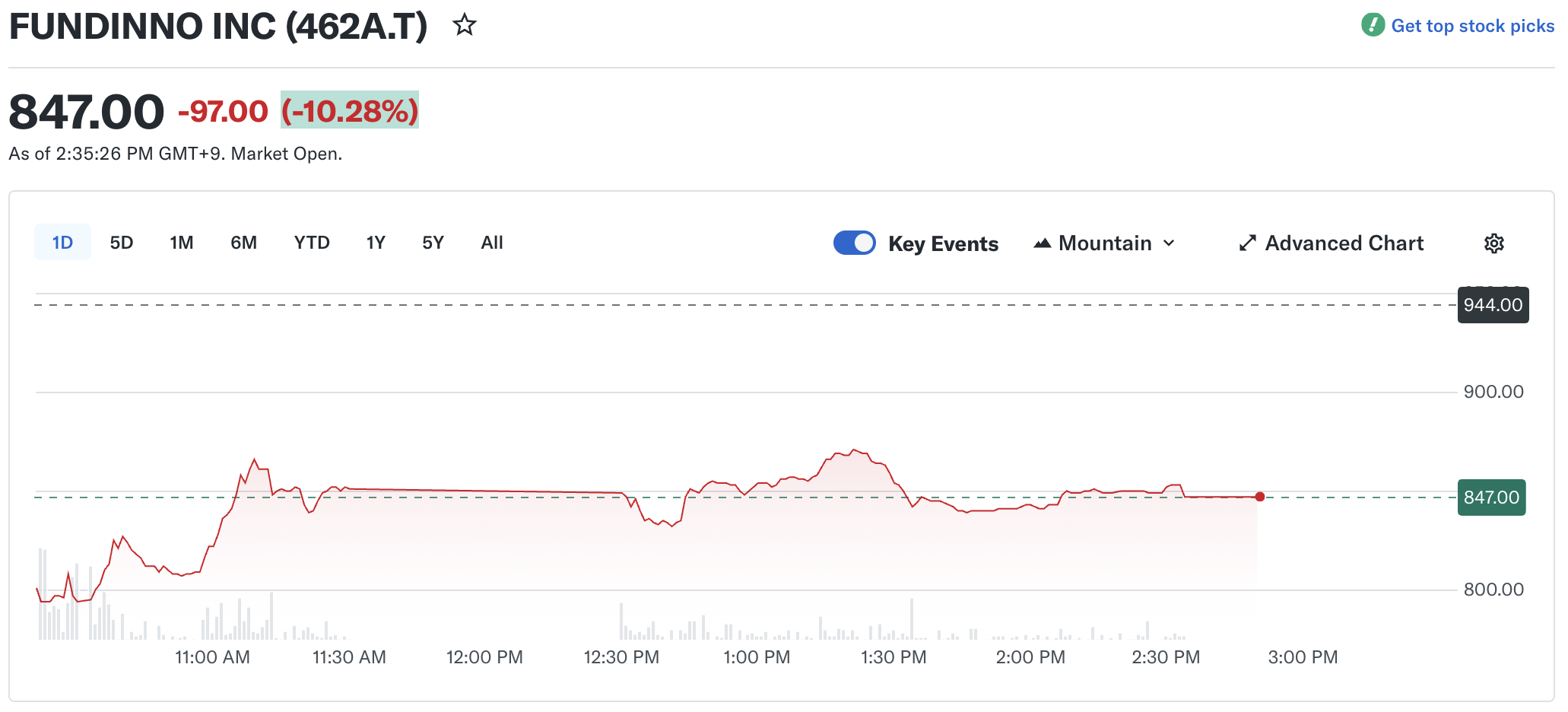

The market was not quite that sanguine, with FUNDINNO opening "limit down" at 794 yen, although recovering to around 850 for the remainder of Monday's session. That is pretty much in line with its December 5, 2025, IPO, which was priced at the top of the indicated range from JPY 600 to 620. After reaching a high of JPY 935 during the first day of trading, the stock then settled in around the JPY 800 mark, giving FUNDINNO a market cap of approximately USD 120m.

The dichotomy between a quiet first quarter and explosive full-year guidance tells a compelling story about the maturation of Japan's startup funding ecosystem, the volatility of large-ticket private fundraising, and the evolution of FUNDINNO from a retail crowdfunding site into a sophisticated, institutional-grade financial infrastructure.

The Financials: A Tale of Timing and Deal Volatility

To understand FUNDINNO’s Q1 contraction, one must look at the mechanics of its primary revenue driver: the "FUNDINNO PLUS+" service.

Unlike its legacy Equity Crowdfunding (ECF) service, which is capped at smaller retail investments, FUNDINNO PLUS+ targets "Accredited Investors"—a regulatory classification for high-net-worth individuals and institutional players. This tier utilizes the "J-Ships" (Specified Investor Private Placement) scheme, allowing startups to raise virtually limitless capital.

Because of the sheer size of these deals, the company's quarterly revenue is highly susceptible to volatility. A single funding round can alter the financial landscape of a quarter.

"The large-scale funding support provided by FUNDINNO PLUS+ experiences a certain degree of volatility in quarterly performance depending on deal scale, disclosure timing, and the fundraising period," the company noted in its financial materials.

In the first quarter of the previous fiscal year (FY10/2025), FUNDINNO successfully closed two mega-deals exceeding 1 billion yen each. In stark contrast, the first quarter of FY10/2026 saw zero deals in the 1 billion yen+ tranche, and only two deals in the 500 million to 1 billion yen range.

CEO Yuki Shibahara emphasized that this was not a demand issue, but a strategic timing decision. "We execute disclosures by assessing the needs of the issuing companies and investors, aiming for the timing that maximizes project revenue," Shibahara stated. "As a result, the booking of large-scale projects in the first quarter has been shifted to subsequent quarters."

Essentially, FUNDINNO is holding its fire. The pipeline remains robust, but the revenue recognition has simply rolled over into Q2 and beyond. The company is actively investing its resources into what it calls "preparations" for discontinuous, exponential growth post-listing—specifically, expanding its investor potential and enriching its product offerings.

Proof of Concept: The InnovaCell Milestone

If there was any anxiety regarding the Q1 revenue dip, it was thoroughly eclipsed by a monumental milestone achieved just weeks prior to the earnings release.

On February 24, 2026, InnovaCell, a regenerative medicine and cell therapy biotech firm, successfully listed on the Tokyo Stock Exchange (TSE) Growth Market. InnovaCell is the very first company to go public after utilizing the "J-Ships" regulatory framework on the FUNDINNO PLUS+ platform.

The timeline is a testament to the platform's efficacy as a late-stage growth engine. In December 2024, InnovaCell raised approximately 1.06 billion yen through FUNDINNO PLUS+. Just 14 months later, the company went public. The stock, which was issued at 850 yen during the FUNDINNO raise, priced its IPO at 1,350 yen and opened at an initial price of 1,248 yen.

For the Japanese venture ecosystem, this is a noteworthy development. Historically, traditional venture capital firms and institutional investors viewed equity crowdfunding with deep skepticism. The prevailing stigma was that bringing a crowd of retail investors onto a cap table would create a governance nightmare, effectively poisoning the company's chances of a future IPO.

The InnovaCell listing disproves this narrative. It clearly shows that a startup can raise late-stage, mega-round capital via a digital platform, aggregate high-net-worth investors through the J-Ships scheme, and seamlessly transition into the public markets without regulatory or governance friction.

"The existence of our platform has been proven to be a direct catalyst for accelerating corporate growth and leading to an IPO exit," CEO Shibahara remarked during the earnings call. "We view this as a vital milestone."

This success story serves a dual purpose for FUNDINNO. First, it acts as the ultimate marketing tool to attract high-quality, late-stage startups that previously might have only looked to traditional VC or private equity. Second, it creates a powerful wealth-creation cycle for investors. The 83 accredited investors who participated in the InnovaCell round are subject to an institutional lock-up period, but upon expiration, the realized capital gains are highly likely to be recycled back into the FUNDINNO ecosystem for new investments.

KPI Deep Dive: Chasing the Ultra-Wealthy

FUNDINNO’s Q1 results highlighted several key performance indicators (KPIs) that underscore its strategic pivot toward the ultra-wealthy. The most critical metric is Gross Merchandise Value (GMV), defined as the total value of primary domain investments and secondary domain stock trades executed on the platform.

In Q1, cumulative GMV since the company's inception officially breached the 300 billion yen mark—a psychological and financial barrier that cements FUNDINNO's position as the undisputed market leader in Japan's unlisted equity space, boasting a 92.1% market share in the ECF domain and a 100% monopoly in the J-Ships domain.

To sustain this GMV growth, FUNDINNO is relentlessly pursuing "Accredited Investors." FUNDINNO's stated target demographic is Japan's ultra-high-net-worth individuals—specifically, the estimated 118,000 households possessing over 500 million yen in purely financial assets.

In Q1, the number of registered Accredited Investors grew by 124, reaching a total of 1,746. While this number may sound small compared to retail brokerage accounts, the concentration of wealth is staggering. Because the J-Ships scheme removes the investment caps inherent in traditional equity crowdfunding, securing just a few dozen of these investors can fully fund a billion-yen startup round.

Expanding the Moat: The Regional Banking Strategy

How does a Tokyo-based FinTech company find and onboard Japan's quiet, ultra-rich elite? The answer lies in B2B2C strategic alliances.

FUNDINNO has built an impressive network of partnerships with regional banks, independent financial advisors (IFAs), and regional securities firms. As of Q1, this network has expanded to 37 partnered institutions.

This strategy is brilliant in its symbiosis. Regional banks in Japan are flush with deposits from wealthy local business owners, but in a historically low-yield environment, they struggle to offer exciting, high-return alternative investment products. By partnering with FUNDINNO, these regional financial institutions can introduce their top-tier clients to exclusive, late-stage venture capital opportunities without taking on the regulatory burden or underwriting risk themselves.

Furthermore, because FUNDINNO deals exclusively in unlisted equities, it does not cannibalize the banks' traditional operations. "By handling unlisted stocks—which do not compete with other financial institutions—we can forge alliances based on the deep regional trust held by these banks and securities firms," the company noted. This mutual referral scheme acts as an elite, decentralized sales force, driving high-net-worth individuals directly onto the FUNDINNO PLUS+ platform.

The Secondary Market: Solving the Illiquidity Trap

One of the great deterrents to private equity investing is the illiquidity discount. Capital is locked up for years, with investors unable to exit until an IPO or M&A event. FUNDINNO is addressing this head-on with the expansion of its secondary market capabilities.

The company operates "FUNDINNO MARKET" for standard retail users and "FUNDINNO MARKET PLUS+" for high-net-worth and institutional block trades. By facilitating a venue where already-issued unlisted shares can be traded between investors, FUNDINNO is injecting much-needed liquidity into the private markets.

In Q1, secondary market GMV accounted for roughly 4.4 million yen via peer-to-peer trades. However, the company is preparing for a massive leap forward. FUNDINNO has been building a framework to capture the selling needs of unlisted stocks outside of its own primary platform. This means facilitating block trades for venture capital firms or early employees of non-FUNDINNO startups who need liquidity.

The company expects to realize significant block trades (large-lot secondary transactions) in the upcoming second quarter. If successful, this effectively transforms FUNDINNO from a primary issuance platform into a true, holistic stock exchange for private companies.

Navigating Regulatory Tailwinds

FUNDINNO’s growth is inextricably linked to the Japanese government's broader macroeconomic policy. Under the administration's "Five-Year Startup Development Plan," fostering a vibrant venture ecosystem is viewed as a matter of national economic security. Consequently, the regulatory landscape is shifting rapidly in FUNDINNO's favor.

Historically, Japan's Financial Instruments and Exchange Act strictly regulated how companies could solicit investments. The 2015 legalization of Equity Crowdfunding (ECF) birthed FUNDINNO, but it came with severe handicaps: a company could only raise up to 100 million yen per year, and individuals could only invest up to 500,000 yen per company.

The 2022 introduction of the J-Ships (Accredited Investor) scheme bypassed these limits, but only for professional and high-net-worth investors, creating the foundation for FUNDINNO PLUS+.

Now, the middle market is opening up. In February 2025, a revised law took effect that raised the ECF fundraising limit per project from 100 million yen to just under 500 million yen. Furthermore, the burdensome requirement for strict audit reports—a major hurdle for early-stage startups—is slated for future relaxation.

By closely monitoring and adapting to these regulatory shifts, FUNDINNO is positioning itself to capture every phase of a startup's lifecycle. A company can now raise 300 million yen from the crowd via ECF, return two years later to raise 1.5 billion yen from the ultra-wealthy via J-Ships, manage its cap table via the "FUNDOOR" SaaS product, and eventually go public—all within the FUNDINNO ecosystem.

Balance Sheet Cleanup: Paving the Way for Shareholder Returns

While the revenue narrative dominates the headlines, seasoned financial analysts will take keen interest in a subtle but highly significant corporate action announced by the company.

Effective March 3, 2026, FUNDINNO executed a reduction in capital stock and capital reserves, combined with an appropriation of surplus. Specifically, the company reduced its capital stock by 236 million yen and its capital reserves by over 10 billion yen. These funds were transferred to "other capital surplus," from which 5.15 billion yen was immediately used to wipe out the company's accumulated deficit (retained earnings deficit).

Following this accounting maneuver, the company's capital stock and capital reserves each stand at a lean 50 million yen, with retained earnings at zero, and other capital surplus resting at 5.13 billion yen. Total net assets remain entirely unchanged at 5.23 billion yen.

In corporate finance, this is a classic "balance sheet cleanup." It has no impact on the company's cash position, net assets, or shareholder value. So why do it?

First, there are tangible tax benefits to reducing capital stock to 50 million yen, placing the company in a more favorable tax bracket designed for small-to-medium enterprises under Japanese tax law.

Second, and more importantly for investors, Japanese corporate law prohibits companies from paying dividends or executing share buybacks if they have a negative retained earnings balance. By wiping out the historical deficit accumulated during its aggressive startup growth phase, FUNDINNO has "cleared the pipes." The company now possesses the legal and financial agility to initiate shareholder return policies—such as dividends or stock repurchases—as soon as it generates consistent net income. This signals management's confidence that the days of burning cash for market share are ending, and an era of sustainable profitability is on the horizon.

The Expense Structure: Operational Leverage at Scale

A critical component of FUNDINNO's bullish full-year profit forecast (1.13 billion yen operating profit) is its highly scalable cost structure. As a tech-driven platform, the company enjoys significant operational leverage.

An analysis of the Q1 expenses shows that despite massive growth in GMV and registered users over the past few years, the increase in operating expenses remains heavily constrained. Over the period from FY10/2023 to FY10/2025, the average growth rate of expenses was a mere 7.1%.

The breakdown of costs reveals a healthy dynamic. Outsourcing costs—which include introduction fees paid to regional banks and IFA partners—fluctuate directly with revenue. Therefore, if revenue dips as it did in Q1, these variable costs drop in tandem, protecting the bottom line. Meanwhile, fixed personnel costs have risen slightly, reflecting strategic hiring for sales expansion, but technology keeps the marginal cost of processing a 1 billion yen transaction virtually identical to that of a 10 million yen transaction.

This means that when the delayed mega-deals finally close in Q2 and Q3, the vast majority of that top-line revenue will drop straight to the bottom line as pure profit.

Analyst's Corner: The Road Ahead

Looking at the broader trajectory, FUNDINNO is executing a highly ambitious transition. It is attempting to build the infrastructure that Wall Street and traditional Japanese financial houses failed to build: a liquid, transparent, and democratic market for private equity.

"We want to make this country's venture market more open and democratic," the company's vision statement reads. "To eliminate the gap in information and opportunity for all entrepreneurs and investors. A financial platform equipped with securities, printing, trust, and exchange functions has not yet been perfected even in the global market."

The Q1 results, while optically disappointing on a year-over-year revenue basis, are merely a symptom of the lumpy nature of investment banking and mega-round venture capital. The underlying fundamentals tell a story of vital health:

- Validation: The InnovaCell IPO proves the J-Ships/FUNDINNO PLUS+ model works as a viable path to the public markets.

- Demographics: The successful onboarding of the ultra-wealthy shifts the platform from retail speculation to institutional-grade capital allocation.

- Liquidity: The expansion of the secondary market solves the greatest pain point in venture capital.

- Financial Hygiene: The balance sheet restructuring prepares the company to reward its own shareholders.

As the fiscal year progresses, all eyes will be on the second and third quarters. If FUNDINNO can successfully execute the delayed mega-deals and launch its anticipated large-block secondary trades, the Q1 blip will quickly be forgotten.

With regulatory winds at its back, a monopoly on the J-Ships market, and an expanding network of regional banking alliances, FUNDINNO is no longer just a startup helping other startups. It is rapidly becoming the essential plumbing of Japan's new digital economy. For investors willing to look past the short-term volatility of deal-flow timing, the structural long-term narrative of FUNDINNO remains one of the most compelling stories in the Japanese fintech sector today.