Global Divergence: A Strategic Comparison of US and Japanese Blockchain Regulatory Trajectories

At a Japan Blockchain Association webinar held on February 18, 2026, Startale Group's Sota Watanabe and Kengo Masuyama discussed the evolving landscape of blockchain regulation in both Japan and the United States. The speakers highlight how US legislative drafts, such as the Lummis-Gillibrand and Clarity Acts, are moving toward a tiered system that distinguishes between securities and network tokens. They emphasize that Japan’s regulatory direction is shifting from a focus on payments to investor protection, potentially reclassifying crypto assets under the Financial Instruments and Exchange Act. To ensure Japan remains competitive, the Japan Blockchain Association has established an On-chain Subcommittee to advocate for practical rules for DeFi and stablecoins. The discussion concludes that clear legal frameworks are essential for encouraging traditional financial institutions to adopt on-chain technology without stifling innovation.

1. Strategic Context: The Institutional Shift to On-Chain Finance

The global financial landscape is undergoing a fundamental structural transformation as decentralized infrastructure migrates from retail speculation to the core of institutional capital markets. The transition from a "wait and see" posture to the establishment of formal legislative frameworks serves as the primary catalyst for this shift. By codifying the rules of engagement, regulators in the United States and Japan are moving beyond reactive posturing to provide the legal certainty required for large-scale institutional participation.

The objective of this event report is to provide executive decision-makers with a clinical comparative roadmap of the emerging regulatory regimes: the Lummis-Gillibrand and Clarity Acts in the US, and the Financial Services Agency (FSA) Working Group’s recommendations in Japan. These frameworks represent the "on-ramps" that will dictate global capital flow through 2027. While both jurisdictions seek to foster innovation, their divergent approaches to asset classification and intermediary liability create a complex map for cross-border compliance. Within Japan, these movements signal a definitive pivot toward an investment-centric market structure designed to institutionalize on-chain assets.

2. Japan’s Regulatory Evolution: The Pivot to Financial Instruments Oversight

Japan is executing a strategic migration away from the utility-focused Payment Services Act toward a robust oversight model under the Financial Instruments and Exchange Act (FIEA). This shift is a calculated move to capture the "Investment Side" of the digital asset market. By reclassifying crypto-assets as traditional investment vehicles under the FIEA, Japan aims to align digital assets with existing securities laws, thereby facilitating the approval of Exchange-Traded Funds (ETFs) and providing a level of investor protection commensurate with traditional capital markets.

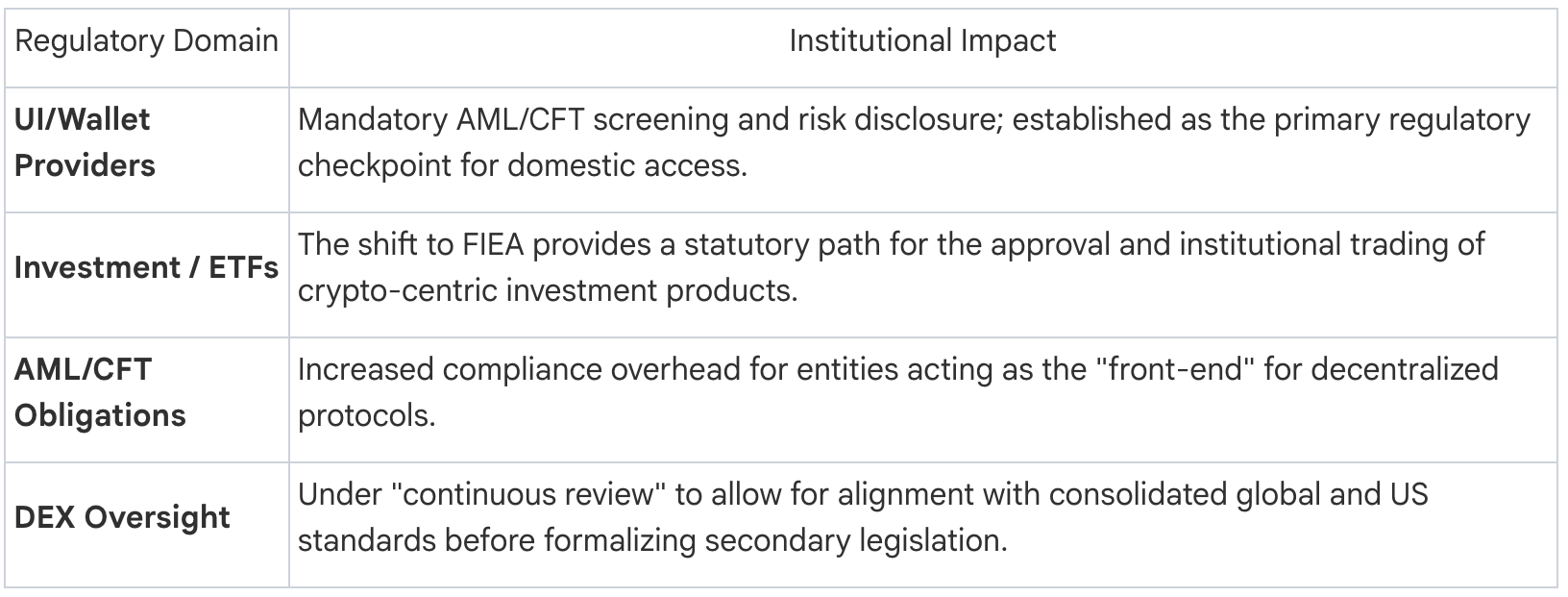

2.1 The FIEA Shift and Decentralized Finance

The FSA’s stance on Decentralized Finance (DeFi) remains under "continuous review." The Working Group report acknowledges that while decentralized exchanges (DEXs) lack a traditional central operator, they cannot remain outside the regulatory perimeter. Consequently, Japanese authorities are focusing on "intermediary regulation," placing specific Anti-Money Laundering and Counter-Financing of Terrorism (AML/CFT) obligations on User Interface (UI) providers. By targeting the gateway rather than the immutable smart contract, the FSA seeks to control access for domestic residents without stifling the underlying protocol.

2.2 Japan’s Regulatory Focus Areas

This focus on the "intermediary" layer sets the stage for a critical contrast with the United States, which is prioritizing the classification of the assets themselves through a statutory on-ramp.

3. The United States: Decoding the Lummis-Gillibrand and Clarity Acts

For the United States, resolving the jurisdictional friction between the SEC and CFTC is a strategic prerequisite to maintaining its position as a global digital asset leader. Current legislative efforts aim to replace "regulation by enforcement" with a predictable lifecycle for digital assets.

3.1 The "Clarity Act" Framework: A Statutory On-Ramp

The proposed Clarity Act (officially the Financial Innovation and Technology for the 21st Century Act in some drafts) introduces a phased lifecycle that allows tokens to evolve from securities to commodities:

- Phase 1: Ancillary Assets: This category creates a dedicated on-ramp for assets that are non-securities but still rely on entrepreneurial efforts. Fundraising is permitted with a cap of $50 million per year or 10% of the asset's market cap. Strict disclosure requirements—including financial statements and management history—apply.

- Phase 2: Network Tokens: Upon achieving "decentralization certification" (where value is driven by protocol utility rather than a central entity), assets transition to CFTC oversight as digital commodities.

- The Micro-Innovation Fund Box: To prevent innovation flight, the US framework includes a regulatory sandbox where developers can apply for specific exemptions while maintaining a transparent dialogue with authorities.

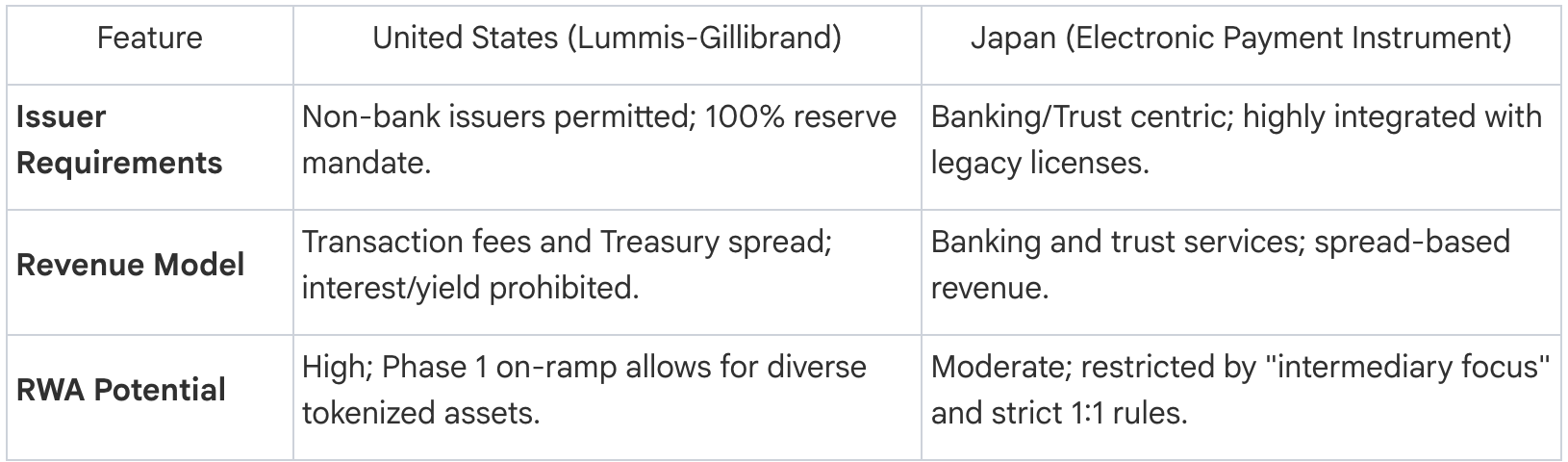

3.2 The Lummis-Gillibrand Payment Stablecoin Act (The "Genius Act")

The Lummis-Gillibrand framework mandates 100% reserves for payment stablecoins and imposes a strict prohibition on the payment of interest or yield to holders. This yield prohibition is a strategic concession to the traditional banking lobby, designed to prevent "deposit flight" from legacy banks into high-yield digital equivalents. While payment stablecoins face these restrictions, the Act includes a separate carve-out for algorithmic models, which will be governed under a distinct, specialized framework.

4. Comparative Analysis: Stablecoins and the Tokenization of Traditional Finance

Tokenized deposits and equities represent the "bridge" to a fully on-chain economy. The US and Japan are taking different approaches to the operational viability of these instruments.

4.1 Yield Models and Electronic Payment Instruments

While the US limits issuers like Circle to a transaction-utility model through the yield ban, Japan classifies stablecoins as "Electronic Payment Instruments" under a framework integrated with banking and trust licenses. This favors Japan's megabanks, allowing them to leverage existing institutional trust for Real World Asset (RWA) collateralization.

4.2 The Three Tiers of Stock Tokenization

The strategic value of stock tokenization lies in administrative efficiency. Traditional Japanese shareholder registries can cost 200,000 JPY to obtain and take weeks to process. Native on-chain issuance (Tier 3) reduces these costs to near-zero and provides instantaneous settlement.

- Synthetic Assets: Price-tracking tokens with no underlying ownership.

- 1:1 Backed Assets: Collateralized tokens where the issuer holds physical shares.

- Direct On-Chain Issuance: Native tokenization where the registry is maintained on-chain.

4.3 Operational Viability for Stablecoin Issuers

5. Institutional Decision-Making: Navigating Cross-Border Compliance

Institutional strategy must account for the diverging philosophies regarding liability.

5.1 Developer vs. Operator Risk

The US framework creates a regulatory safe harbor for non-custodial developers, mitigating the risk of intermediary liability for code publishers. In contrast, the Japanese approach targets the UI and gateway layer for AML/CFT compliance. For protocol developers, the US offers a superior environment for "publishing code," while Japan requires a more rigorous compliance structure for entities acting as the consumer-facing interface.

5.2 The "Strategic Laggard" Risk

If Japan’s regulations remain more restrictive than the US "Ancillary Asset" model, it risks a "jurisdictional exodus." The US Clarity Act requires a US-based entity for its protections; if Japan does not provide a similar statutory on-ramp for fundraising and decentralization, it will lose its Fintech ecosystem to North American or more flexible jurisdictions.

5.3 Three Strategic Mandates for Institutional Compliance Officers

- Benchmark Against US Decentralization Standards: Monitor the specific metrics the US uses to certify an asset as a "Network Token" to ensure protocol designs are compatible with future commodity status.

- Audit Gateway Dependencies: For Japanese operations, verify that all UI and frontend components are equipped for AML/CFT screening to meet "Intermediary" standards.

- Parity Preparation for 2027: Ensure all cross-border operations achieve compliance parity before the 2027 enforcement cliff, when both the US and Japan will have solidified their market structure frameworks.

6. Strategic Outlook: 2025-2027

The period leading to 2027 represents a watershed for digital asset law. Currently, the United States offers superior long-term legal certainty for Real World Asset (RWA) tokenization. Its "Ancillary Asset" categorization provides a defined, legal path for assets to move from private fundraising to public commodity status—a feature Japan currently lacks. Japan’s focus on UI/Gateway oversight creates a higher compliance overhead for decentralized protocols compared to the US "safe harbor" for code.

The ultimate destination for both jurisdictions is a state of "De-Cefi"—the fusion of decentralized blockchain infrastructure with regulated, centralized gateway providers. Success in this era will be defined by the ability to leverage the radical cost efficiencies of on-chain issuance (e.g., the reduction of registry costs from 200,000 JPY to near-zero) while navigating the increasingly strict gateway regulations of these two dominant financial powers.