IPO-Grade Corporate Governance Policy Framework

For this article, we have applied the recently updated "Preparation Guidebook for Initial Public Offerings (IPOs)", published by the Japanese Institute of Certified Public Accountants (JICPA), to generate an IPO-grade corporate governance policy framework that startups need to complete before conducting an accounting audit.

1. The Strategic Mandate: Defining the 'Tone at the Top'

The transition from a private entity to a public institution is a fundamental transformation of the company’s social identity. To list on a public exchange, the organization must move beyond an owner-centric model toward a structure of social credibility and investor protection. This transition is anchored by the "Tone at the Top"—a culture where high ethical standards and integrity are non-negotiable. As the company prepares to manage capital provided by general investors, management must demonstrate a profound commitment to accountability and transparency, ensuring the firm is prepared to meet its heightened social responsibilities.

1.1 CEO’s Statement of Governance Principles

The CEO mandates the following core principles to institutionalize this mandate:

- Absolute Accountability: Management shall provide clear, accurate explanations (accountability) to all stakeholders regarding management decisions and financial health.

- Proactive Information Disclosure: The firm must ensure timely and appropriate disclosure of financial and non-financial information, exceeding minimum legal requirements to foster investor trust.

- Elimination of Arbitrary Management: Subjective, owner-driven decision-making is strictly prohibited. Management must replace informal "Kessai" (approvals) via chat or email with institutionalized processes and formal approval rules to prevent governance failures.

- Mandated Legal Adherence: The organization shall prioritize compliance with the Financial Instruments and Exchange Act, the Companies Act, and all tax and labor laws as the absolute baseline for business execution.

1.2 The Strategic Role of the Corporate Governance Code

The Corporate Governance Code is a strategic mechanism for enhancing medium-to-long-term corporate value. By adopting the "Comply or Explain" framework, the company avoids a rigid, formalistic approach. Instead, it engages in a strategic dialogue, providing rational explanations for its governance choices that align with its specific growth phase. This framework serves as a catalyst for value creation and market confidence.

The effectiveness of rigorous internal control systems is entirely dependent on the ethical stance of top leadership, which must bridge the gap between management’s ethical stance and practical implementation.

2. Financial Reporting Integrity & Internal Control Systems (J-SOX Readiness)

Financial transparency is the cornerstone of a public company’s market relationship. Under the Financial Instruments and Exchange Act, a listing applicant must obtain a "Clean" Audit Opinion for the N-2 and N-1 periods. This requires an accounting infrastructure capable of producing verifiable, high-quality financial statements that withstand the scrutiny of professional auditors.

2.1 Transitioning to Public-Grade Accrual Accounting

Management is commanded to transition from "Tax-Basis Accounting" to "Public-Grade Accrual Accounting." A critical component is the 5-Step Approach for Revenue Recognition:

- Identify the contract with the customer.

- Identify the performance obligations.

- Determine the transaction price.

- Allocate the transaction price to the performance obligations.

- Recognize revenue when (or as) the entity satisfies a performance obligation.

Failing Step 5—recognition upon satisfaction of obligation—is a frequent audit failure point in the N-2/N-1 periods. This transition demands robust evidence (vouchers, contracts, and inspection sheets) to ensure every entry is auditable.

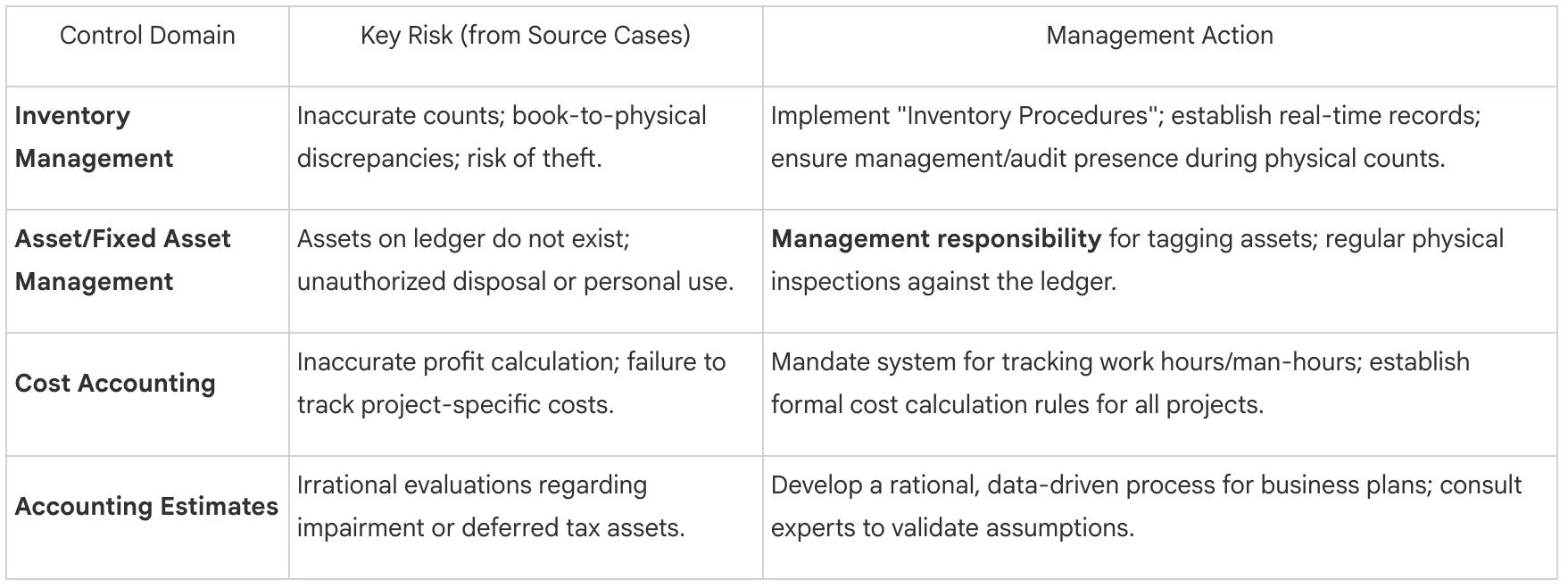

2.2 Critical Internal Control Areas for IPO Readiness

2.3 Internal Control Reporting (J-SOX)

The J-SOX system requires management to evaluate the effectiveness of internal controls over financial reporting. Documentation, evaluation, and audit planning must be prioritized. Critical Compliance Detail: While certain small-scale IPOs (capital < 10 billion yen AND total debt < 100 billion yen) are exempt from the audit of the Internal Control Report for the first three years post-listing, the submission of the Internal Control Report itself is mandatory from the first year of listing.

Rigorous financial controls provide the integrity necessary to manage the operational risks inherent in labor and technology.

3. Operational Risk Management: IT General Controls (ITGC) & Labor Compliance

Operational failures in IT and labor serve as major obstacles to a successful IPO and can lead to significant unrecorded "off-balance" liabilities.

3.1 CEO’s IT General Controls (ITGC) Monitoring Checklist

The CEO must monitor the following controls to ensure data reliability and a valid Audit Trail. Note: Deficiencies in these areas, particularly shared IDs, act as a blocker for the N-2 audit.

- Access Management: Are individual IDs assigned to every user? Shared IDs are strictly prohibited to ensure a clear audit trail of data modifications.

- Change Management: Are there standardized rules and formal approval processes for updating programs and system configurations?

- External Service/Cloud Security: Has the company verified the reliability and security of third-party cloud providers and RPA services?

3.2 Mandatory Directives for Labor Compliance

The Human Resources department is directed to implement the following to avoid pitfalls:

- Elimination of Off-Balance Liabilities: Conduct a comprehensive audit for unpaid overtime. Unpaid wages are debt and must be recorded on the balance sheet.

- Implementation of Objective Time-Tracking: Manual or "fixed-rate" overtime assumptions are insufficient. Management mandates objective time-tracking systems (e.g., PC log-on/off times) to record actual working hours for all employees.

- Adherence to the "36 Agreement": This foundational legal requirement for overtime must be correctly filed and strictly monitored for adherence.

By ensuring operational compliance, the company fulfills its mandate to remain fair and faithful in its business execution.

4. Governance of Stakeholder Relations & Related-Party Transactions

The "Health of Corporate Management" is a primary focus for exchange examiners. To protect general shareholders, management must eliminate conflicts of interest and extract no arbitrary benefits for major stakeholders.

4.1 Directive for Cleaning Related-Party Transactions

All transactions with major shareholders, officers, and their relatives must be reorganized to eliminate "arbitrary terms."

- Before: Transactions conducted under arbitrary terms (e.g., purchasing materials at 30% above market price to support an officer’s side business or personal use of company vehicles).

- After: All transactions must be conducted under third-party equivalent terms or eliminated entirely if they serve no clear business necessity.

4.2 Group Management & Consolidation Policy

Management shall define the scope of consolidated subsidiaries based on "effective control." The parent company is commanded to provide:

- Unified Reporting Systems: To ensure accurate, timely data for consolidated financial statements.

- Educational Support: To ensure subsidiaries meet global audit standards and prevent reporting lags.

The transparency of these transactions serves as the ultimate test of the firm's internal monitoring functions.

5. Institutional Monitoring: Internal Audit & Independent Oversight

A successful IPO requires a shift from owner-driven "personal Kessai" to institutionalized oversight. Establishing robust "Checking Functions" is mandatory.

5.1 Requirements for the Internal Audit Function

- Independence: The department must remain independent from all business execution units.

- Universal Monitoring Authority: Internal Audit is granted the authority to monitor any department or subsidiary without prior notice to ensure compliance.

- Strategic Oversight: The function must evaluate whether the company is meeting the social responsibilities expected of a public entity.

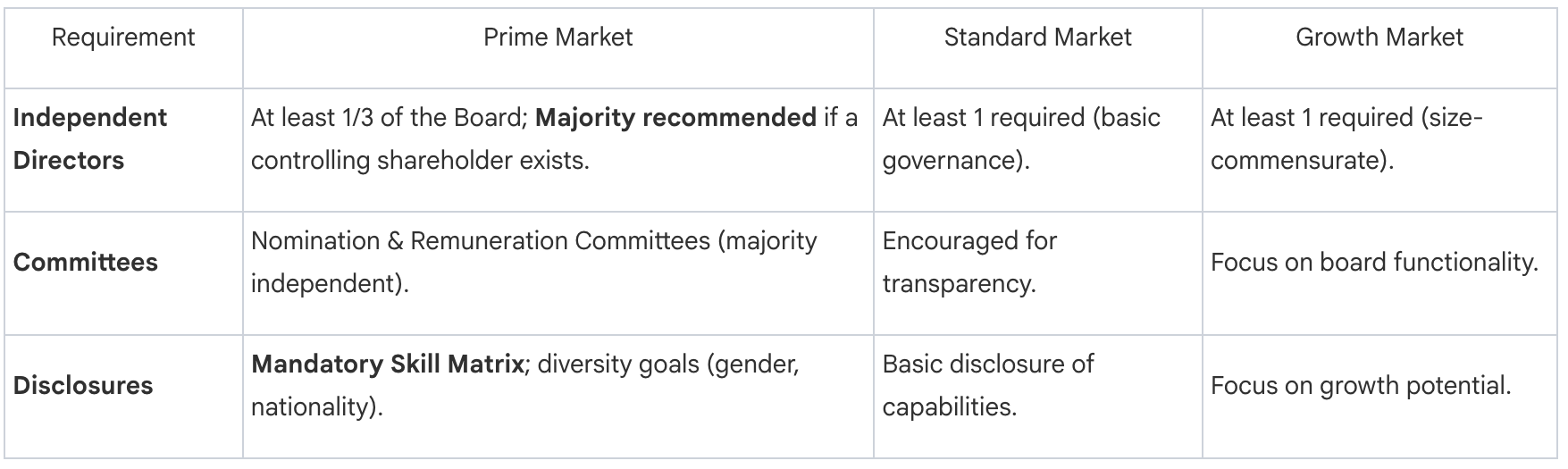

5.2 Independent Director Mandate by Market Segment

6. The Path Forward

An IPO is not the goal, but the start of growth as a social institution. This framework is a continuous process of refinement, preparing the firm for the "Audit of Social Responsibility" required by the public market and the Financial Instruments and Exchange Act. The institutionalization of these structures ensures the company remains worthy of public trust.