Japan’s Bond Market Faces Behind-the-Curve Fears and Seasonal Inversion in Ultra-Long Yields

Japan’s benchmark 10-year government bond yield continues to hover at a elevated level of around 2.7%. Despite recent volatility triggered by geopolitical tensions in the Middle East, shifts in the Bank of Japan’s (BOJ) policy stance, and the fiscal direction of the Takaichi administration, yields have resisted breaking above the 2.8% threshold.

According to a June 26, 2026, report by Sony Financial Group Senior Economist Takayuki Miyajima, market analysts attribute this ceiling to the fact that the bond market's terminal rate assumptions have already largely priced in a level above 2%. Pushing yields significantly higher from this point would require a sharper policy rate hike that explicitly exceeds the BOJ's inflation target—a scenario deemed unlikely at this stage. Additionally, the stabilization of Middle East tensions and a Takaichi supplementary budget that turned out less expansionary than initially feared have helped cap the upside.

'Behind-the-Curve' Concerns Keep Spread Risks Alive

The BOJ’s June policy meeting ultimately passed without causing major waves in the debt market. However, the yield spread between long- and short-term bonds—a key proxy for market anxiety regarding the BOJ falling "behind the curve"—widened slightly following the meeting.

Remarks from Deputy Governor Uchida offered few new clues regarding the future pace of monetary tightening, leaving the market's rate-hike pricing unchanged. Because these concerns have not receded, observers warn that the risk of further widening in the long-short spread remains on the table. Looking at the broader trend, this steepening bias has been building since last October, reflecting market adjustments to the Takaichi administration’s aggressive fiscal policy posture, shifting inflation expectations, and changing supply-demand dynamics.

The 40-Year and 30-Year Yield Inversion: A Seasonal Phenomenon?

A notable anomaly has emerged in the ultra-long sector: the 40-year and 30-year yield spread fell into negative territory in June, resulting in a yield inversion. Rather than a structural breakdown, experts point to a distinct seasonal pattern linked to primary market issuance.

- The PD Discussion Factor: Historically, since the lifting of the negative interest rate policy, this spread has sharply narrowed between May and early July each year. This coincides with rising market anticipation of reduced ultra-long bond issuance ahead of the Ministry of Finance's Primary Dealer (PD) meeting in June.

- Supply-Demand Tightness: The 40-year segment is particularly sensitive to these shifts because its planned issuance volume for this year is already restricted to just one-quarter of the 30-year supply.

- Institutional Buying: On the demand side, reports indicate that some life insurers are beginning to re-enter the ultra-long market now that the wave of investment curbs prompted by last year's spike in yen yields has run its course.

While the inversion may persist in the near term if supply-reduction expectations remain intact, historical patterns show the spread typically widens again in July. This reversal is often driven by a seasonal rise in fiscal expansion expectations, particularly surrounding the government's upcoming policy blueprint. If fiscal risks escalate, the inversion could quickly unwind, likely stabilizing the spread near zero.

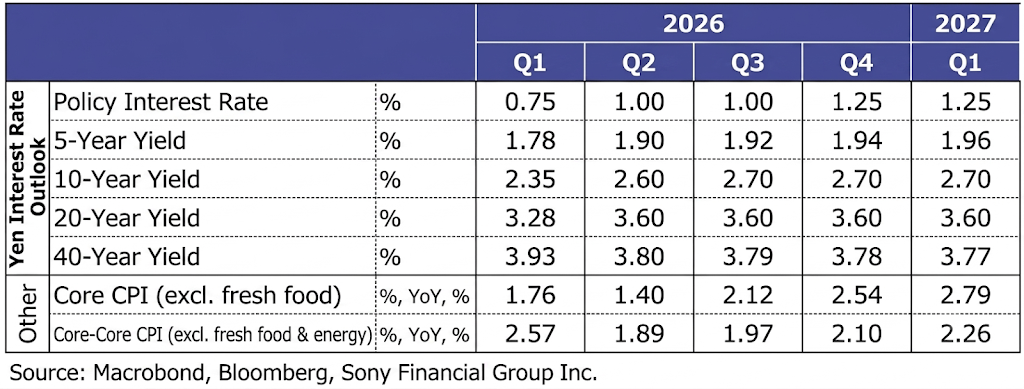

Medium-Term Outlook and Interest Rate Projections

Looking ahead, the 10-year yield is projected to remain firmly supported around 2.7% due to persistent behind-the-curve anxieties. However, if upcoming fiscal policy debates spark deeper deficit concerns, the 10-year yield could test the 2.8% mark. Meanwhile, ultra-long yields are expected to undergo a gradual downward drift due to government and BOJ stability measures, though they will likely remain historically high at around 3.8% due to global yield pressures and domestic fiscal caution.

According to institutional forecasts, the BOJ is expected to take time assessing the inflation outlook and the post-hike financial environment, pointing to a baseline projection for the next rate hike in December 2026.