JGB Yields Eye Peak as Geopolitical Tensions and BoJ Hawkishness Collide

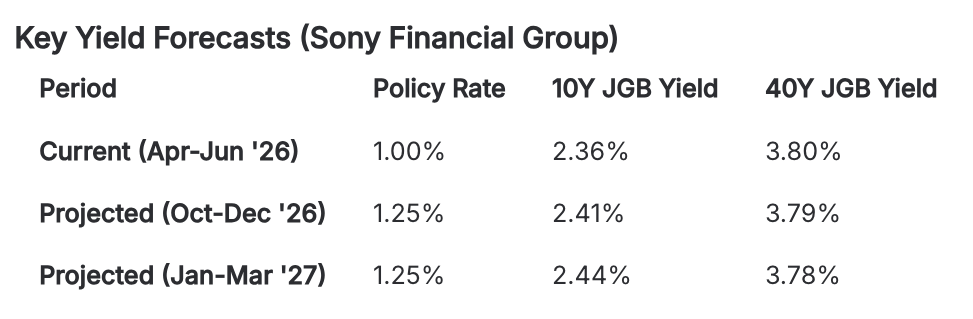

Sony Financial Group’s latest market outlook, released April 9, 2026, suggests that while Japanese Government Bond yields remain on an upward trajectory, the "ultra-long" end of the curve may be nearing a peak.

Senior Economist Takayuki Miyajima highlights a complex landscape where Middle East volatility and a tightening Bank of Japan are pushing rates to multi-year highs, even as technical factors begin to provide a ceiling for long-dated debt.

Long-Term Rates Testing Historical Resistance

The benchmark 10-year JGB yield is currently hovering near 2.44%—a level last seen during the infamous "Trust Fund Bureau Shock." This surge is being driven by two primary engines:

- Energy Inflation: With crude oil prices sustained above $100 per barrel due to prolonged Middle East instability, Japan’s 10-year breakeven inflation rate has climbed to 1.9%.

- A Hawkish BoJ: Following the March policy meeting, the Bank of Japan has maintained a steady drumbeat of hawkish signals. Markets are now aggressively pricing in a terminal rate approaching 2.0%, with Sony Financial’s house view predicting the policy rate will reach 1.25% by the end of 2026.

The Ultra-Long Yield Paradox

Interestingly, while the 40-year JGB yield recently touched a historic 4.0%, the spread between long-term and ultra-long-term bonds has not widened as drastically as it did during the political volatility of early 2026. Analysts point to three stabilizing factors:

- Foreign Demand: At roughly 3.8%, Japanese 30-year yields have surpassed German equivalents (3.5%). When adjusted for currency hedging costs on a USD basis, yields exceed 6%, making JGBs highly attractive to global investors.

- BoJ Supply Dynamics: While the BoJ is reducing purchases in most tenors, it has actually increased its ratio of purchases in the 25-year-plus segment for April, easing supply-demand concerns in the ultra-long zone.

- Regulatory Relief: New accounting proposals from the JICPA, which would exempt long-term holdings from certain impairment rules for life insurers, have reduced the perceived risk of holding long-dated debt.

The Road Ahead: A June Hike in Focus

Sony Financial maintains its "Main Scenario" that the BoJ will implement its next rate hike in June 2026. However, this remains "live" and highly dependent on market stability.

"The key indicator to watch is the VIX Index," the report notes. "If the VIX remains significantly below 20 and oil prices stabilize, the BoJ will likely have the green light. However, if yen depreciation risks subside due to a sudden drop in oil prices, the Bank may find the 'breathing room' to delay until the second half of the year."

Risk Factors: Fiscal Health and Rebalancing

The outlook is not without its pitfalls. The report warns that the government’s continued reliance on gas and utility subsidies is straining the fiscal outlook. Furthermore, if the domestic stock market falters, pension funds may engage in "rebalancing," selling bonds to manage portfolio weights, which could trigger a sudden spike in ultra-long yields.