NetStars Reaches Profitability: Record Transaction Volume and Cost Efficiency Drive First Full-Year Surplus Since Listing

NetStars (Ticker: 5590) announced its consolidated financial results for the fiscal year ended December 31, 2025, achieving its first full year of profitability since its public listing. Driven by a surge in domestic cashless adoption and rigorous technological cost controls, the company outperformed its own forecasts across all key profit metrics.

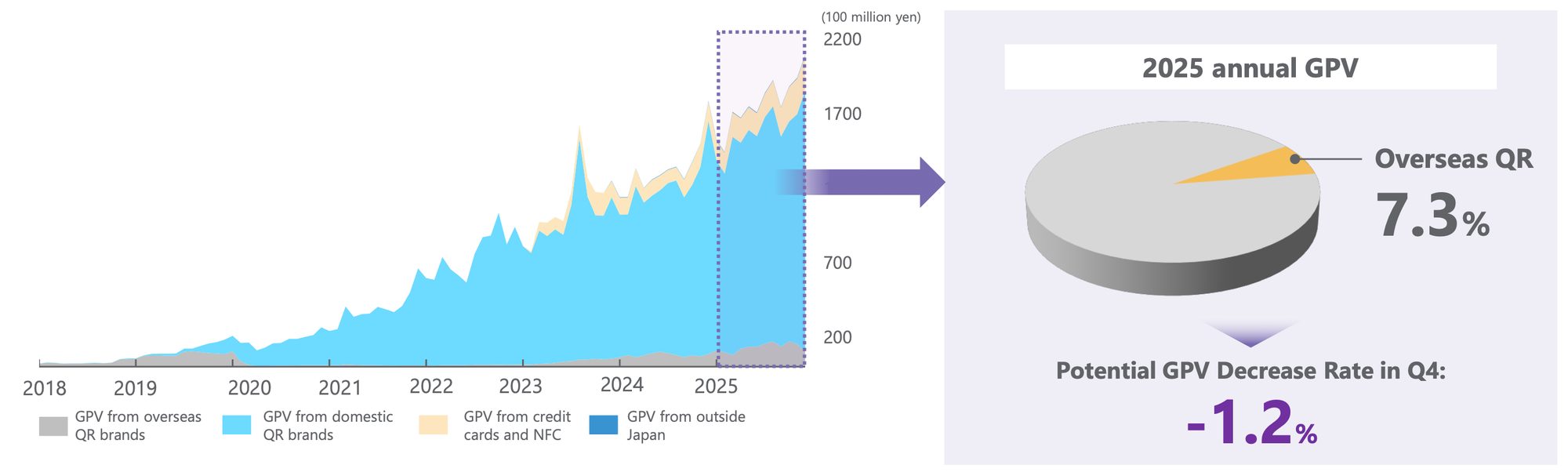

The payment gateway provider reported that Gross Payment Volume (GPV) shattered historical records, exceeding 2.1 trillion yen, a 33.2% increase year-over-year. This scale, combined with the successful deployment of AI-driven infrastructure, allowed NetStars to demonstrate significant operating leverage, proving that its business model has successfully transitioned from a high-burn growth phase to a sustainable, profitable expansion phase.

1. Financial Overview: Breaking the Profit Barrier

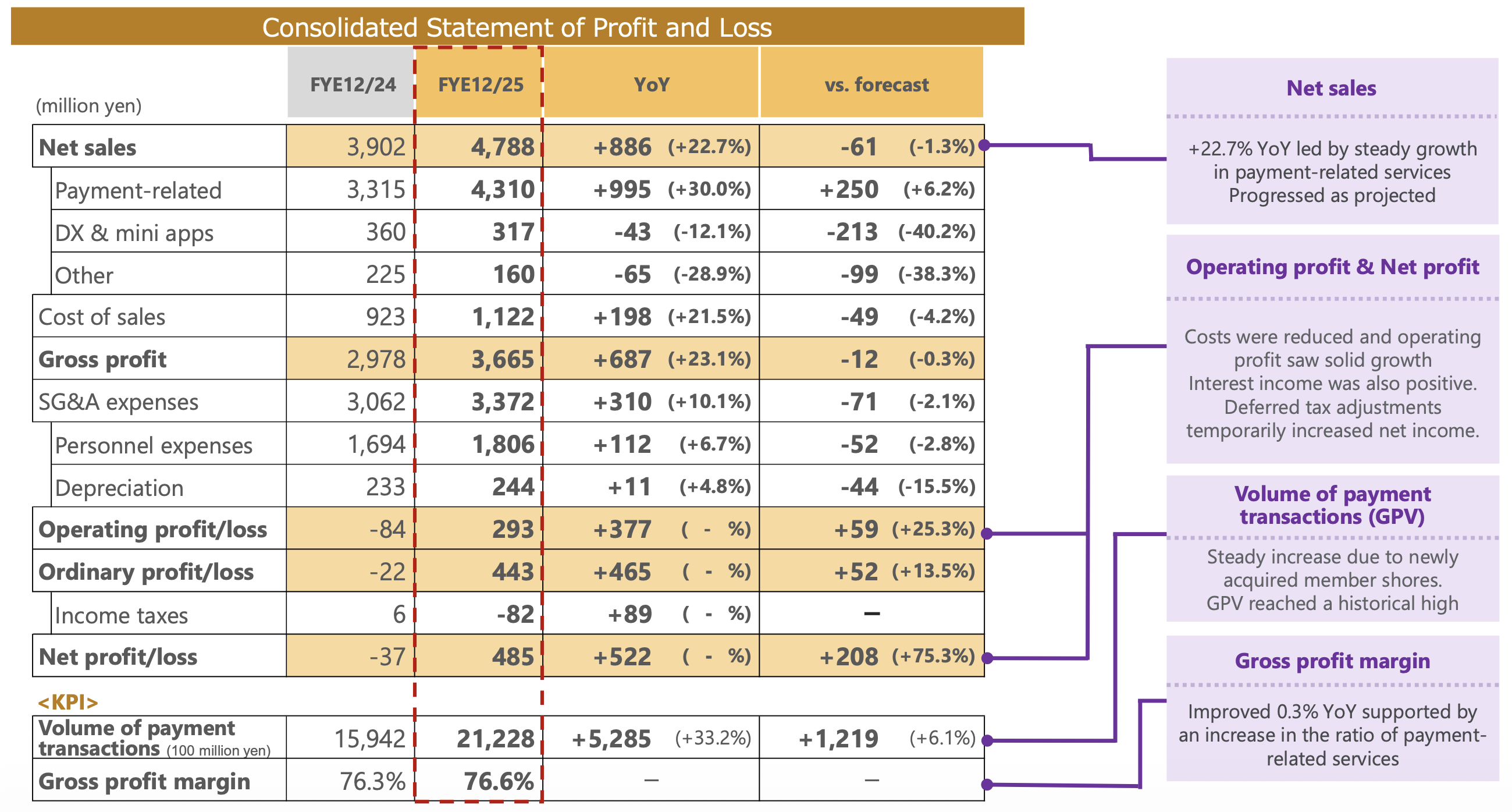

For the fiscal year 2025, NetStars reported net sales of 4,788 million yen, representing a robust 22.7% increase compared to the previous fiscal year. While this figure came in slightly under the company's aggressive forecast by 1.3%, the shortfall was primarily attributed to lower-than-expected revenue in the DX (Digital Transformation) and "Other" segments. However, the core engine of the company—payment-related services—surged, compensating for weaknesses elsewhere and driving the bottom line.

The most significant narrative of this earnings report is the dramatic turnaround in profitability.

- Operating Profit: The company posted an operating profit of 293 million yen, a massive swing from the 84 million yen loss recorded in FY 2024. This result exceeded the company’s forecast by roughly 25%.

- Ordinary Profit: Ordinary profit reached 443 million yen, a year-over-year improvement of 465 million yen.

- Net Profit: Profit attributable to owners of the parent hit 485 million yen, significantly higher than the forecasted 208 million yen, bolstered in part by adjustments for deferred tax assets.

“We achieved our first full-year of profitability since our public listing,” the company stated in its presentation. “GPV growth exceeded the forecast, and as a first step toward building a high-profit business structure, we achieved full-year profitability.”

This financial stabilization was underpinned by a Gross Profit Margin of 76.6%, an improvement of 0.3 percentage points year-over-year. This margin is notably high for the sector and underscores NetStars’ position as a technology platform.

2. The Engine of Growth: GPV and Payment Services

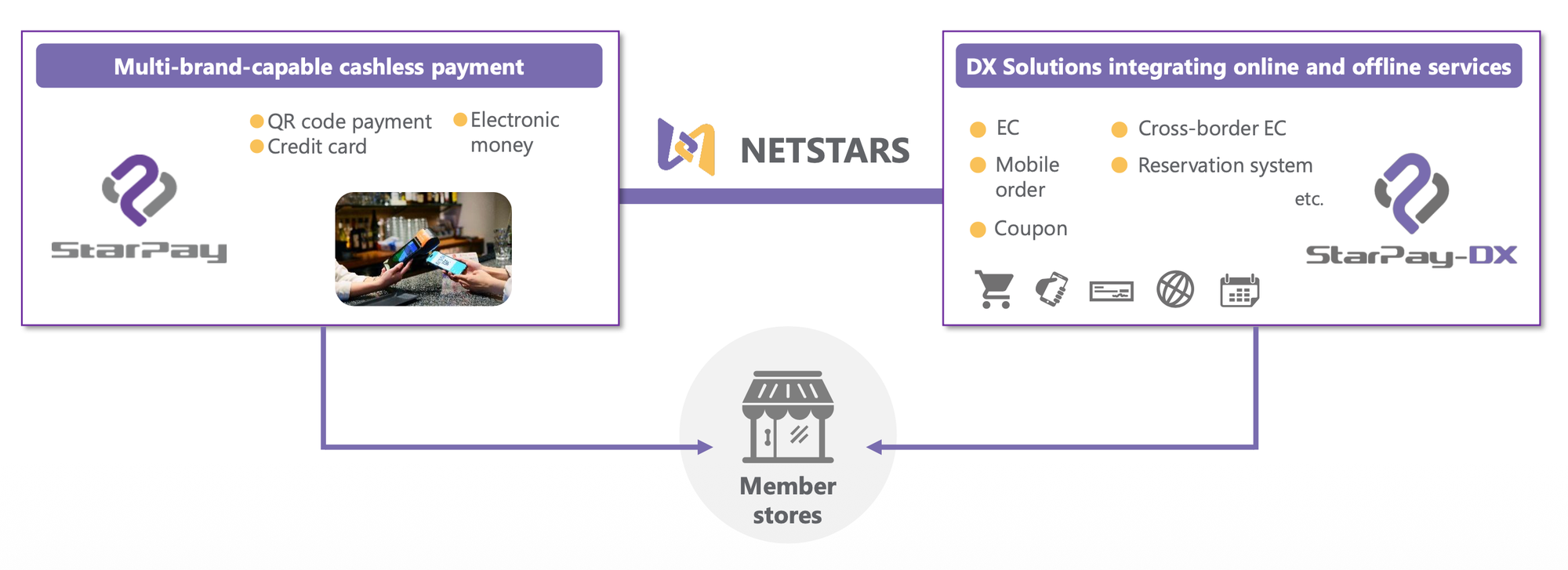

The heart of NetStars’ success lies in its proprietary gateway, "StarPay," which aggregates disparate QR code payment brands into a single device or interface for merchants.

2.1 Segment Performance

- Payment-related Revenue: This segment generated 4,310 million yen, up 30.0% year-over-year. It now accounts for over 80% of total net sales. This growth was driven by the rapid acquisition of new member stores and the deepening penetration of cashless payments in the Japanese retail sector.

- DX & Mini-apps: Revenue contracted by 12.1% to 317 million yen. The company noted that orders for inbound promotions and other DX initiatives did not meet the forecast, signaling a need for strategic realignment in this secondary pillar.

- Terminal Sales: While necessary for onboarding new merchants, terminal sales remain a low-margin component, purposely kept below 10% of total sales to maintain the company’s high overall gross margin.

2.2 Transaction Volume Dynamics

The company’s GPV trajectory remains aggressive. The 2.1 trillion yen figure was achieved despite headwinds in the inbound tourism sector. Specifically, the company noted a decline in Chinese inbound tourists—historically a strong driver of WeChat Pay and Alipay usage.

In Q4, the potential GPV impact from reduced flights between Japan and China was estimated at a negative 1.2%. Chinese-origin payment services saw a decline of approximately 20%. However, this was entirely eclipsed by domestic demand. Domestic QR brands and credit card usage surged, proving that NetStars is no longer solely dependent on inbound tourism but has become a critical infrastructure player for Japanese domestic consumption.

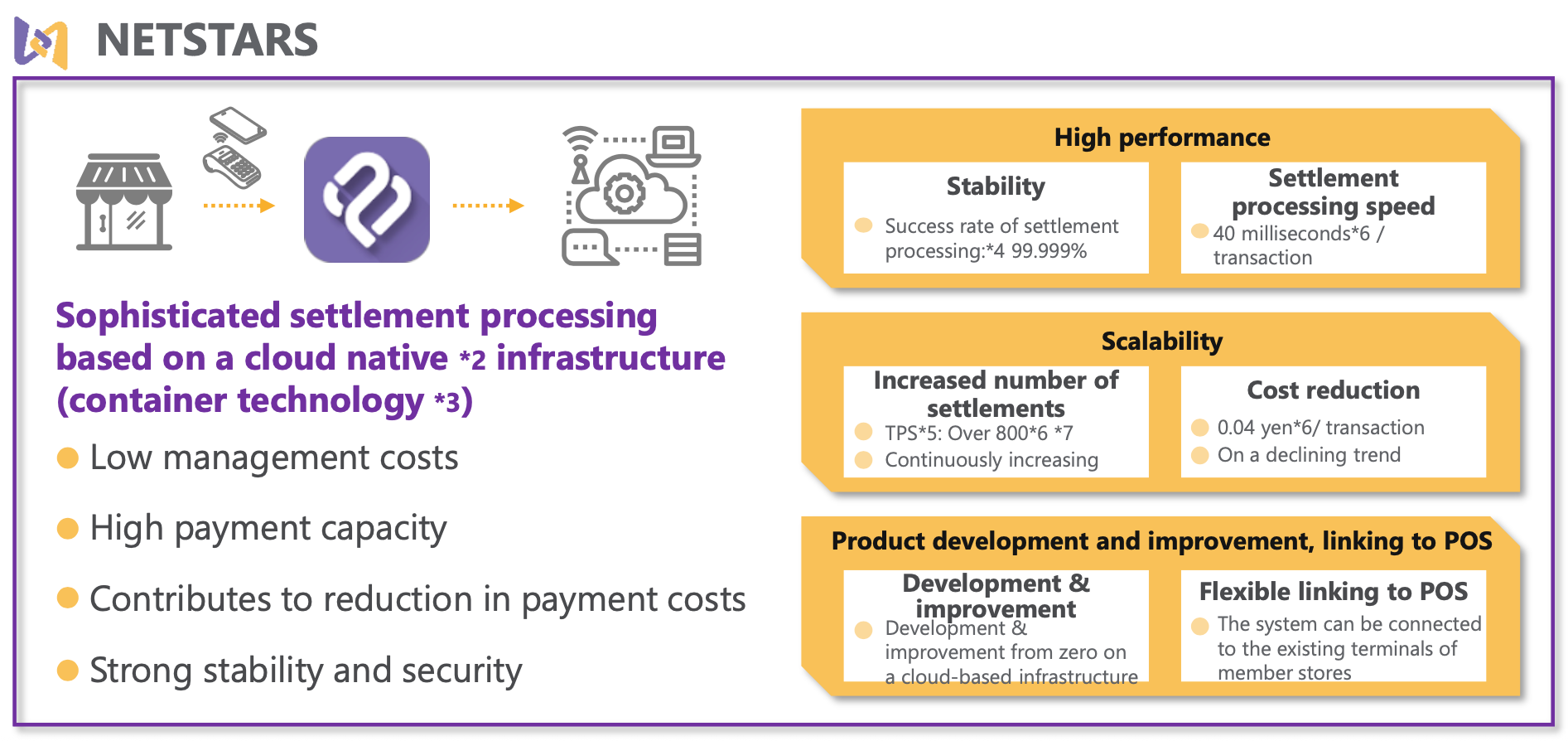

3. Technological Leverage: The "AI" Factor in Cost Control

A standout detail in the FY 2025 report is the divergence between transaction volume growth and expenses. While GPV grew by 33%, dollar-denominated server costs remained largely flat.

NetStars attributes this efficiency to a rigorous technological overhaul and the integration of Artificial Intelligence (AI) into its backend operations.

- Cloud-Native Infrastructure: The company has migrated to a cloud-native infrastructure using container technology. This allows for scalability without linear cost increases.

- AI Implementation: AI is now utilized for server monitoring, resource usage analysis, and code development. By optimizing batch processing and migrating processors from x86 to ARM architecture, NetStars has successfully decoupled its cost base from its volume growth.

- Result: This technological discipline allowed the company to keep SG&A (Selling, General, and Administrative) expense growth to just 10.1%, significantly slower than the 22.7% revenue growth, thereby expanding operating margins.

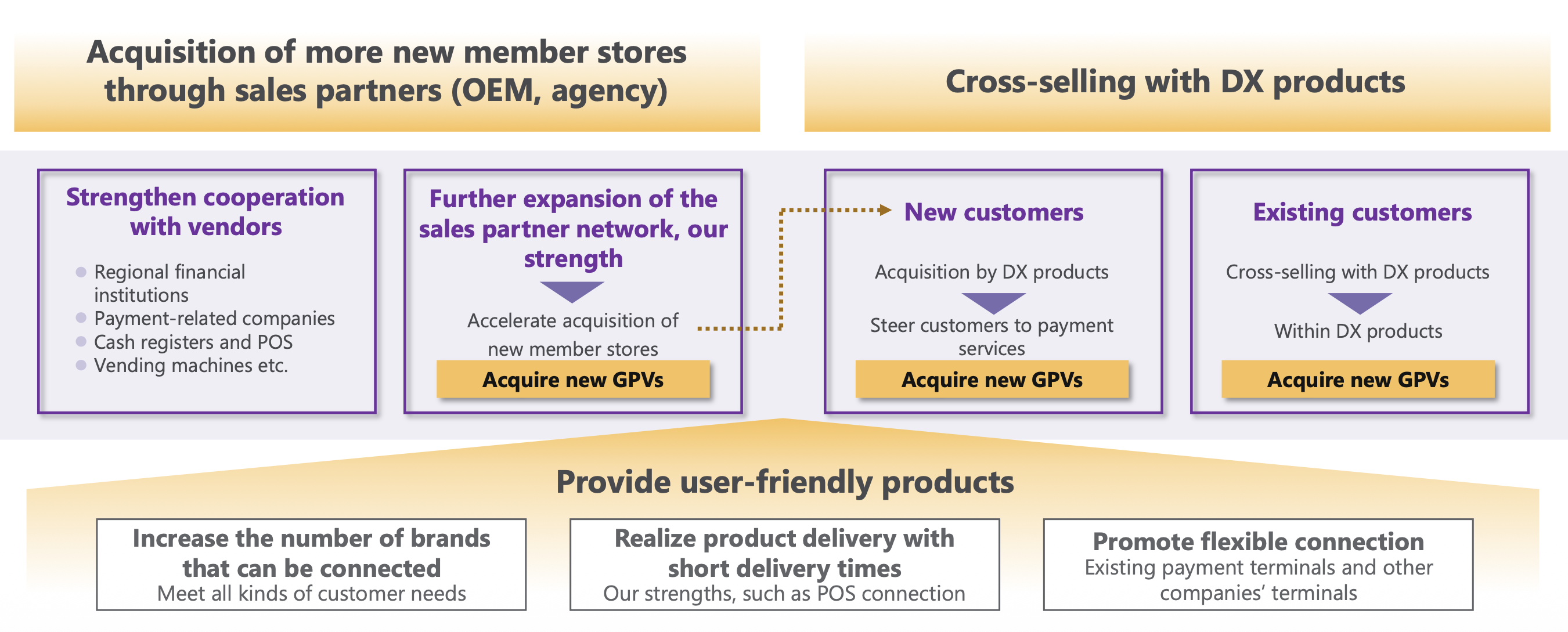

4. Strategic Growth Pillars

NetStars outlined a three-pronged strategy to sustain this momentum through FY 2026 and toward their 2030 vision.

4.1 Multi-Cashless Payment Expansion

The company plans to continue its aggressive expansion of the "StarPay" network. NetStars currently supports over 40 QR code payment brands—one of the largest portfolios in Japan. The strategy involves not just adding more stores, but expanding into new industries.

Historically strong in retail and dining, NetStars is pushing into "non-traditional" cashless sectors such as healthcare, insurance, real estate, and education. The company aims to add "10 or more" new payment brands in the current fiscal year, further cementing its status as the universal gateway for payments in Japan.

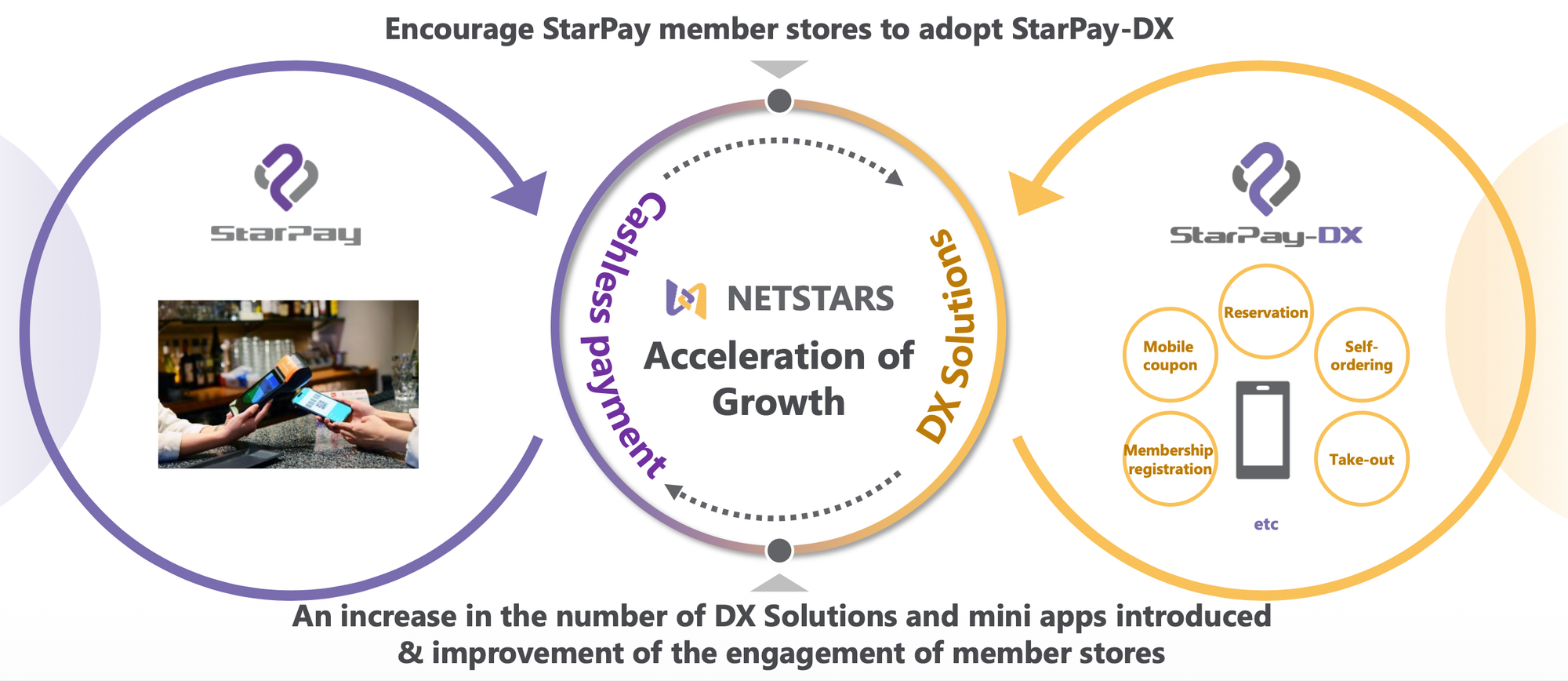

4.2 DX Solutions and "Checkout-Less" Platforms

Despite the segment's revenue dip in FY 2025, NetStars is doubling down on Digital Transformation (DX) products to drive cross-selling. The focus is on labor-saving technologies, a critical need in Japan’s aging, labor-scarce economy.

- Self-Checkouts: The company is deploying self-checkout kiosks and mobile ordering systems for restaurants, movie theaters, and hotels (including a high-profile rollout at Hoshino Resorts' "1955 Tokyo Bay").

- Regional Currencies: NetStars is powering local government digital wallets, such as "Kanagawa Pay" and "NahanchuPay" (Naha City). These projects generate fee revenue and embed NetStars deeply into regional economic infrastructures.

- Mini-Apps: Leveraging super-apps like LINE, NetStars develops mini-apps for clients (e.g., Joshin Denki, BYD) that handle membership, coupons, and reservations, creating a sticky ecosystem beyond simple payments.

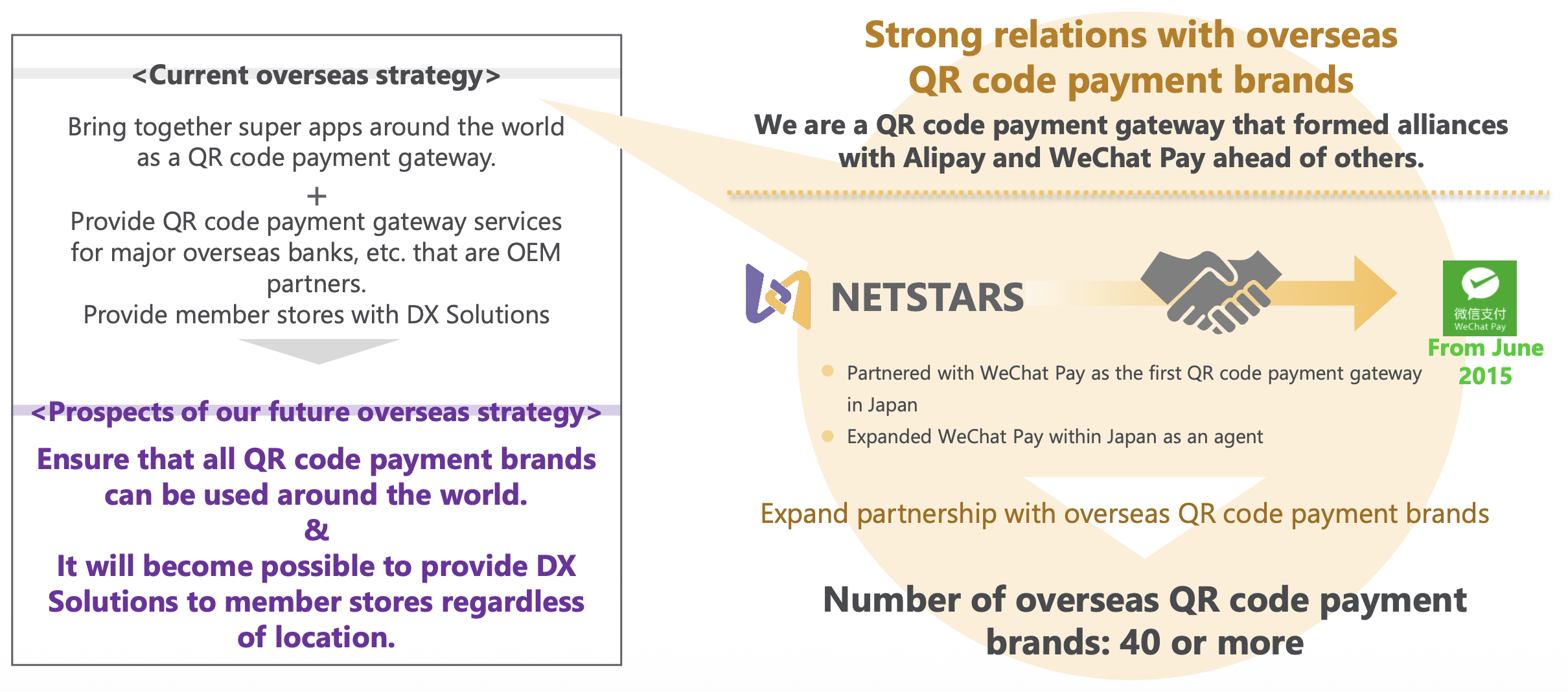

4.3 Overseas Expansion

NetStars is exporting its "Made-in-Japan" payment gateway model.

- JPQR Global: NetStars has been designated as a switching system operator for "JPQR," the Japanese government's unified QR code standard. The company is facilitating cross-border payments, allowing visitors from countries like Indonesia and Cambodia to use their home payment apps at Japanese merchants.

- Middle East & Asia: The company has accelerated its presence in Qatar, where the number of cashless stores has increased by 112% since 2023. Additionally, partnerships are expanding in India (via UPI) and Southeast Asia, aiming to capture both inbound spending in Japan and outbound spending by Japanese travelers.

5. Innovation Topics: Crypto and Gaming

The report highlighted two major innovations launched since late 2025, signaling NetStars’ ambition to operate on the bleeding edge of fintech.

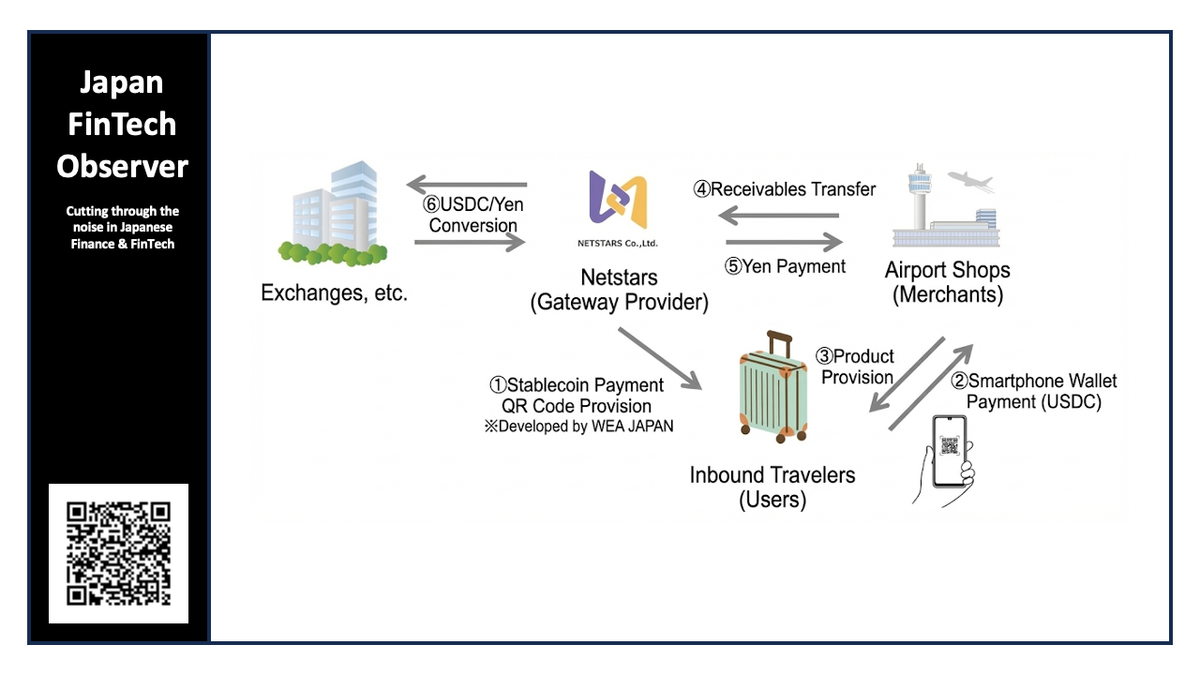

5. 1 Stablecoin Payments (USDC)

In a Japanese first, NetStars successfully conducted a pilot program at Haneda Airport Terminal 3 accepting USDC (USD Coin) for in-store payments. This system allows users to pay directly from MetaMask wallets, with the merchant receiving Japanese Yen. This bridges the gap between Web3 assets and real-world retail without requiring merchants to handle cryptocurrency directly.

5.2 StarPay-Entertainment

Responding to the "New Smartphone Law" (Act on Promotion of Competition for Specified Smartphone Software), NetStars established a subsidiary to handle out-of-app billing for smartphone games. This service allows game publishers to bypass traditional app store payment rails (and their high fees), offering a direct payment system for users. This represents a significant new revenue stream potential in the high-volume gaming market.

6. Forecast for FY 2026: Continuing the Upward Trajectory

Looking ahead, NetStars issued a bullish forecast for the fiscal year ending December 31, 2026. The company expects the "virtuous cycle" of increasing scale and stable costs to continue.

- Net Sales: Forecasted to reach 5,760 million yen, a 20.3% increase.

- GPV: Expected to hit 2.54 trillion yen, a 20.0% increase.

- Operating Profit: Projected to nearly double to 500 million yen (+70.8%).

- Ordinary Profit: Forecasted at 707 million yen (+59.7%), bolstered by expected increases in interest income due to the rising interest rate environment in Japan.

The company plans to maintain a zero-dividend policy for FY 2026, opting instead to reinvest profits into growth opportunities. Key investment areas include recruiting talent, upgrading POS systems for new large-scale clients, and furthering DX product development. Despite these investments, the company projects SG&A expenses will grow by only 8.8%, furthering the narrative of operational efficiency.

7. Long-Term Vision: The Road to 2030

NetStars concluded its report by reiterating its "Ideal State for 2030." The targets are ambitious:

- GPV: Over 6 trillion yen.

- Consolidated Sales: Over 12 billion yen.

- Gross Profit Margin: Maintaining 70%+.

- Operating Profit Margin: Reaching 25%+.

The company envisions itself not just as a payment processor, but as a comprehensive infrastructure provider that enriches the flow of money through society.

8. Market Context

NetStars operates in a highly favorable macro environment. Japan’s cashless payment ratio stood at 42.8% in 2024, significantly trailing peers like South Korea and China. The Japanese government has set a target of 80% cashless adoption, providing a long runway for growth. Furthermore, QR code payments are the fastest-growing segment of this market, with a CAGR of 120% from 2018 to 2024, compared to just 10% for credit cards.

As a pioneer that formed alliances with WeChat Pay and Alipay as early as 2015, NetStars has successfully leveraged its first-mover advantage to build a moat of 40+ brands and 400,000+ member stores.

9. Conclusion

The FY 2025 earnings report serves as a validation of NetStars' IPO promise. By navigating the volatility of the post-pandemic tourism recovery and successfully capitalizing on domestic cashless trends, the company has proven its resilience. The pivot to profitability, achieved while maintaining 20%+ top-line growth, suggests that NetStars has found a sustainable formula.

With new frontiers in stablecoins and gaming billing opening up, and a disciplined approach to cost management via AI, NetStars appears well-positioned to capitalize on Japan’s inevitable march toward a cashless society. Investors will be watching closely to see if the company can maintain its technological edge while executing its ambitious overseas and DX strategies in 2026.