Real Estate: Zero Energy Renovation (Zenobe) & Portfolio Valuation

To achieve carbon neutrality by 2050, Japanese financial institutions are promoting "Zero Energy Renovation (Zenobe) Finance" to upgrade the environmental performance of aging building stocks. This requires a collaborative effort by major banks to address economic hurdles and technical constraints that currently prevent owners from retrofitting older properties. Financial institutions aim to move beyond rigid statutory lifespans by developing evidence-based screening and "connoisseurship" to evaluate a building's true green potential. Market data suggests a growing "green premium," where tenants are increasingly willing to pay higher rents for sustainable, energy-efficient office spaces. Ultimately, the initiative seeks to establish a new investment ecosystem where decarbonization efforts are directly reflected in real estate valuations and asset liquidity. Successful implementation requires standardized CO2 disclosure and the widespread adoption of energy certifications to foster trust among global investors.

1. The Strategic Imperative: Transitioning from Depreciation to Appreciation

The institutional real estate market is facing a structural crisis of obsolescence. In Japan’s major metropolitan centers, the "volume zone" of office stock—buildings aged between 20 and 40 years—accounts for approximately 40% to 50% of total floor area. Traditional valuation models, which rely on rigid linear depreciation, are fundamentally failing to price the "Stranded Asset" risks inherent in this stock. As global disclosure mandates tighten, assets with poor environmental performance face rapid liquidity discounts and valuation write-downs.

However, this 20–40 year window represents the "Economic Sweet Spot" for strategic intervention. Because these assets are entering major equipment replacement and maintenance cycles, the capital required for high-performance upgrades can be absorbed into existing CAPEX budgets. By shifting from standard maintenance to Zenobe (Zero Energy Renovation), owners can bridge the gap between necessary repairs and value-accretive upgrades, though they must first scale three critical "Execution Walls":

- Economic Rationality: The "Split Incentive" deadlock remains the primary barrier; owners bear the CAPEX for efficiency while tenants capture the utility savings. Without a mechanism to translate energy performance into Net Operating Income (NOI) expansion, the ROI remains opaque.

- Technical & Execution Constraints: Performing "in-place" renovations in occupied buildings carries high operational risks, including tenant disruption and the discovery of "hidden defects" like asbestos or structural fatigue that can blow out project timelines.

- Immature Market Environments: While global mandates are clear, local tenant willingness to pay for "Green" features is still developing, and the friction of navigating subsidy applications and BELS/ZEB certifications remains high for non-specialized owners.

2. The Zenobe Methodology: Technical Metrics as Financial Indicators

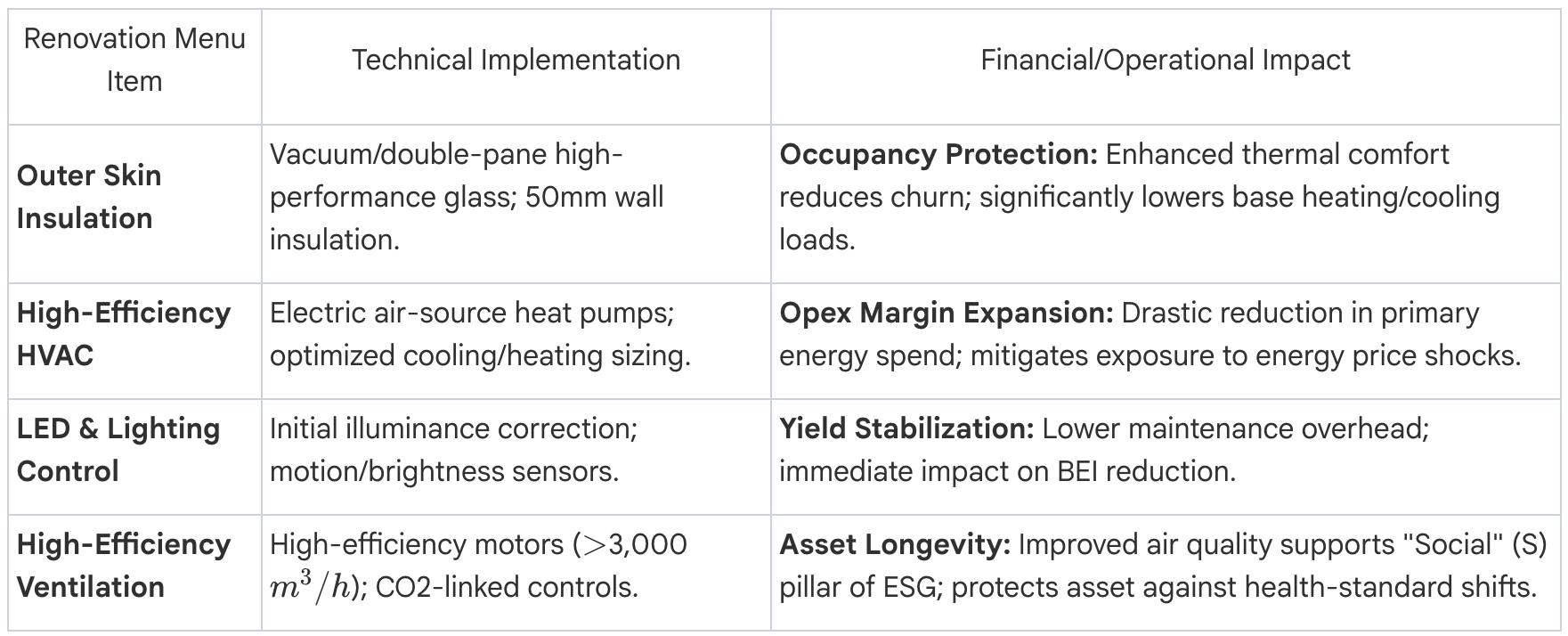

For the sophisticated investor, technical energy metrics like the Building Energy Index (BEI)—the ratio of design primary energy consumption to standard consumption—are now fundamental proxies for financial durability. A lower BEI is a shield against utility price volatility and future carbon taxation.

The following "Renovation Menu" maps technical interventions to their impact on operational margins:

A critical component of this methodology is "Operational ZEB." This moves beyond static design values to incorporate tenant behavior. The implementation of natural ventilation notification lamps is essential; these systems prompt occupants to utilize manual windows during optimal weather, leveraging "passive" design to drive real-world performance. This synthesis of hardware and human behavior ensures the building hits its performance targets in practice, not just on paper.

3. Reconciling CAPEX: The "Green Premium" and Tenant Economics

The high initial CAPEX of Zenobe is increasingly offset by measurable rental growth. Evidence from Tokyo’s 23 wards reveals a 7.2% rental premium for certified green buildings. This is supported by shifting tenant demographics; as of 2025, 52.3% of corporate tenants expressed a willingness to accept higher costs for environmentally superior space.

Beyond the "Green Premium," three primary value drivers justify the investment:

- Wellness & Productivity: High-insulation environments and superior indoor air quality are directly linked to worker productivity. For corporate occupiers, the "Social" value of a Zenobe asset facilitates talent retention, justifying higher base rents.

- Resilience & Business Continuity Planning (BCP): Integrating solar PV and battery storage allows a building to maintain critical functions during grid failures. This resilience profile attracts high-credit tenants who view BCP as a non-negotiable leasing requirement.

- Leasing Velocity: High-performance assets consistently experience shorter vacancy periods. In a market where institutional mandates forbid the leasing of high-carbon assets, Zenobe properties avoid the "liquidity trap" that plagues aging, un-renovated stock.

4. The New Valuation Paradigm: Integrated Cash-Flow vs. Separated Evaluation

To accurately price Zenobe assets, the financial sector must abandon the Separated Evaluation Approach, which treats land and building as distinct entities and depreciates the building toward a 50-year statutory limit. This antiquated view ignores the reality that a renovated building’s economic life can far exceed its tax-driven "useful life."

Zenobe Finance advocates for an Integrated Evaluation Approach, characterized by:

- Cash-Flow Synergies: Treating land and the high-performance building as a single, inseparable income-generating unit.

- Terminal Value Preservation: Valuing the asset based on its Exit Cap Rate in a 2050 Net Zero economy. Assets that are "Zenobe-ready" will trade at a significant premium to peers that face a "Brown Discount" or heavy terminal CAPEX requirements.

- Challenging Statutory Constraints: While statutory life is 50 years for RC offices, other benchmarks—such as the 90-year life considered in public loss compensation—demonstrate that with proper Zenobe intervention, the residual value of the structure remains high, significantly improving the Internal Rate of Return (IRR).

Major Japanese institutions, including DBJ, Mizuho, SMBC, MUFG, and SMTB, are now evolving their roles. They are moving toward Evidence-based Screening and Potency Assessment, evaluating a building’s location and renovation potential as the primary indicators of creditworthiness rather than simple chronological age.

5. Institutional Implementation: Aligning with ISSB and Global Standards

For Zenobe projects to attract global institutional capital, they must be elegible within the International Sustainability Standards Board (ISSB) framework. Global investors view BELS and ZEB certifications as a "Global Currency"—a standardized proof of value that mitigates the risk of "greenwashing."

To establish market credibility, asset managers should follow this 4-point suggestion plan:

- Visualization: Disclose CO2 reduction based on rigorous "Design Values" (BEI) to provide a transparent performance baseline.

- Certification: Aggressively pursue BELS certifications to validate energy efficiency to international lenders.

- Appraisal Integration: Actively collaborate with appraisers to ensure "Carbon Value" and risk-reduction features are explicitly quantified in official valuation reports.

- Reporting Consistency: Ensure all sustainability reporting is strictly aligned with ISSB-governed standards to maintain institutional trust and secondary market liquidity.

6. Case Study Synthesis: The "Green Building Ecosystem" Model

The implementation of Zenobe at scale requires a multi-stakeholder "Ecosystem" to distribute risk. The Green Building Ecosystem 2 fund, capitalized at approximately 65 Billion Yen, provides a benchmark for this collaborative approach.

The distribution of risk across the nine participating entities is structured as follows:

- Lenders: SMBC and MUFG provide senior debt based on integrated cash-flow valuations.

- Investors (Equity): Kyushu Electric, Nikken Sekkei (serving as both lead architect and equity partner), Development Bank of Japan (DBJ), Fuyo General Lease, Mizuho Lease, and Sumitomo Mitsui Trust Bank (SMTB).

- Asset Management: DBJ Asset Management (DBJAM).

A primary application of this model is the Nikken Sekkei Korakuen Building (34 years old). This project targets a ZEB-Oriented status (BEI \le 0.6) and aims for a 50% reduction in operational energy. The project focuses on Space Value Enhancement, converting underutilized areas into high-margin coworking hubs and lounges. This demonstrates that Zenobe is not a "cost" of compliance, but a strategic repositioning that increases NOI through both reduced Opex and enhanced space-use efficiency.

7. Strategic Conclusion: The Future of Real Estate Asset Management

Zero Energy Renovation is the only viable strategy for preserving the terminal value of real estate in a carbon-constrained market. For the 20–40 year office stock, the transition from a "Stranded Asset" to an institutional-grade investment requires a fundamental shift in how we perceive the relationship between technical performance and financial return.