Seven Bank Records Revenue Growth Amid Net Income Compression in FY2025

The fiscal year ended March 31, 2026, was characterized by a distinct divergence for Seven Bank. While the institution successfully accelerated its top-line momentum, reaching record levels of ordinary income, the transition to the bottom line revealed significant friction. This divergence highlights a complex operating environment where the domestic banking engine’s robust performance, marked by a rise in non-consolidated profitability, was overshadowed by compression at the consolidated level. The results suggest that while the core Japanese operation remains highly efficient, the broader group is absorbing higher structural costs and investment burdens from its subsidiaries or international ventures.

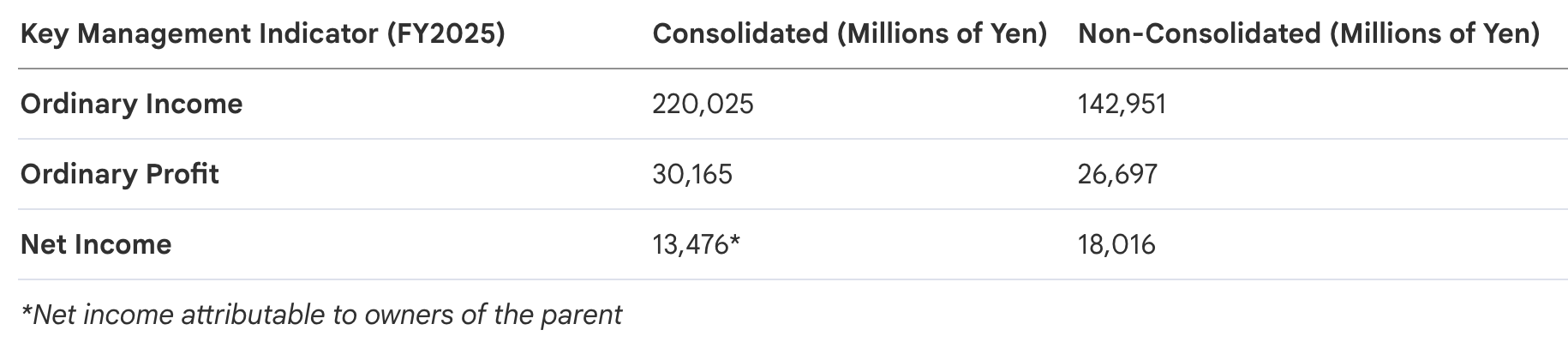

The most pressing concern for shareholders is the 26% decline in Consolidated Net Income, which slid from 18,221 million yen in FY2024 to 13,476 million yen. Critically, this compression is exclusively a consolidated phenomenon; on a non-consolidated basis, net income actually grew from 17,657 million yen to 18,016 million yen. This suggests that the bank’s domestic core is subsidizing growth or navigating headwinds within its subsidiaries. For investors, the consequence is clear: Seven Bank is currently a high-performance domestic engine powering a group-wide phase of transition and heavy reinvestment.

To understand the resilience of the core business, one must examine the specific mechanics of the bank’s revenue generation and its response to a shifting interest rate landscape.

1. Revenue Analysis: Yield Expansion and Interest Margin Dynamics

In a rising rate environment, the strategic management of interest-earning assets has become Seven Bank’s primary growth lever. The institution has aggressively capitalized on market shifts, significantly enhancing its yield profile through a disciplined focus on high-return retail lending and a more productive securities portfolio.

The efficiency of the bank's interest-earning assets reflects a sharp upward trajectory:

- Yield Expansion: The average yield on interest-earning assets surged from 3.21% in FY2024 to 4.61% in FY2025.

- Anomalous Yield Activity: Notably, the yield on "Due from banks" spiked from 7.68% to a staggering 42.53%. This headline-grabbing anomaly suggests high-yield activity in specific subsidiary channels or specialized international operations that warrants close monitoring.

- Interest Margin Expansion: While the cost of liabilities rose from 0.10% to 0.26%, the yield on assets grew at a far steeper rate. Consequently, the total interest margin expanded by 124 basis points, reaching 4.35%.

Within the non-consolidated portfolio, the bank maintains a bifurcated strategy:

- Stability of Loan Yields: The loan portfolio continues to serve as the bank's high-yield anchor. Despite broader market volatility, the yield on loans remained remarkably steady, shifting only nominally from 14.80% to 14.79%. This consistent double-digit yield provides a reliable foundation for net interest income.

- Growth in Securities Yields: The securities portfolio demonstrated greater sensitivity to market conditions, with yields rising from 0.19% to 0.63%. This 44-basis-point increase suggests a successful rotation into higher-coupon instruments, improving the productivity of the bank’s investment capital.

While these revenue drivers are performing robustly, maintaining the high-tech infrastructure required to capture this income necessitates a substantial and growing operational commitment.

2. Operational Overhead: Analyzing the General and Administrative (G&A) Burden

Seven Bank’s specialized, ATM-heavy model makes General and Administrative (G&A) expenses a critical strategic indicator. Because the bank relies on a vast physical and digital network rather than a traditional branch system, depreciation and outsourcing are the primary barometers of its operational health and technological reach.

Non-consolidated G&A expenses rose to 81,477 million yen in FY2025. A breakdown of these costs reveals a highly concentrated expenditure profile:

- Business Outsourcing Expenses: 27,152 million yen

- Depreciation of Fixed Assets: 25,048 million yen

- Salary and Allowances: 7,555 million yen

Together, these three categories account for 73.3% of the bank's total G&A burden. This structure underscores a lean human capital model that is heavily leveraged toward technical infrastructure and third-party partnerships.

The 2,758 million yen year-over-year increase in total expenses was driven largely by a 1,939 million yen rise in depreciation and a 687 million yen boost in advertising expenses. The latter is particularly telling; the increased marketing spend aligns with the bank’s strategic pivot toward individual lending, where higher customer acquisition costs are a prerequisite for capturing high-yield retail market share. While these outlays weigh on short-term net income, they represent an aggressive attempt to secure the bank's future competitive position.

Beyond infrastructure costs, the bank’s ultimate stability is tied to the quality of its expanding credit portfolio.

3. Credit Portfolio and Risk Profile: Loan Growth and Asset Quality

Seven Bank has accelerated its shift toward individual lending, a high-margin strategy that demands rigorous credit oversight. The ability to scale this book without deteriorating asset quality remains the most significant test of the bank's risk management framework.

The loan book expanded substantially, with year-end balances climbing by 18,694 million yen to a total of 79,394 million yen. This growth is almost entirely concentrated in the "Individual" sector, which represents 99.8% of total loans. This confirms that consumer overdrafts and card loans have become the bank’s primary engine for lending growth.

Despite this expansion, the bank’s risk profile appears well-contained:

- Risk-Monitored Loans: On a consolidated basis, risk-monitored loans remained effectively flat at 1,167 million yen, compared to 1,163 million yen the previous year. On a non-consolidated basis, the figure stands at a negligible 177 million yen.

- Proactive Credit Buffers: The "Allowance for Credit Losses" was increased by 1,040 million yen year-over-year. Given that risk-monitored loans did not see a corresponding spike, this move should be viewed as a sophisticated, proactive measure. Management is building a capital cushion today to offset the inherent risks of a much larger, retail-heavy loan book tomorrow.

The bank’s capacity to absorb these potential credit risks is further bolstered by an exceptionally robust capital position and a stable, strategic ownership structure.

4. Capital Adequacy and Ownership Structure

For any financial institution, the capital adequacy ratio (CAR) and shareholder stability are the ultimate metrics of long-term viability. High CAR levels provide the necessary buffer against market shocks, while committed "anchor" investors ensure strategic continuity.

Seven Bank continues to maintain capital levels that far exceed regulatory mandates:

- Consolidated CAR: 29.91% (up from 29.13% in FY2024).

- Non-Consolidated CAR: 42.75% (up from 41.50% in FY2024).

These figures demonstrate that the bank is effectively growing its capital base even as it navigates profit compression and significant infrastructure reinvestment.

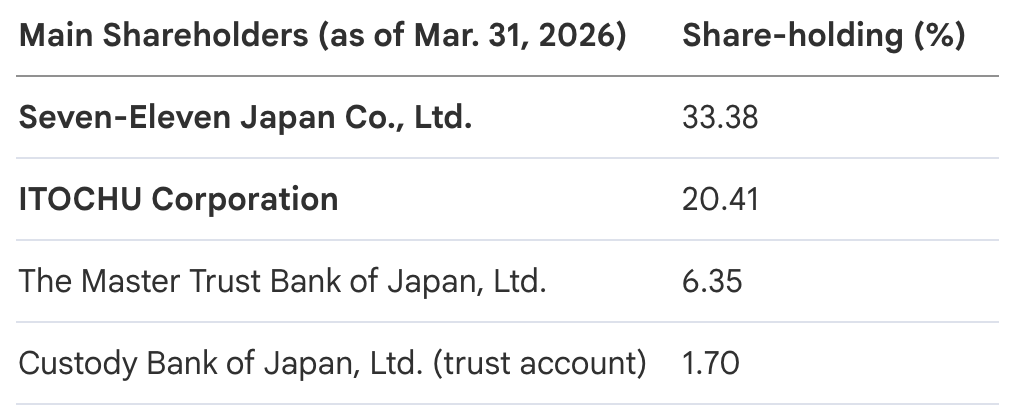

The bank’s ownership remains dominated by strategic corporate partners, ensuring that management is insulated from short-term market pressures and aligned with a retail-centric long-term vision.

With Seven-Eleven Japan and ITOCHU Corporation controlling over 53% of the shares, the bank possesses a stable foundation for its high-yield, tech-driven model.

In summary, Seven Bank enters the next fiscal year as a high-yield, exceptionally well-capitalized institution that is successfully navigating consolidated profit compression by aggressively strengthening its domestic profit engine and expanding its consumer credit footprint.