Sompo Holdings Lifts Full-Year Outlook to Record High as 3Q Profit Surges 47% on Underwriting Improvements

Sompo Holdings delivered a robust set of third-quarter results for fiscal year 2025, posting a sharp increase in profitability driven by improved underwriting margins in its domestic property and casualty (P&C) business and sustained growth in overseas operations.

Buoyed by lower-than-expected natural catastrophe losses and strong investment returns, the insurer has revised its full-year adjusted consolidated profit guidance upward by ¥40.0 billion to a record-breaking ¥480.0 billion.

Key Financial Highlights (3Q YTD FY2025)

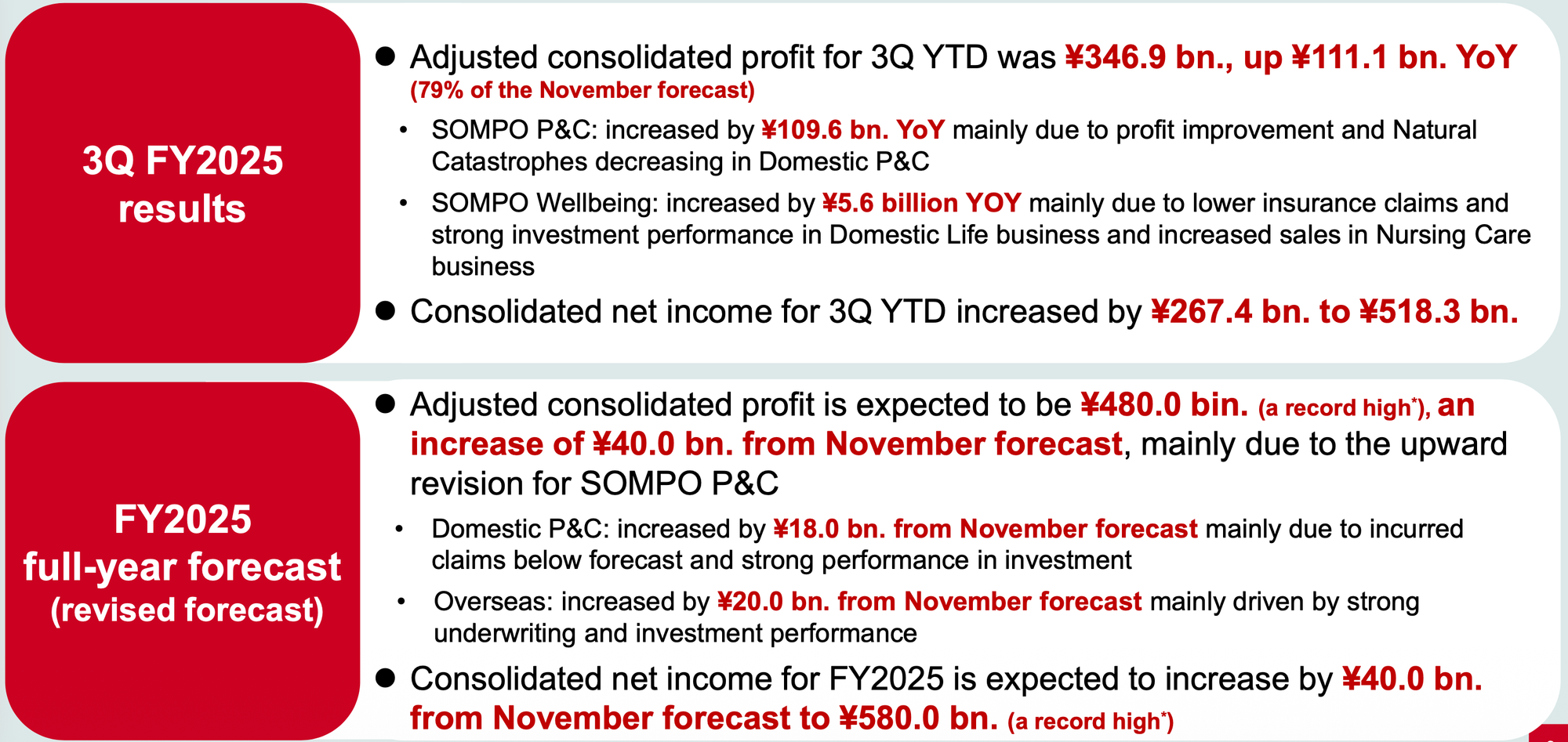

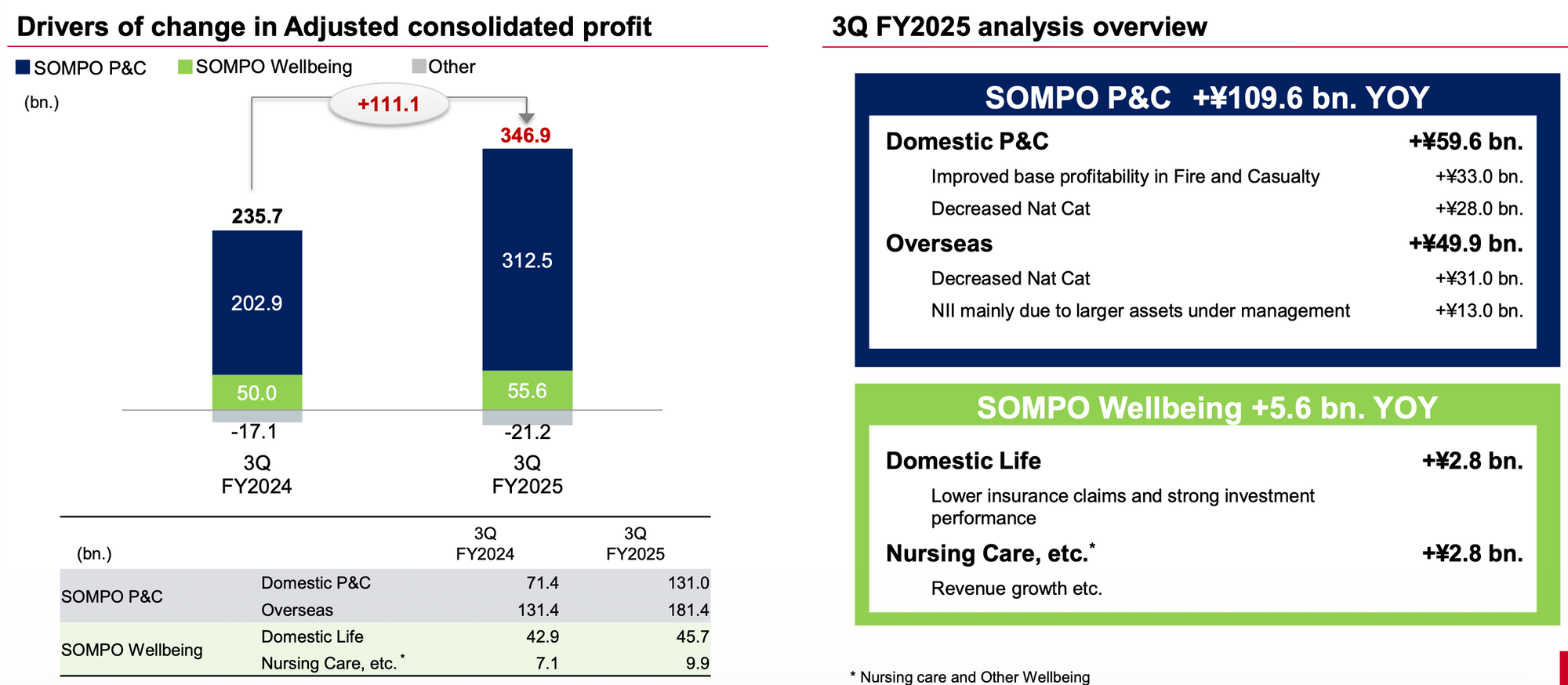

- Adjusted Consolidated Profit: ¥346.9 billion (+¥111.1 billion YoY).

- Consolidated Net Income: ¥518.3 billion (+¥267.4 billion YoY).

- Progress: 79% of the previous November forecast achieved.

- Full-Year Forecast (Revised): Adjusted consolidated profit raised to ¥480.0 billion; Net income raised to ¥580.0 billion.

Segment Performance

Sompo P&C (Domestic Business)

The domestic unit was the primary driver of the quarter's outperformance. Adjusted profit for Sompo Japan climbed ¥59.2 billion to ¥130.4 billion. This turnaround was attributed to two main factors:

- Improved Base Profitability: Product revisions in automobile and fire insurance, alongside reduced expense ratios, bolstered margins.

- Benign Weather: A significant year-over-year decrease in natural catastrophe losses contributed approximately ¥37.0 billion to the bottom line improvement.

Overseas Insurance (Sompo International)

The overseas segment continued its expansion, posting an adjusted profit of $1.20 billion, up $355 million year-over-year. Top-line growth remained healthy with insurance revenue up 7%, while the combined ratio (discounted) improved by 7.1 points to 82.8%, reflecting disciplined underwriting in commercial lines and reduced catastrophe impacts. Net investment income also saw a boost, rising to $1.2 billion due to higher assets under management and resilient yields.

Sompo Wellbeing

The Wellbeing segment, comprising Domestic Life and Nursing Care, contributed steady gains.

- Himawari Life: Adjusted profit rose ¥2.8 billion to ¥45.7 billion, supported by lower insurance claims payments and strong investment income.

- Nursing Care: Despite rising labor costs due to improved remuneration, the division increased adjusted profit to ¥8.6 billion (+¥2.2 billion YoY), driven by higher occupancy rates (94.0%) and sales growth.

Capital & Strategic Updates

Sompo Holdings continues to execute on capital efficiency strategies. The company reduced strategic shareholdings by ¥223.4 billion in the third quarter alone, signaling potential to outperform its reduction targets. Financial soundness remains robust, with an Economic Solvency Ratio (ESR) of 258.3% as of the end of December 2025, factoring in the impact of the Aspen acquisition.

Outlook

Management expressed confidence in the remainder of the fiscal year, revising the full-year net income forecast to a record high of ¥580.0 billion. The upward revision reflects the continued suppression of incurred claims in the domestic business and strong underwriting and investment momentum in overseas markets.