The Ascendance of the Hokkoku Digital Banking Overdraft

Within the contemporary Japanese financial landscape, digital transformation has become a fundamental survival mechanism for the regional banking sector. The Hokkoku Digital Banking Overdraft service represents this shift, moving beyond incremental product improvement to redefine how regional financial institutions facilitate capital velocity for local enterprises. This comprises a fundamental reimagining of liquidity management for the modern era.

As a core extension of the "Hokkoku Digital Banking" ecosystem, this service holds the distinction of being the inaugural initiative of its kind among Japanese regional banks. Its significance is further elevated by the institutional evolution of its parent company; on October 1, 2025, Hokkoku Financial Holdings officially rebranded as CCI Group. From a strategic perspective, this "de-banking" of the corporate identity—transitioning from a traditional "Financial Holding" structure to a "Group" moniker—signifies a pivot toward a tech-first, platform-centric ecosystem. This evolution provides the institutional framework necessary to sustain the digital-native financial solutions required by today’s corporations and sole proprietors.

1. The 100 Billion Yen Growth Trajectory

In the traditionally conservative regional markets of Ishikawa and Toyama, rapid loan balance growth serves as the primary validator for digital adoption. Achieving scale in these segments typically requires years of relationship-based, face-to-face negotiation. The trajectory of the Hokkoku Digital Banking Overdraft, however, presents a "velocity outlier" that signals a collapse of traditional barriers to entry.

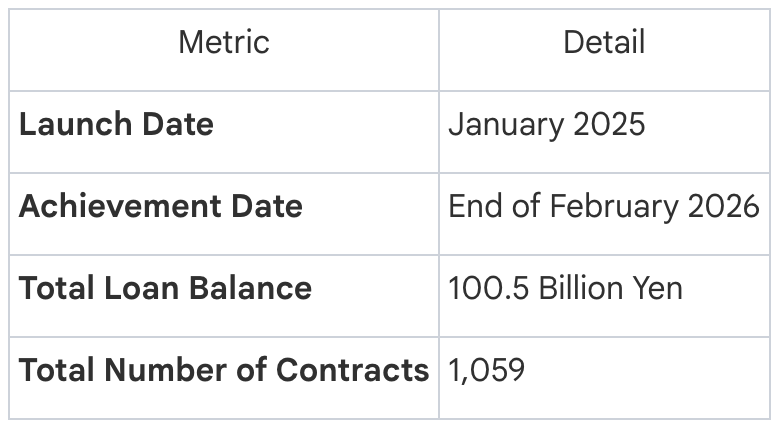

Key Performance Metrics (as of February 2026)

The attainment of a 100.5-billion-yen balance within approximately 14 months is a remarkable feat of market penetration. This rapid scale suggests that when regional banks eliminate administrative friction, they unlock latent demand for agile credit. The volume of contracts—exceeding 1,000 in just over a year—indicates that the service has successfully reached both established corporations and agile sole proprietors. This quantitative success is an inevitable byproduct of the product’s high-convience functional architecture.

2. Functional Differentiators and Operational Innovation

Traditional regional lending is often hamstrung by inherent friction: manual documentation, physical branch requirements, and the "gatekeeper" mentality of bank staff. The Hokkoku Digital Banking model dismantles these barriers through a self-service framework that prioritizes borrower autonomy.

The strategic value of this service is concentrated in three primary areas:

- Real-time Liquidity Management: By facilitating immediate borrowing and repayment between 9:00 and 17:00, the service allows firms to manage "just-in-time" capital. The key factor here is the optimization of interest expenses; firms can apply surplus funds to repayments instantly, minimizing their interest burden and maximizing internal capital efficiency.

- Autonomy via Credit Limit Visibility (Disintermediation): Clients can monitor their credit limits and execute transactions without bank staff intervention. This shifts the bank’s role from a restrictive gatekeeper to an empowerer of corporate management, allowing business owners to make decisive moves without the delay of a manual approval cycle.

- Operational Streamlining (Visit-less/Paperless): The elimination of physical visits, paper documents, and the hanko (seal) is a critical response to the acute labor shortages and geographic decentralization in regional Japan. This "visit-less" banking is a necessity for modernizing Japanese business culture, allowing lean administrative teams to focus on core growth rather than the logistics of financial paperwork.

These efficiencies represent a catalyst for regional economic revitalization, fostering a more productive environment where capital moves at the speed of digital business.

3. Technical Specifications and Service Architecture

Transparency and technical accessibility are the bedrock of trust in any digital-native ecosystem. By providing precise terms and constant data access, CCI Group’s banking arm ensures that the overdraft remains a reliable component of a firm's financial oversight.

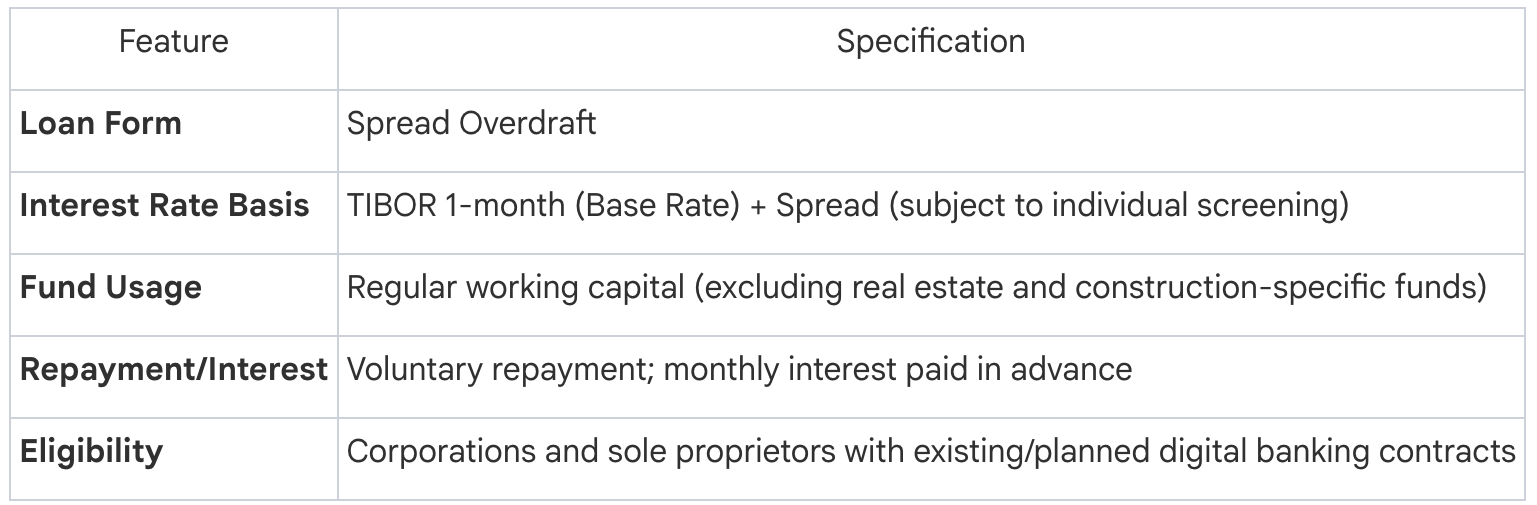

Product Specifications

Furthermore, the architecture provides 0:00–24:00 inquiry availability for transaction histories and interest calculations. This 24-hour transparency is vital for modern business owners who operate outside of standard bank hours. Such precision in data access bridges the gap between traditional credit and contemporary digital oversight, setting a high standard for the broader regional finance landscape.

4. Conclusion: Defining the Future of Regional Digital Finance

The performance of the Hokkoku Digital Banking Overdraft service provides a definitive blueprint for the "Chiho Ginko" (regional bank) of the future. By reaching the 100-billion-yen milestone with such velocity, the service has proven that the appetite for digital-native credit is robust even in the most traditional markets.

The CCI Group’s commitment to "continuing to evolve" this service implies that the platform is not a static tool, but a dynamic financial ecosystem. This strategy is essential for long-term customer retention, ensuring the bank remains the primary partner in an increasingly competitive fintech environment.

Ultimately, this success validates the CCI Group’s vision of a tech-first financial identity. By meeting diverse regional needs through high-convenience, autonomous solutions, they have established a new standard for how financial institutions can contribute to a modernized, efficient, and autonomous regional economy.