The Convergence of Code and Capital: How AI and Stablecoins are Rewiring Global Finance

The global financial landscape is undergoing a rigorous restructuring as stablecoins evolve from speculative "safe havens" for crypto-traders into the standardized settlement layer for the real-world economy. As we have progressed through the 2024–2025 cycle, these assets are being integrated into core economic infrastructure, shifting the focus from retail volatility to institutional capital efficiency and cross-border settlement.

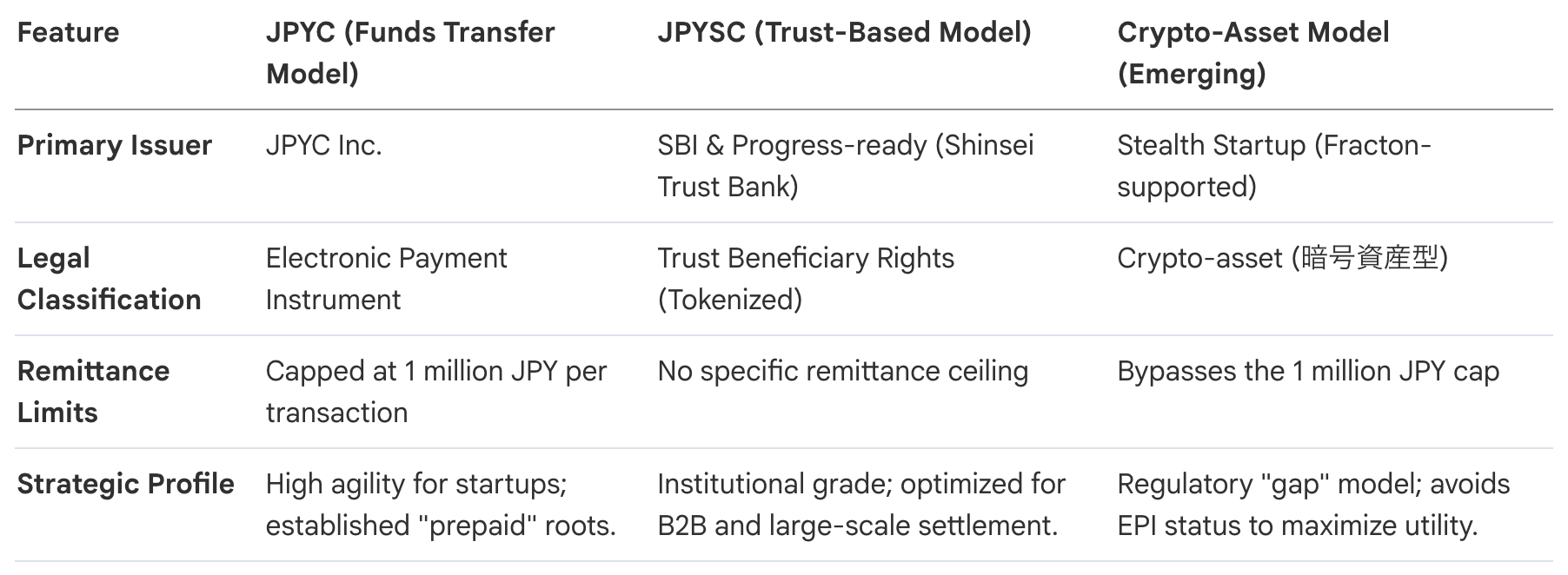

In Japan, this transition is evidenced by a maturing regulatory environment that has bifurcated into three distinct issuance models. Notably, JPYC commenced issuance under the current "Electronic Payment Instrument" framework in Autumn 2023, marking a shift toward regulated, programmable yen.

Comparison of Japanese Stablecoin Frameworks

While Japan formalizes its internal rails, the global market remains dominated by USDT on the Tron network, which currently captures over 50% of all USDT transaction volume.

There is a widening divergence between institutional technology preferences (typically Ethereum and its Layer-2s) and the retail/remittance reality. In regions such as the Middle East and Asia, Tron’s ultra-low-fee environment has rendered it the de facto global standard for value transfer, despite its lack of widespread support on major Japanese exchanges. For institutional capital to bridge this gap, legal certainty is no longer a luxury but a prerequisite.

This post serves as an event report for a webinar hosted by Fracton Ventures and SurfAI on Tuesday, March 17, 2026.

1. The Regulatory Frontier: Institutionalizing the Wild West

In the 2024–2025 cycle, regulatory clarity has transitioned from a hurdle to a primary catalyst for capital inflows. High-level executives and policy-makers now view stringent oversight as the necessary "seal of approval" for moving significant balance-sheet assets on-chain.

Two pivotal legislative frameworks identified as the "ground truth" for the U.S. market are defining this era:

- The Genius Act: This mandate requires 1:1 reserve backing and enforces bank-level security requirements. By "deputizing" issuers as quasi-banking institutions, this act mitigates counterparty risk and ensures that digital dollar equivalents maintain the same safety profile as traditional commercial bank deposits.

- The Clarity Act: This framework aims to resolve jurisdictional disputes by categorizing tokens as either securities (SEC) or commodities (CFTC). A critical point of current debate in the U.S. Senate is whether stablecoin issuers should be permitted to pass yields to holders—a decision that will dictate the competitive landscape between yield-bearing synthetic assets and non-yielding "pure" payment tokens.

Summary of Institutional Safeguards:

- Elimination of De-pegging Risk: Mandatory 1:1 liquid reserve transparency.

- Insolvency Mitigation: Statutory requirements for issuer bankruptcy remoteness.

- Operational Predictability: Clear licensing paths allowing asset managers to deploy long-term strategies without fear of retroactive enforcement.

2. The Institutional Bridge: RWA Tokenization and Global Payment Rails

The "on-chaining" of traditional finance (TradFi) represents a strategic move toward 24/7 liquidity and the elimination of T+2 settlement cycles. This is best exemplified by BlackRock’s BUIDL fund, which has successfully integrated sovereign debt into DeFi ecosystems.

A sophisticated iteration of this trend is the Kraken-Nasdaq partnership, utilizing the XT service. This model tokenizes the monetary value of equities (e.g., Meta, Netflix) as synthetic assets. By tokenizing the value rather than the underlying equity, the service circumvents the complexities of voting rights and dividends, focusing instead on price exposure and collateral efficiency.

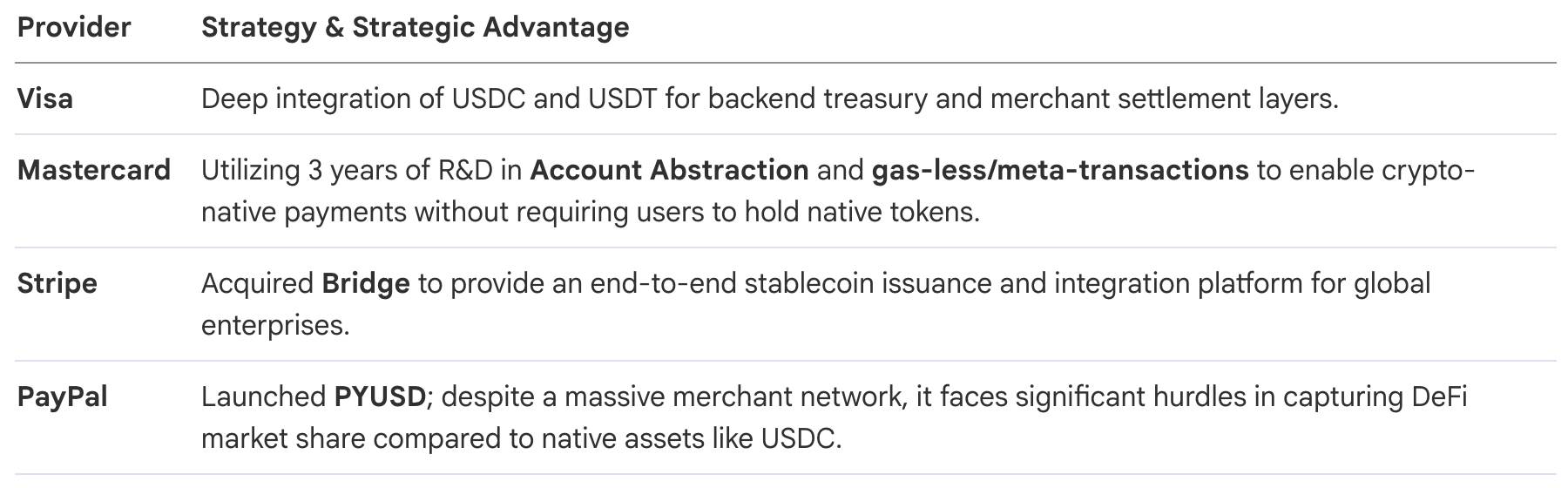

The "Big Four" payment providers have shifted from R&D to active market-share acquisition:

3. Web 4.0 and the Rise of the AI Agent Economy

The emergence of "Web 4.0" signifies an internet where autonomous AI agents act as the primary economic actors. Traditional banking—reliant on KYC (Know Your Customer), physical cards, and human-verified signatures—is fundamentally incompatible with software that operates at machine speed.

The primary friction point is cost. A standard credit card transaction involves a fee of roughly $0.30 + 3%. For an AI agent conducting a micro-payment of 0.001 USDC, the transaction fee would represent 30,000% of the value transferred, making traditional rails mathematically impossible.

To solve this, Coinbase has revived the X402 (Payment Required) protocol, an evolution of the dormant HTTP 402 error code. This allows AI agents to conduct instant, sub-cent micro-payments autonomously.

The rise of agentic funds like AI16Z and platforms like Virtuals—which manage assets based on community sentiment and autonomous logic—necessitates a shift from KYC to KYA (Know Your Agent). Institutional players must now develop frameworks to verify the provenance and permissions of code-based actors rather than human individuals.

4. Infrastructure for a Decoupled Reality: GPU Markets and Identity

The "back-end" of the AI-Crypto intersection relies on decentralized physical infrastructure (DePIN) and robust human-verification protocols to maintain a balance between automation and accountability.

- Decentralized Compute: Gensyn and Aethir are creating marketplaces for idle GPU power. This provides a disintermediated alternative to centralized cloud providers, reducing AI training costs while offering hardware providers programmatic incentives.

- Humanity Verification: As AI agents proliferate, the ability to distinguish humans from bots becomes a security imperative. World ID (Worldcoin) uses iris-scanning to establish a "proof of personhood." Conversely, the Sentient project—backed by Peter Thiel’s Founders Fund—aims to build the "Linux of AI," an open-source AGI framework that uses crypto-economic incentives to prevent the monopolization of artificial intelligence.

- The Analytical Layer: Modern data platforms like SurfAI are essential for this high-velocity ecosystem. SurfAI enables the creation of real-time dashboards that track on-chain AI activity, GPU utilization, and agentic fund performance, transforming raw data into actionable strategic intelligence.

Outlook for 2026: The Year of Implementation

2026 marks the transition from theoretical R&D to a dominant financial reality. With stablecoins providing the medium of exchange, RWAs providing the collateral, and AI agents providing autonomous labor, the global financial system is being rewired. For executives and policy-makers, the strategic imperative is no longer merely to "understand" these technologies, but to integrate them into the core of institutional operations as the new architecture of global capital.