The Digital Yen Blueprint: Navigating Japan’s Multi-Stage Transition to a CBDC Ecosystem

The Ministry of Finance hosted the 11th "Expert Meeting on CBDC" on June 25, 2026, providing a moment of reflection on Japan's institutional readiness for a Central Bank Digital Currency (CBDC).

Between October 2020 and June 2026, the Bank of Japan (BoJ) and the Ministry of Finance (MoF) have methodically constructed a framework that moves toward a definitive "System Architecture." This trajectory has evolved into a race for digital sovereignty.

As global stablecoins and foreign CBDCs threaten to infringe upon domestic monetary boundaries, Japan’s June 2026 Progress Report—a cornerstone of the "Basic Policy on Economic and Fiscal Management and Reform"—signals a transition from "if" to "how" the nation will defend the yen’s status through strategic self-reliance.

The path to this milestone is defined by a rigorous chronological evolution:

- October 2020: The BoJ issues its "Approach to CBDC," establishing the foundational policy and the "Two-Tiered" vision.

- April 2021: Launch of Proof of Concept (PoC) and pilot experiments to test technical viability and basic ledger functions.

- June 2021: The Japanese Cabinet’s "Basic Policy 2021" formalizes the government’s mandate to organize institutional design.

- April 2023: The MoF establishes the CBDC Expert Committee to analyze social impacts and civil law implications.

- January 2024: Formation of the "Liaison Committee" between ministries and the BoJ, producing its first "Interim Report" in April 2024.

- May 2025: Publication of the "Second Interim Report," refining privacy protections and legal frameworks for digital assets.

- June 2026: The current "Progress Report" is released, defining the division of labor between the public and private sectors and setting the roadmap for deployment.

Deliberations remain officially "non-prejudicial," meaning the report does not guarantee issuance. However, the depth of the 2026 framework ensures that Japan possesses a fiscal bulwark ready for immediate activation. The primary focus now shifts to the precarious balancing act of integrating this digital asset without triggering structural disintermediation in the private banking sector.

1. The Stability Mandate: Managing the Migration from Deposits to CBDC

The central threat to Japan’s macro-prudential stability is the prospect of "digital bank runs." Because a digital yen would represent a direct claim on the central bank, it is fundamentally safer than commercial bank deposits. Without safeguards, a mass migration of capital could drain commercial bank liquidity, crippling their ability to provide credit to the economy. To prevent this, the BoJ is prioritizing the "coexistence" of CBDC and private deposits through a multi-layered limit system.

The BoJ’s strategy distinguishes between macro-prudential logic—system-wide limits to prevent structural declines in deposit volumes—and micro-prudential logic, which allows individual institutions to set transfer frequency or volume caps during periods of idiosyncratic stress.

A critical, high-stakes nuance in the current deliberations is the "Zero-Limit" proposal for corporate holdings. Drawing on Eurozone comparisons, the BoJ is considering setting corporate CBDC holding limits to zero, effectively mandating that 100% of incoming corporate CBDC payments be instantly converted to bank deposits. This ensures that the digital yen remains a medium of exchange rather than a vehicle for corporate cash hoarding that could destabilize the commercial lending market.

To maintain user utility despite these restrictions, the "Auto-swing" function is proposed, a system-level function that automatically transfers CBDC balance overflows to a pre-registered commercial bank account. This ensures that if a transaction pushes a user above their holding limit, the excess is instantly converted into private money (deposits), preventing transaction rejection while maintaining the "cap" on central bank liabilities.

However, the BoJ admits to a significant technical difficulty: managing limits across multiple intermediaries. If a user holds accounts with different banks, the system must navigate the complexity of real-time aggregation to prevent limit evasion—a hurdle that may lead the BoJ to initially restrict users to one CBDC account per person.

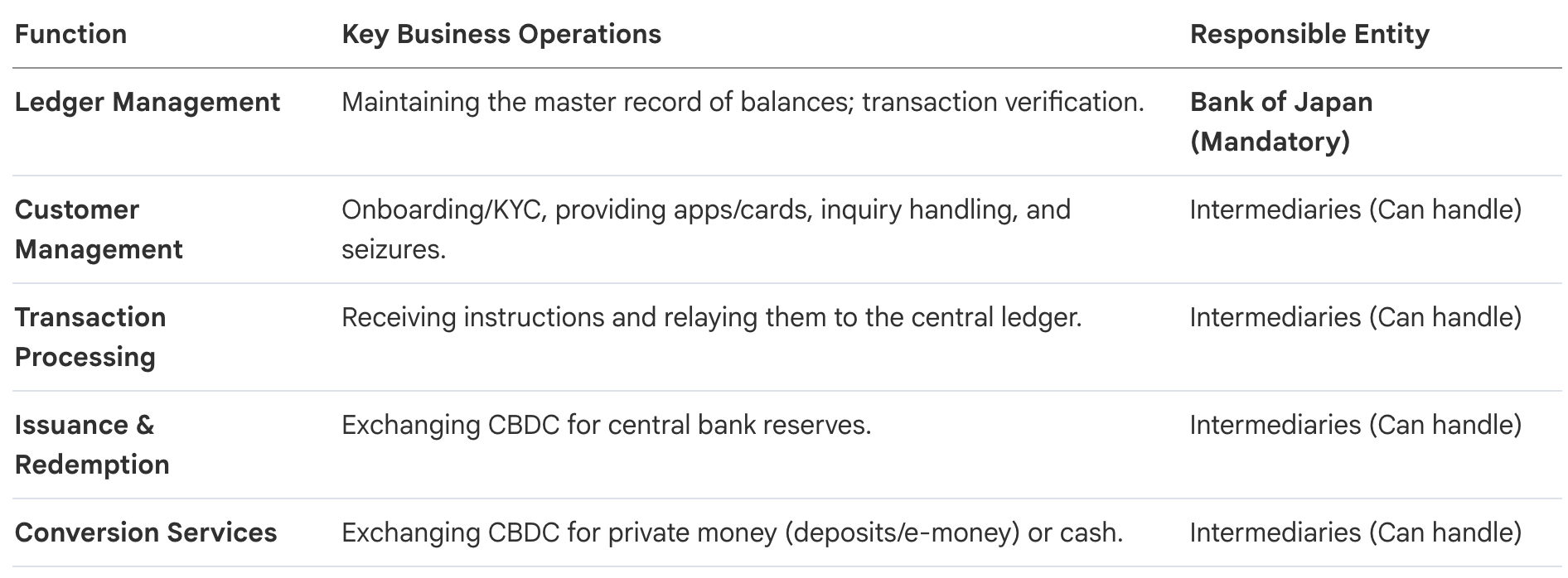

2. The Two-Tiered Architecture: Defining Roles for the BoJ and Intermediaries

Japan’s architecture leverages the "Two-Tiered Structure" to combine central bank credibility with private-sector agility. In this model, the BoJ provides the "Anchor of Trust" through the core ledger, while intermediaries handle the "last mile" of customer interaction.

The BoJ will act as a "Catalyst" for innovation, providing standardized specifications and Software Development Kits (SDKs) to lower the barrier for private entry. This prevents the core system from becoming a bloated monopoly, instead allowing banks and fintechs to build proprietary services on top of a public utility.

3. Incentivizing Participation: Burden Reduction and Value Expansion

For the private sector, the digital yen must be economically sustainable. The 2026 report outlines strategies to reduce the operational "burden" of compliance while expanding the "benefit" of participation.

Burden Reduction Strategies:

- KYC Reliance: Intermediaries may rely on existing identity verification data from a user’s current bank account to simplify onboarding.

- Common Application Platforms: Developing shared databases for AML/CFT alert data to prevent duplicative system costs.

- Maintenance Flexibility: To prevent system load failures, the BoJ proposes allowing "temporary limit breaches" during bank maintenance windows. This ensures that CBDC payments can still be received even when a bank's "auto-swing" connection is temporarily offline.

Benefit Expansion:

- Cost Compression: For banks, the digital yen offers a significant reduction in "cash handling costs," potentially allowing for the rationalization of expensive ATM networks.

- Corporate Synergy: By integrating with accounting and bookkeeping software, the CBDC could automate reconciliation processes, making it an attractive offering for corporate "main bank" relationships.

4. The Functional Roadmap: From Basic Payments to "Additional Services"

The BoJ is adopting a Minimum Viable Product (MVP) strategy for "Day 1" issuance, focusing on core transfers. However, to compete with Japan’s highly advanced private payment ecosystem, the digital yen must evolve into a programmable platform.

The report distinguishes between "Conditional Payments" (smart contracts) and "Programmable Money." The BoJ explicitly prefers the "External Program Mode"—where payment logic sits outside the core ledger. This ensures the central system remains simple and resilient, while intermediaries use APIs to trigger payments based on external events.

Roadmap for Value-Added Services

- Conditional Payments:

- Escrow: Securing C2C trades (e.g., used goods) until delivery is confirmed.

- M2M (Machine-to-Machine): Automated settlements, such as a car paying a parking meter or a machine paying for utility consumption.

- Usage-Based Billing: Real-time payments for gas or electricity based on sensor data.

- Information Utilization: Electronic receipts and automated tax/interest calculations integrated into accounting software.

- Diverse User Experiences: Real-time G2P (Government-to-Person) disbursements for subsidies and support funds.

5. Strategic Pillars: Universal Access, Resilience, and Digital Society

In a cash-saturated society, the digital yen’s existence is justified by four strategic pillars:

- Universal Access: A digital equivalent to cash that serves as a public safety net, ensuring payment access even if private networks consolidate or fail.

- Digital Society Infrastructure: Driving Digital Transformation (DX) by providing a common, low-cost payment rail.

- Autonomy and Resilience: Maintaining strategic self-reliance against foreign digital currencies and ensuring the "yen" remains the unit of account in a digitized world.

- Monetary Uniformity: Serving as the "Anchor of Trust" to ensure 1:1 exchangeability between different private digital moneys.

The rollout will be phased. The initial focus is smartphone-based QR codes (both Merchant-Presented and Consumer-Presented). However, a significant "Foreigner Gap" remains: while residents will use residency cards for KYC, providing CBDC access to non-residents (tourists) is deemed a long-term challenge requiring specialized card-based devices to mitigate double-spending risks in an offline-capable environment.

6. The Legal and Technical Frontier: Implementation Hurdles

Transforming a digital entry into "Legal Tender" requires a massive overhaul of Japan’s legal architecture. The digital yen must possess "dynamic safety," meaning a good-faith receiver is legally protected even if the sender’s authority was flawed.

- Private Law: Defining ownership and transfer rights for a digital asset.

- Civil Execution: Establishing how legal authorities can "seize" or "attach" a balance held on a central bank ledger via an intermediary.

- Criminal Law: Creating new statutes for "digital counterfeiting" to penalize the unauthorized creation of CBDC entries.

A major regulatory requirement is "Account Portability." To prevent "intermediary lock-in" and ensure a competitive landscape, the BoJ insists that users must be able to switch their service provider without changing their digital ID or losing their history.

The development process follows three distinct phases:

- Institutional Design: Finalizing policy and stakeholder roles.

- Requirement Definition: Translating policy into technical specs for performance and security.

- System Construction: Building the platform and conducting "Live Tests" with real value in controlled regions.

7. Conclusion: The Path Forward for the Japanese Financial System

The 2026 Progress Report is the definitive blueprint for a digital yen, but it highlights that the most difficult decisions—the "water-level" of holding limits and the final cost-sharing model—lie ahead.

Ultimately, the digital yen is designed to perform a vital "Anchor Function." In a future where the digital economy is increasingly fragmented by various private tokens and stablecoins, central bank money must provide the ultimate liquidity backstop. By grounding the evolving digital financial architecture in a stable, public-backed currency, the BoJ ensures that the integrity of the Japanese yen remains unassailable in the digital age.