The Formation of Chiba Financial Group

In September 2025, The Chiba Bank and The Chiba Kogyo Bank have jointly declared their resolution to pursue a management consolidation. Formalized at the time through the signing of a Memorandum of Understanding (MOU), the move aims to establish a new bank holding company that will serve as the wholly-owning parent of both institutions. To that extent, the Consolidation Agreement has been executed this past week.

The consolidation, planned to be effective on or around April 1, 2027, is a forward-looking response to the evolving economic landscape, increasing complexity of customer needs, and the intensifying competition within the financial services industry.

To sustain regional franchise value and optimize the cost-to-income ratio in this high-stakes environment, the formation of a joint holding company is the only viable path to securing long-term capital efficiency and economic stability.

The "Management Consolidation" narrative leverages Chiba Prefecture’s inherent economic vitality to address systemic demographic and technological headwinds:

- Regional Dominance: Chiba Prefecture boasts premier national rankings in GDP, commerce, industry, agriculture, and fisheries. Its status as an international business hub is anchored by Narita Airport and a sophisticated transportation infrastructure including the Ken-O Expressway.

- Structural Challenges: Despite its wealth, the region faces acute labor shortages, inflationary pressures on raw materials, and a shift in customer behavior toward digital-first interactions.

The cornerstone of this integration is the "Two Brands" vision. By retaining the operational autonomy and distinct identities of Chiba Bank and Chiba Kogyo Bank, the group maximizes regional financial capabilities while minimizing customer churn and preserving the localized trust inherent in each brand. This dual-brand strategy ensures the maintenance of a sound regional financial system while providing a diversified suite of sophisticated financial solutions. This structural alignment is meticulously governed to ensure that strategic efficiency does not come at the expense of regional intimacy.

1. Corporate Governance and Leadership Architecture

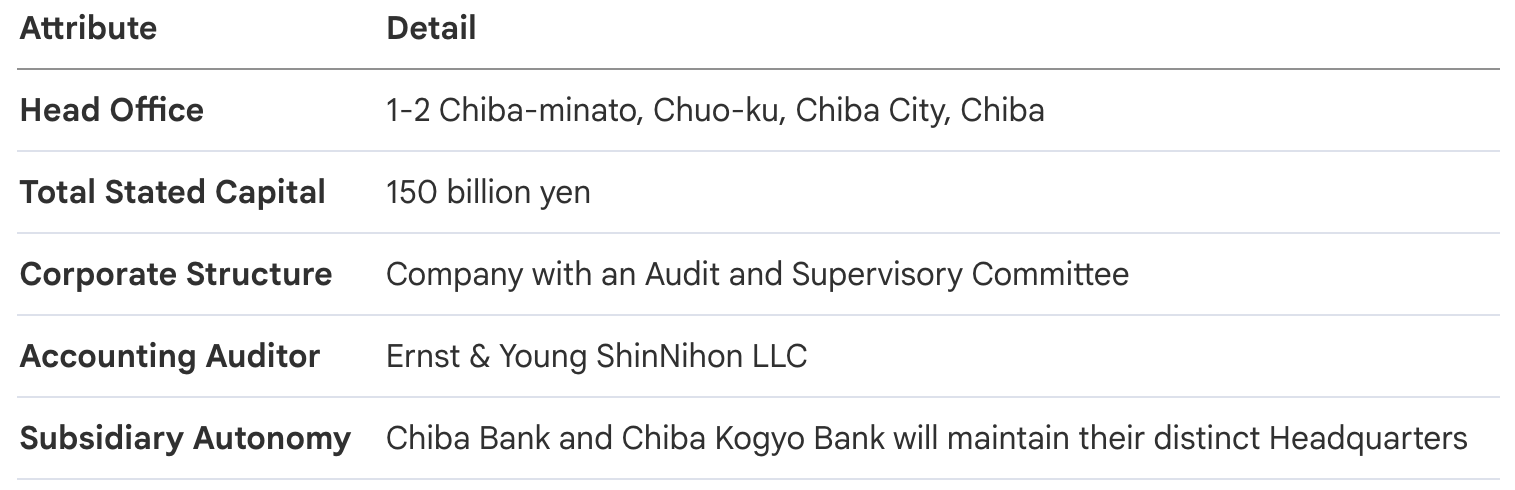

Ensuring "mutual trust and respect" during a joint share transfer requires a governance framework that balances independent oversight with tactical integration expertise. The Joint Holding Company is structured as a "Company with an Audit and Supervisory Committee" to provide rigorous fiduciary oversight.

The leadership architecture is designed for executive continuity and balanced representation. Tsutomu Yonemoto (President and Group CEO of Chiba Bank) will assume the role of President and Representative Director, while Hitoshi Umeda (President of Chiba Kogyo Bank) will serve as Vice President and Representative Director.

The Board will consist of 10 Directors, 5 of whom are Outside Directors, ensuring majority independent oversight on key strategic decisions. The board is supported by specialized committees including Sustainability, Digital, ALM, Risk Management, Compliance, and the Nomination, Remuneration and Corporate Advisory Committee. Crucially, the Consolidation Promotion Committee and the General Secretariat will serve as the technical engine rooms for the integration, managing the complex operational convergence between the two brands.

2. The Management Consolidation & Share Transfer Roadmap

The "Joint Share Transfer" serves as the foundational mechanism, establishing Chiba Financial Group as the 100% parent of both banks. This alignment of capital is the prerequisite for realizing group-wide economies of scale.

Chronological Integration Timeline

- September 29, 2025: Execution of the Memorandum of Understanding (MOU).

- March 25, 2026: Execution of the Management Consolidation Agreement.

- September 30, 2026: Preparation of the formal Share Transfer Plan and Record Date for Extraordinary General Meetings.

- December 23, 2026: Extraordinary General Meetings of Shareholders to approve the Share Transfer Plan.

- March 30, 2027: Delisting of both banks from the Tokyo Stock Exchange.

- April 1, 2027 (Effective Date): Registration of Chiba Financial Group, Inc. and listing on the TSE Prime Market.

Details of Financial Allotment

The allotment of shares ensures equitable value distribution for all classes of investors:

- Common Stock: A 1:1 ratio is established. An expected total of 867,743,132 shares of common stock will be issued by the new holding company.

- Preferred Stock (Class 6 and 7): To ensure fairness for unlisted shares, the Variable Share Transfer Ratio Method was adopted. This method targets a value of 20,000 yen for Class 6 and 500,000 yen for Class 7 shares. The ratio will be determined using a simple average of the closing price of Chiba Bank common stock during the calculation window of March 5, 2027, to March 18, 2027. The ratio will be calculated to the third decimal place and rounded to the second, minimizing the risk of price volatility during the transition.

3. Operational Synergies and Functional Integration

A primary strategic objective is leveraging economies of scale to optimize the group’s cost-to-income ratio. This streamlining allows for the reallocation of capital toward high-growth fields like DX and AI.

Evaluation of Integration Pillars

- Headquarter Optimization: By reducing administrative overlap and centralizing management functions at the holding company level, the group will eliminate redundant cost layers and improve decision-making speed.

- Back-Office Consolidation: The centralization of second- and third-line operations (clerical, system operations, and credit processing) will directly mitigate operational risk while freeing up significant human capital for high-value client-facing roles.

- Core Systems Integration: Building a unified system architecture is a high-priority efficiency play. This integration will drastically reduce the long-term IT maintenance burden and create a standardized platform for rapid AI deployment.

Integration Readiness and Resilience

Both banks bring extensive alliance experience to this merger, which significantly de-risks the integration process. Chiba Bank’s leadership in the TSUBASA Alliance, Chiba-Musashino Alliance, and Chiba-Yokohama Partnership, combined with Chiba Kogyo Bank’s involvement in the FinX Partnership and the Regional Bank Integrated Service Center, provides a proven blueprint for collaboration. This collective expertise will be utilized to strengthen resilience against financial crimes through unified AML protocols and enhanced cybersecurity measures.

4. Value Creation: Customer Experience and Regional Revitalization

The group will "step up" to solve regional challenges by combining the sophisticated capabilities of a major holding company with the localized intimacy of two trusted brands.

Customer Experience (CX) Evolution

The integration will deliver a superior CX through:

- Sales Channel Expansion: Mutually leveraging customer relationships to provide a broader solution set across the prefecture.

- Product Diversification: Scaling high-specialty products (e.g., sustainability-linked loans, wealth management) across both banks.

- Omni-channel Integration: Harmonizing in-person, remote, and digital channels to meet the evolving behavioral patterns of the modern consumer.

Sustainable Regional Development

The "Two Brands" approach is a commitment to the maintenance of a sound regional financial system. By preventing regional economic disruption and providing "Sustainable Solutions," the group supports Chiba’s evolution as an international business hub, ensuring that regional growth remains resilient despite national demographic shifts.

5. Human Capital Management and Organizational Engagement

The long-term success of the consolidation depends on fostering specialized talent capable of driving value in a digital-first economy.

Human Resources Strategy

The HR strategy focuses on cross-pollinating expertise between the two banks to create new growth opportunities:

- Fostering DX Talent: Pooling resources to train personnel in generative AI and advanced financial technologies.

- Knowledge Sharing: Utilizing the different strengths of each bank to create a more versatile and professional workforce.

- Employee Engagement: Building a culture where employees can "shine in their own way" by providing diverse career paths within the expanded group structure. This approach is vital for attracting the professional expertise required to navigate the modern financial landscape.

6. Conclusion: Stakeholder Value Cycle and Implementation Outlook

The formation of Chiba Financial Group, Inc. initiates a comprehensive "Cycle of Value Enhancement for Stakeholders." This is not merely a financial transaction but a fundamental restructuring of regional financial power to thrive in an era of positive interest rates and rapid technological change.

With the Effective Date of April 1, 2027, established and the Extraordinary General Meetings scheduled for December 2026, the group is moving forward with significant momentum. The ultimate objective is clear: creating a consolidated, resilient, and technologically advanced regional powerhouse that is perfectly positioned to bring each person’s hope to life while ensuring the sustainable prosperity of Chiba Prefecture.