The Quiet Conservatism: How Japan’s G-SIBs Navigate the Fragmented Global Capital Stack

In the wreckage of the Great Financial Crisis (GFC), the Basel III framework was marketed as the definitive regulatory equalizer—a universal code designed to ensure that Global Systemically Important Banks (G-SIBs) operated on a level playing field. The strategic vision was a harmonized global standard that would eliminate the "race to the bottom" in banking supervision. However, looking back from the vantage point of 2026, it is clear that while the rules have converged, the actual regulatory burdens remain profoundly disparate. The result is a fragmented global "capital stack" where the definition of resilience is increasingly shaped by national supervisory discretion rather than international accord.

The Basel III architecture rests on three pillars: Pillar 1 (minimum capital and universal buffers), Pillar 2 (the supervisory review process), and the non-risk-based Leverage Ratio. While Pillar 1 establishes a common floor—most notably the 4.5% Common Equity Tier 1 (CET1) ratio—national authorities have aggressively utilized the flexibility to "tailor" requirements. This jurisdictional tailoring has turned the dream of a singular standard into a heterogeneous reality. In 2026, the regulatory burden a bank carries is a product of its home supervisor’s philosophy, creating a complex bridge between these global standards and the structurally leaner, yet deceptively conservative, reality of the Japanese banking sector.

1. Positioning Japan in the Global Capital Hierarchy

For the institutional investor or policy-maker, raw capital ratios are a dangerous metric to view in isolation. Comparing Japanese G-SIBs against their peers in the European Banking Union (BU), the United States, and China requires a forensic look at jurisdictional nuance. A bank that appears "lean" in Tokyo may carry the same functional resilience as a "heavy" bank in New York once the underlying risk-weighting methodologies are unmasked.

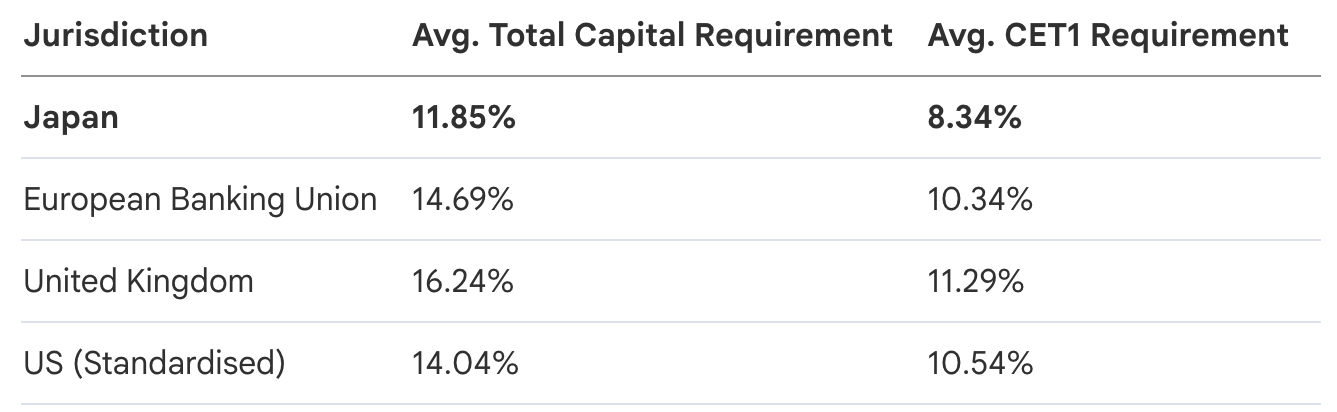

In terms of explicit ratio requirements, Japan currently sits at the lower end of the global spectrum. As of the 2025/2026 reporting cycle, Japan’s "Total Capital Requirements" average 11.85%, with a CET1 requirement of 8.34%. This contrasts sharply with the European Banking Union’s 14.69% total requirement and the US Standardised Approach, which frequently demands in excess of 14%.

Does this lower ratio represent a "regulatory advantage" for Japan? Not necessarily. The data suggests a compensatory trade-off: jurisdictions with leaner ratio requirements often balance them with different supervisory expectations or risk-weighting densities. For the Japanese G-SIBs, the "advantage" of a lower ratio is largely offset by a system of supervisory benchmarking that operates with the weight of law, if not the transparency.

2. The Japanese Exception: Supervisory Benchmarking vs. Explicit Pillar 2

If Pillar 1 is the universal law, Pillar 2 is the supervisor’s scalpel—a mechanism to capture idiosyncratic risks like interest rate risk in the banking book (IRRBB) or credit concentration that Pillar 1 misses. While the EU and UK have moved toward a "Two-Tier" framework—combining binding Pillar 2 Requirements (P2R/P2A) with non-binding Pillar 2 Guidance (P2G/P2B)—Japan remains the global outlier.

Japanese G-SIBs are not subject to the explicit, public-facing Pillar 2 targets found in the West. Instead, Tokyo employs a "Benchmarking" system. Through annual stress tests and intensive "supervisory dialogue," the Bank of Japan forms "implicit expectations" of capital adequacy. This is a system of "gentleman’s agreement" backed by regulatory steel; while Japan lacks an explicit Maximum Distributable Amount (MDA) trigger for Pillar 2, the "shadow of the MDA" looms large. Bank managers understand that falling short of these benchmarks invites supervisory intervention that is functionally equivalent to the binding rules of their peers.

The Landscape of Discretion: Binding vs. Non-binding Elements

- Japan: No explicit Pillar 2 targets; reliance on annual benchmarking and implicit supervisory expectations.

- United States: A binding Stress Capital Buffer (SCB) floored at 2.5%, translating stress test results directly into a public mandate.

- Canada: A non-binding Domestic Stability Buffer (DSB), currently set at 3.5%, designed to be dialled up or down based on systemic risk.

- European Banking Union: A two-tier structure featuring a binding P2R (triggering MDA) and a non-binding P2G calibrated from stress tests.

3. The RWA Density Factor: Where Japan Truly Stands

A capital ratio is only as honest as its denominator. Risk-Weighted Assets (RWA) are where the true "conservatism trade-off" is revealed. If a supervisor allows a bank to model its risk aggressively, it will likely demand a higher capital ratio to compensate. Conversely, high RWA density—a more conservative measure of risk—allows for lower ratios.

The 2026 data highlights this tension perfectly. Japan’s RWA density stands at 27.86%. This is significantly lower than China (54.85%) or the US Standardised Approach (44.93%), though it remains slightly higher than the UK’s 26.21%.

Comparative RWA Density (2025/2026 Average)

- China: 54.85% (Conservative measurement, lower ratios)

- United States (SA): 44.93% (Standardized floor, high ratios)

- Japan: 27.86% (Moderate density, leaner ratio stack)

- United Kingdom: 26.21% (Internal model reliance, higher ratios)

The suggestive evidence from the 2026 cycle is that authorities like those in Japan compensate for lower risk measurement conservatism (lower RWA density) with their intensive supervisory dialogue. The degree to which a jurisdiction allows internal models to influence these densities is the silent driver of the entire capital stack. In Japan, the moderate density suggests that while the "leanness" of the ratio is real, the underlying assets are held to a measurement standard that keeps the total capital burden competitive with more "aggressive" ratio-heavy regimes.

4. The Leverage Ratio Backstop: A Secondary Comparison

To prevent internal risk models from drifting into fantasy, Basel III’s non-risk-based Leverage Ratio serves as the ultimate backstop. It is the "Too-Big-To-Fail" insurance policy. While Japan adheres closely to the common Basel III baseline, other jurisdictions have armored their leverage ratios with additional systemic buffers.

The US, for instance, has maintained its "enhanced supplementary leverage ratio," while Switzerland has implemented a specific 0.8% AT1 systemic risk buffer and a 1.5% CET1 systemic risk buffer to address the sheer scale of its G-SIBs relative to its GDP. For Japanese institutions, the leverage ratio remains a critical secondary constraint, ensuring that the "quiet conservatism" of their risk-based modeling does not evolve into excessive nominal leverage.

5. Conclusion: Navigating the "Uneven Playing Field"

The debate over the "uneven playing field" in global banking is often a debate over optics. On the surface, Japanese G-SIBs operate within a leaner framework, with explicit capital percentages that suggest a lighter touch than those found in London or New York. However, this is a regulatory mirage.

The true state of the global regulatory experiment in 2026 is a "Convergence of Outcomes" rather than a "Convergence of Rules." While the requirements stack looks different across borders, the actual capital levels held by G-SIBs have become increasingly homogeneous. Japan’s leaner stack is balanced by moderate RWA density and an informal but ironclad supervisory benchmarking process.

As we move forward, "Market Discipline" (Pillar 3) will be the only tool capable of piercing this jurisdictional fog. The Basel Committee’s ongoing efforts to increase transparency will eventually expose that Japan’s "Quiet Conservatism" is not a sign of weakness, but a localized method of achieving the same systemic resilience as its more vocal peers. Global convergence is no longer about identical rulebooks; it is about ensuring that, regardless of the methodology, the world’s largest banks are prepared for the next crisis.