The Revised Financial Instruments and Exchange Act Submitted to the Diet

The Cabinet Office on Friday submitted proposed legislative reforms to Japan’s Financial Instruments and Exchange Act and the Payment Services Act, aimed at modernizing capital markets and enhancing investor protection, to the Diet.

The headline-grabbing focus is reclassifying crypto-assets as financial products under stricter securities regulations to curb unfair trading and improve service provider transparency. The amendments also introduce mandatory sustainability disclosures and third-party assurance for major listed companies, aligning Japanese reporting with international standards.

To foster innovation, the legal framework simplifies fundraising for startups by raising disclosure exemption thresholds and expanding the scope of professional investors. Additionally, the proposal strengthens enforcement mechanisms by increasing penalties for unregistered operators and digitizing investigative procedures to combat market manipulation.

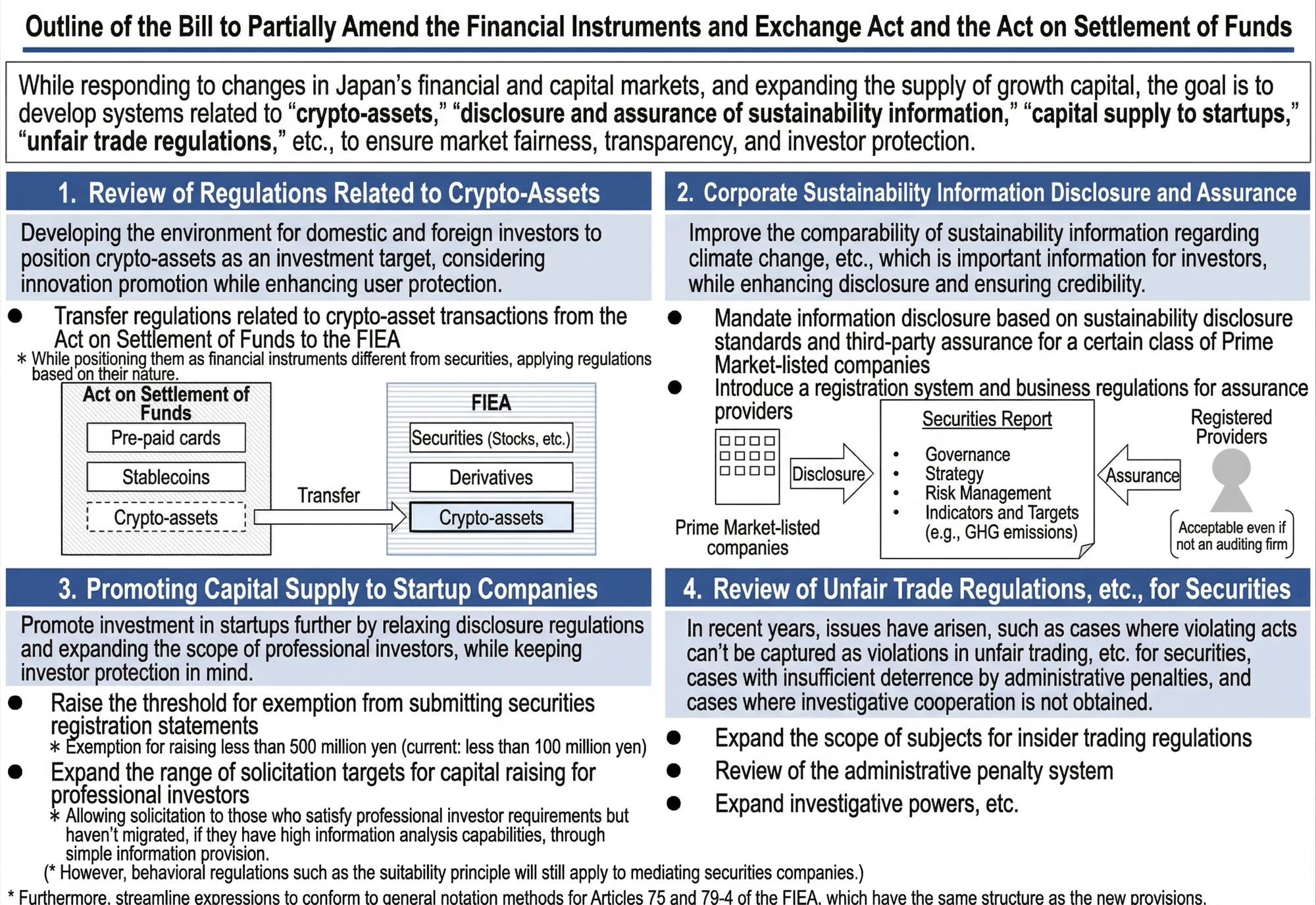

1. The Migration of Crypto-assets to the FIEA Framework

A primary objective of the revision is the re-alignment of crypto-asset regulation from the PSA to the FIEA. This reclassification signifies the maturation of crypto-assets from "means of payment" to "investment targets." From a compliance perspective, this shift subjects the sector to the Financial Services Agency (FSA) and the Securities and Exchange Surveillance Commission (SESC) under much more aggressive supervisory intensity, moving away from the lighter-touch regime of the PSA.

Definitions and Disclosure Requirements

The revised Act distinguishes between "Specified Crypto-assets" (e.g., IEO tokens where a specific issuer exists) and other crypto-assets (e.g., Bitcoin). Under Art. 27-39 and 27-60, disclosure mandates are now strictly tiered based on the nature of the asset.

Insider Trading and Market Integrity

To ensure market integrity, insider trading prohibitions (Art. 171-7 to 171-10) now explicitly apply to crypto-assets. Three categories of "Material Facts" trigger these prohibitions:

- Issuer-related Facts: Decisions such as the dissolution or insolvency of the issuing entity.

- Provider-related Facts: Non-public information regarding the commencement or termination of a specific asset’s handling by a service provider.

- Large-scale Trading-related Facts: Knowledge of intent to conduct massive trades, specifically defined as involving 20% or more of the circulating supply.

Operational Standards for Business Operators

Crypto-asset Business Operators (formerly Exchange Providers) must now meet heightened operational criteria:

- Security & Cold Wallets: Assets must be managed primarily via "Cold Wallets" (offline management of private keys).

- System Provider Oversight: Providers of critical management systems are now subject to registration and safety-of-system obligations.

- Financial Instruments Liability Reserves: Under Art. 46-5, operators must maintain specific reserves to ensure compensation for customers in the event of asset leaks or theft.

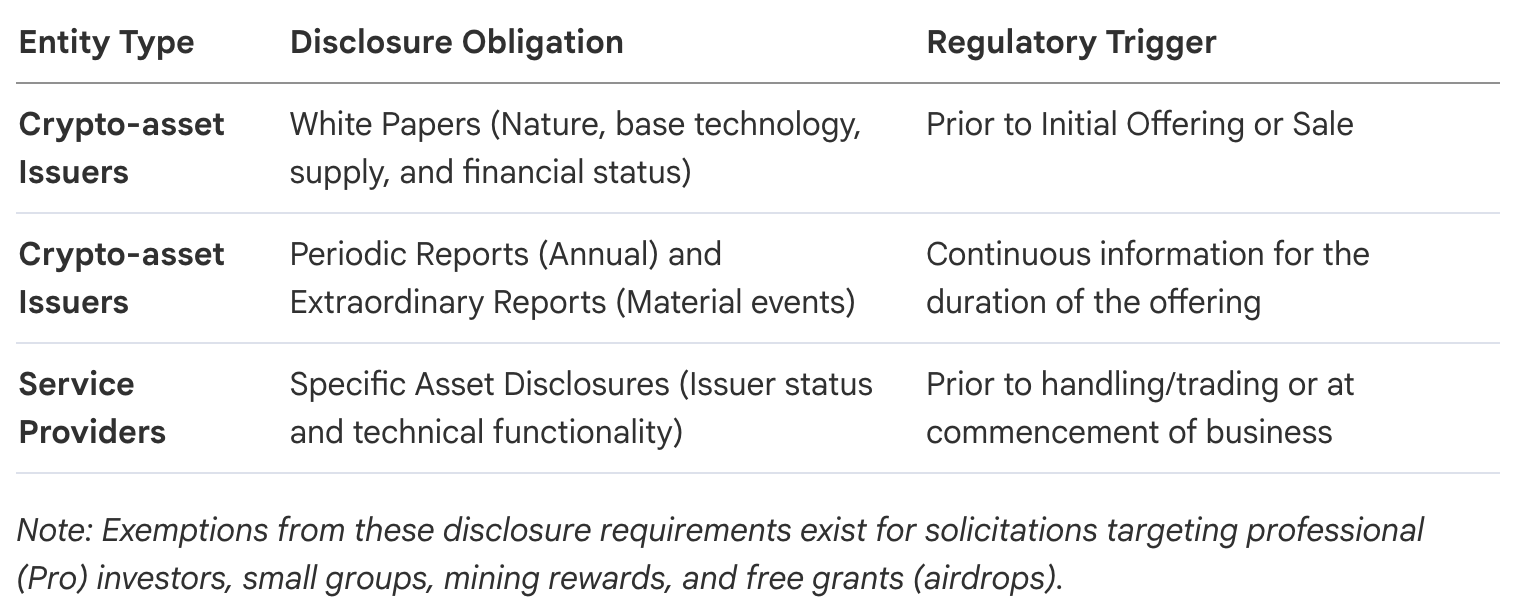

2. Sustainability Disclosure and the SSBJ Standard Mandate

Standardized sustainability reporting has moved from a voluntary best practice to a regulated mandate. The adoption of SSBJ standards ensures functional alignment with the International Sustainability Standards Board (ISSB) benchmarks, reducing reporting fragmentation.

Phased Implementation Timeline

The mandate targets Prime Market companies, with thresholds determined by a 5-year average of fiscal year-end market capitalization:

Compliance Grace Period: A "Two-Step Disclosure" (二段階開示) process is permitted for the first two years of the mandate. This allows companies to file initial reports within the Securities Report and provide supplementary corrections or data by the half-year report deadline.

Third-party Assurance and the Safe Harbor Rule

To ensure data reliability, third-party assurance becomes mandatory one year following the reporting mandate. A registration system is established for assurance providers; notably, non-audit firms may participate if they demonstrate equivalent professional expertise and quality control systems.

To encourage transparent disclosure, the "Safe Harbor" Rule protects companies from civil and administrative liability for certain non-financial data. Compliance Requirements for Protection:

- Disclose the underlying facts, assumptions, and reasoning processes for forward-looking statements.

- Document internal review procedures for estimates and data obtained from third parties not under company control (e.g., Scope 3 emissions or government data).

- Management Confirmation Letter: Management must explicitly state they have established and verified the effectiveness of disclosure procedures for non-financial information.

3. Liberalizing Capital Raising: New Thresholds for Startup Growth

To expand the supply of growth capital, the revision significantly reduces the administrative friction for non-listed companies and clarifies incentive structures for human capital.

Securities Registration and Incentive Reforms

The reform shifts the threshold for filing a full Securities Registration Statement to facilitate larger-scale fundraising without the burden of full disclosure:

- Current State: Exempt for raising < ¥100 Million.

- Revised State: Exempt for raising < ¥500 Million.

Stock Option Reform: Under the revised Art. 2, the solicitation of stock and stock options for officers and employees of a company (and its subsidiaries) is now explicitly excluded from the definition of "Public Offering/Sale," regardless of whether the company is listed. This removes a significant administrative barrier to talent acquisition.

Small-scale Offering Framework (¥500M to ¥1B)

A simplified registration format is available for mid-tier raises, featuring:

- Audited Financials: Only one year of audited financials (including comparative info) is required for first-time filers.

- Optionality: Sustainability information and consolidated data are made optional.

- Governance: Reporting is simplified to match standard business report levels.

Expansion of the "Potential QII" Category

To reduce onboarding friction, the "Potential Qualified Institutional Investor" (Potential QII) category now includes sophisticated individuals and entities who meet the technical requirements but have not completed formal transition procedures. This allows them to participate in private placements under simplified professional-oriented solicitation, while they remain treated as general investors for conduct-of-business protections (e.g., suitability duties).

4. Strengthening Market Integrity: Enforcement and Unfair Trade Provisions

Robust enforcement is the cornerstone of investor trust. The revisions address existing loopholes where unfair behaviors were previously uncaptured or insufficiently deterred.

Expansion of Insider Trading Scope

The definition of "insiders" in Tender Offers (TOB) has been critically expanded. Under Art. 167, advisors and negotiators of the target company (sell-side) are now explicitly covered. This ensures that those negotiating the deal on behalf of the company being acquired are prohibited from trading on that non-public information.

Surcharge System (Administrative Penalties)

The surcharge system has been recalibrated to provide a credible deterrent:

- Insider Trading in TOBs: Penalties now reflect the difference between the purchase price and the higher of: (1) 1.5x the pre-announcement price, or (2) the highest price in the two weeks post-announcement.

- Large Shareholding Reporting Violations: The penalty has been increased to 70x the previous rate, now set at 7/10,000 of the issuer's market capitalization.

- High-Frequency Trading (HFT): Market manipulation penalties are now calculated based on actual profits made during the violation period, with rounding precision adjusted to 1 yen (previously 10,000 yen) to capture high-volume, low-margin manipulation.

Digitalization and Criminal Sanctions

Investigation procedures are being modernized (effective October 1, 2027) to allow for electronic warrants and digital records. Additionally, criminal penalties for unregistered operators have been significantly increased to a maximum of 10 years imprisonment or a ¥10 million fine.