Tokyo Kiraboshi Surpasses Targets as Rate Hikes and Digital Pivot Drive 35% Profit Surge

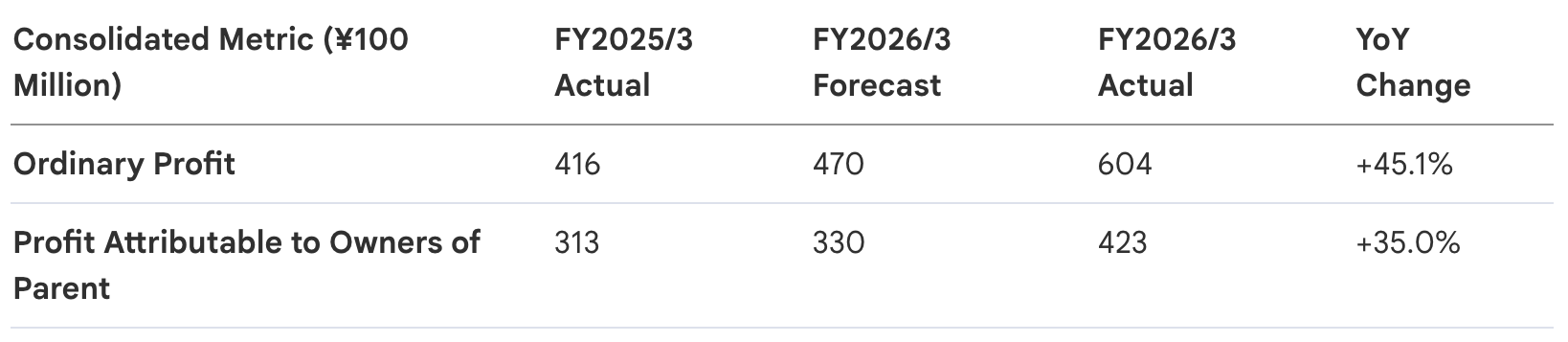

Tokyo Kiraboshi Financial Group (TKFG) delivered a definitive earnings beat for the fiscal year ended March 31, 2026, capitalizing on the Bank of Japan’s hawkish policy shift to outpace its own conservative projections. Amidst the first meaningful rise in domestic interest rates in a generation, the Group reported a consolidated net income of ¥42.3 billion—a 35% surge that significantly exceeded expectations. However, the quality of this beat includes a strategic "special factor": ¥7.4 billion of the gain was derived from the sale of shares specifically earmarked for the redemption of preferred shares, a move aimed at streamlining the Group’s capital structure.

The following table highlights the institution's success in navigating the transition away from negative interest rates:

The Group’s progress rates—128.6% for ordinary profit and 128.3% for net income—underscore an aggressive and successful capture of market tailwinds, an indicator of management’s ability to front-load tactical shifts in its lending and securities portfolios, allowing the bank to absorb volatility and emerge with a significantly bolstered bottom line. As the Group transitions into the 2027 cycle, the focus shifts from top-line consolidated figures to the specific operational engines within the core bank.

1. Core Banking Dynamics: Navigating the Interest Rate Shift

The normalization of Japanese interest rates has fundamentally recalibrated the profitability of Kiraboshi Bank’s non-consolidated operations. The bank’s "Main Bank" strategy—focused on deepening relationship-driven lending with SMEs and retail clients—has allowed it to reprice its loan book with enough speed to offset the inevitable rise in funding costs.

Key drivers of the bank's non-consolidated net income (¥39.6 billion, up 31.1% YoY) include:

- Surge in Loan and Discount Income: Interest income jumped by ¥12.6 billion. This was fueled by a double-pronged approach: increasing overall loan balances and leveraging the BoJ’s policy rate hike to lift loan yields.

- Rising Funding Pressure: The bank recorded a ¥(10.3) billion drag in "Other interest income," a metric primarily representing the rising cost of deposits and other interest-bearing liabilities in a competitive rate environment.

- Operational Discipline: Expenses rose by ¥(2.1) billion, driven by personnel costs—including base salary hikes to attract talent—and administrative outsourcing, though these were comfortably absorbed by the ¥8.5 billion growth in gross core business profit.

Critically, the Loan-Deposit yield difference expanded from 1.37% in 2025/3 to 1.41% in 2026/3. This widening margin confirms the bank’s pricing power; despite rising deposit costs, lending yields (which hit 1.70% on a non-consolidated basis) climbed faster. This traditional lending strength provides the capital runway for the Group’s higher-growth digital and non-interest income initiatives.

2. Segment Analysis: UI Bank’s Path to Profitability and Group Synergies

A major strategic milestone was achieved in the Digital Business segment as UI Bank reached profitability, signaling an end to its capital-intensive startup phase. This turnaround was the primary catalyst for the Group’s non-bank subsidiaries exceeding their aggregate profit target of ¥3.0 billion.

UI Bank Performance Highlights:

- Profit Turnaround: Achieved a net income of ¥100 million, a massive ¥1.5 billion swing from the ¥1.4 billion loss recorded the previous year.

- Loan Mix Evolution: Loan balances reached ¥268.6 billion. While mortgages provided the foundation, the late-year surge was bolstered by Investment Real Estate loans, which have seen rapid adoption since their December 2024 launch.

Group Company Profit (excluding the core bank) reached ¥3.42 billion, driven by a ¥2.29 billion turnaround in the Digital Business. While the Financial and Solutions businesses remained stable, the pivot toward an "integrated solution" model—combining consulting and digital services—is successfully reducing the Group’s structural reliance on interest margins. By providing business matching and system support, Kiraboshi is effectively locking in SME clients beyond the lending relationship.

3. Asset Management and Securities Strategy: Risk Control in Volatile Markets

As domestic yields climbed, TKFG executed a sophisticated "clearing of the decks" maneuver within its securities portfolio. Management moved aggressively to insulate the balance sheet from duration risk, reducing interest rate sensitivity through tactical disposals and hedge operations.

Tactical shifts in the securities portfolio included:

- Duration Compression: The bank dramatically slashed its duration from 3.4 years to 2.1 years (after accounting for hedges), a defensive posture intended to mitigate further rate-driven price volatility.

- The Bond "Exit": Utilizing gains from hedge operations and share sales, the bank funded "loss-cutting" sales of Yen bonds with maturities exceeding 10 years, bringing the balance of that long-term bucket to zero.

- Unwinding Cross-Holdings: The Group realized ¥9.9 billion in gains from the sale of securities, largely driven by the strategic unwinding of cross-held shares—a trend consistent with broader Japanese corporate governance reforms.

- Yield Enhancement: Securities yield rose to 2.91% (+0.50%pt YoY), assisted by a ¥2.9 billion increase in fund income following exits from portfolio funds managed by Kiraboshi Capital.

For FY2027, the bank’s Yen bond policy remains conservative, with a continued focus on short-term instruments. These maneuvers have effectively utilized periods of market strength to flush out long-term interest rate risk, ensuring capital stability.

4. Shareholder Returns and Capital Adequacy

The Group’s record profitability has allowed for a fifth consecutive year of dividend increases, backed by a robust accumulation of capital that has outpaced its risk-weighted asset growth.

Annual Dividend per Share History: The total annual dividend rose to ¥170, reflecting a progressive payout strategy:

- Second Quarter Dividend: ¥85

- Year-end Dividend: ¥85

The underlying strength of these results is even more pronounced when considering that "other non-recurring profit" faced a ¥(6.0) billion YoY headwind. This drag was primarily due to the absence of a ¥3.3 billion extraordinary gain from land sales recorded in the previous fiscal year, meaning the FY2026 surge was driven purely by operational excellence rather than one-off asset liquidations.

TKFG’s Consolidated Capital Ratio improved to 9.54% (up from 8.74%), as profit accumulation far outstripped the modest growth in Risk-Weighted Assets (RWA), which totaled ¥4,038.5 billion. With its balance sheet de-risked and its digital arm now contributing to the bottom line, Tokyo Kiraboshi remains fiscal-ready for the 2027 cycle, firmly committed to its regional mission: "Giving our all, for TOKYO."