Transitioning to Japan’s New Real-Time Payment Architecture

The global financial landscape is currently undergoing a foundational transition toward Fast Payment Systems (FPS) that operate 24/7/365 with near-instantaneous settlement. In this environment, modernizing payment infrastructure is a prerequisite for maintaining national economic competitiveness. As international trade and digital services accelerate, the ability to move liquidity across borders and between institutions with speed and data transparency has become the baseline for the modern economy. For Japan, the transition to a New Settlement System (NSS) is critical to ensuring that its domestic financial ecosystem can interface seamlessly with an increasingly integrated global market.

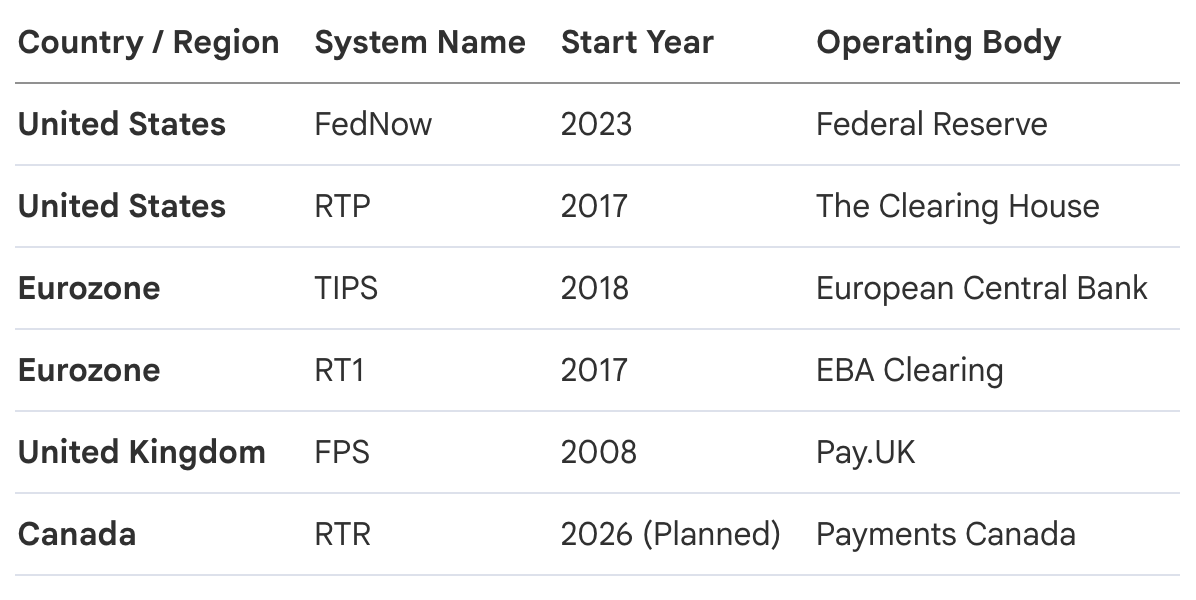

Data from the international landscape indicates that Japan’s peers have already established or are in the final stages of deploying modern FPS architectures, leaving the 1973-era Zengin system increasingly isolated.

Remaining tethered to a legacy framework risks the "Galapagos-ization" of Japan’s financial sector—a state of isolation where domestic systems are technically incompatible with international standards. Specifically, the global shift toward ISO 20022 as the universal messaging standard means that Japan’s traditional formats hinder cross-border interoperability and create friction in foreign exchange efficiency. Failure to modernize will make it technically impossible for Japan to link with emerging multilateral hubs, such as Project Nexus, which are currently connecting national FPS networks across the ASEAN and EU regions for instant cross-border transfers.

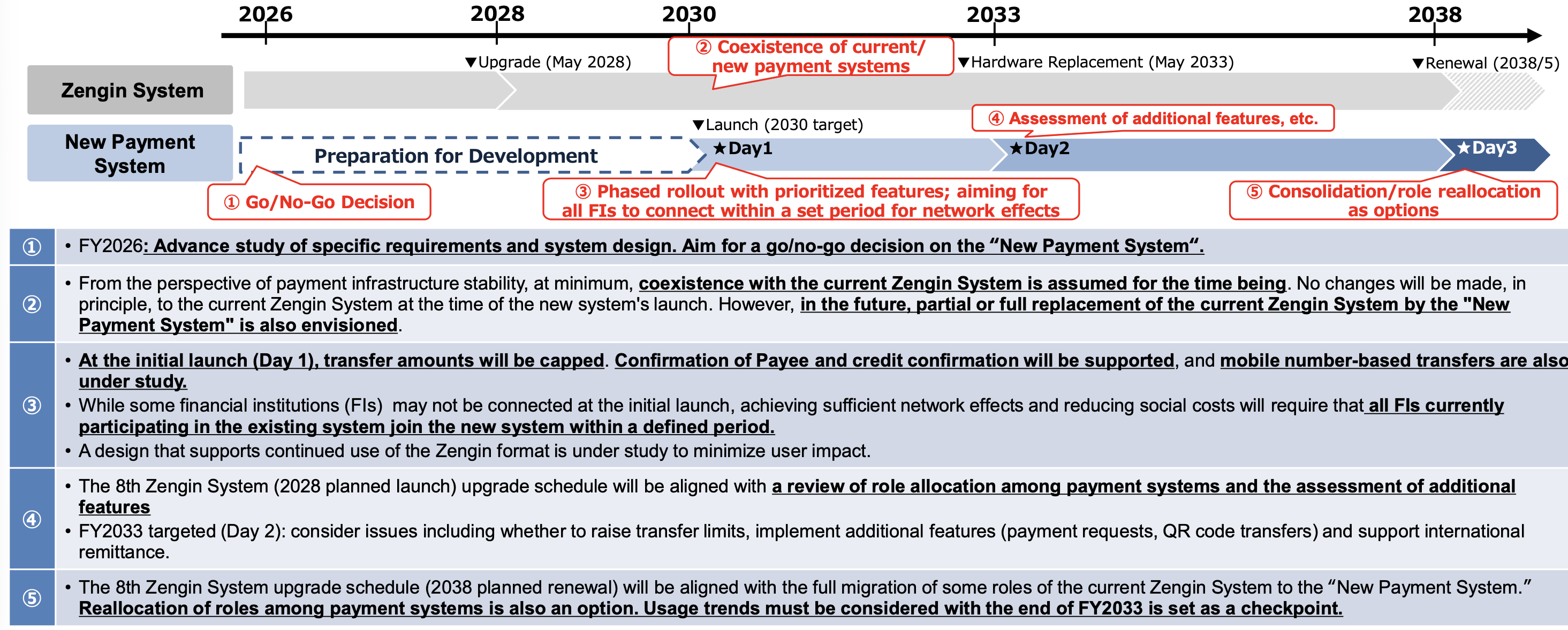

Since its second generation, the Zengin System has been updated every eight years. This implied the eighth generation was scheduled for November 2027, and the ninth generation for 2035. However, towards the end of 2024 the eighth generation had been postponed until 2028, and the discussions since have now led to the concept of a "New Settlement System (NSS)" to be implemented by 2030.

1. Critique of the Legacy Zengin System: Structural and Strategic Failures

While the Zengin system has provided a reliable foundation since 1973, its aging architecture has reached a terminal limit where it can no longer support the demands of a digital-first economy. The system was designed for a different era of banking, and the costs of maintaining this legacy structure now outweigh the benefits of its historical stability.

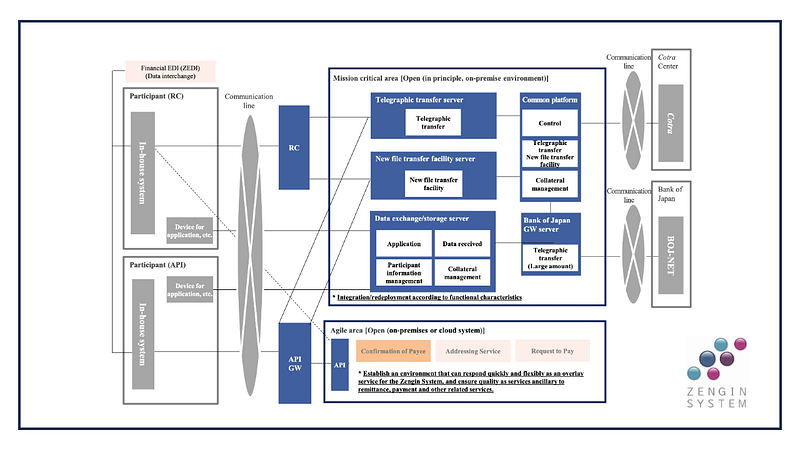

Current Zengin System Challenges

- Architecture (One-Way Constraint): The legacy system relies on "one-way" communication. Unlike modern bi-directional systems, it does not provide an automated delivery confirmation response from the receiver to the sender, creating uncertainty in transaction finality and preventing true Straight-Through Processing (STP).

- Innovation (Structural Rigidity): The use of fixed-length messaging formats makes it mathematically and financially prohibitive to add the "rich data" (e.g., invoice details, compliance info) required for modern automated reconciliation.

- Cost (Operational Overhead): Maintaining a complex web of "peripheral" and "sub-clearing" systems—including ZEDI for EDI data and integrated ATM switching services—creates massive operational redundancy.

- Regulation & Fragility: The 2023 Relay Computer (RC) failure served as a high-profile symptom of "architectural debt." The complexity of decades-old, "black box" code makes cause identification and recovery increasingly difficult, posing a systemic risk to national resilience.

A "Version-up" approach—attempting to patch the existing system—is strategically inferior to a total rebuild. The specialized skill gap required to maintain 50-year-old architecture is widening, leading to "Cost Inflation" as the pool of experts diminishes. A total rebuild is the only path to de-risking the national infrastructure and ensuring long-term sustainability.

2. Conceptual Framework of the New Settlement System (NSS)

The proposed New Settlement System (NSS) is envisioned as a "Public Utility" designed to serve as a high-performance, sustainable foundation for the next several decades of Japanese innovation.

The Three Pillars of the NSS

- Sustainability: Refresh the aging architecture to resolve the legacy skill crisis and ensure the system remains maintainable through modern software engineering practices.

- Competitive Advantage: Enable Japan to catch up with international FPS functional standards, ensuring the nation can participate in global financial networks and cross-border innovation.

- Social Utility: Address pressing national challenges. Specifically, mandate pre-validation to eliminate manual intervention in failed transfers and utilize structured data to enable automated reconciliation, directly mitigating the impact of Japan's labor shortage.

A fundamental shift in the NSS is the transition from Designated-Time Net Settlement (DNS) to a Pre-fund RTGS model. Architecturally, this involves a "Virtual Account" model managed on the clearinghouse ledger. This allows participating financial institutions to settle transactions 24/7/365 against pre-deposited liquidity without requiring the central bank’s primary RTGS system to remain active at all times. This shift fundamentally reduces intraday credit and liquidity risk across the entire network.

3. Functional Transformation: From Transactions to Data-Rich Services

The transition to the NSS shifts the focus of the clearinghouse from "Simple Funds Transfer" to "Data-Enhanced Settlement." This transformation turns a cost-center into a value-driver for the entire Japanese economy.

High-Value Features of the NSS

- Pre-Validation & Alias Payments (Day 1 Launch): Enables users to initiate transfers using mobile numbers or email addresses (Proxy/Alias) while validating the recipient's account existence before funds are sent. This is a critical Day 1 feature to reduce fraud and administrative overhead.

- Request to Pay (RtP) & QR Integration (Roadmap Expansion): While strategically vital for standardizing retail and B2B collections, these features will not be supported at initial launch to minimize the immediate technical burden on participants. They are, however, central to the long-term functional roadmap.

- Bi-Directional Messaging: Utilizing ISO 20022, the system supports real-time status updates (pacs.002), providing the essential ingredient for STP and automated accounting.

The Benefit Matrix

- Individuals: Gain 24/7/365 convenience and the security of knowing a recipient is validated before funds are committed.

- SMEs: Benefit from reduced administrative burdens through automated reconciliation. Notably, the NSS will allow the "Zengin format" to persist for the SME-to-bank leg initially to minimize the immediate migration burden.

- Large Corporations: Achieve global efficiency by utilizing international standards for liquidity management and data-rich messaging for global treasury operations.

4. Regulatory Compliance and International Interoperability (FATF & ISO 20022)

The NSS is a strategic necessity for meeting the revised FATF Recommendation 16 (The Travel Rule). Global regulators now mandate that detailed information about the sender and receiver must "travel" with the payment to prevent money laundering and terrorist financing.

The NSS provides the technical framework to clarify the "Start and End Points" for cross-border transfers involving funds transfer service providers. By adopting ISO 20022 (pacs.008/009), the NSS acts as a technical "shield," providing the data carrying capacity necessary to satisfy international sanctions screening and anti-money laundering (AML) requirements.

Infrastructure that lacks the capacity for rich data effectively invites "Regulatory Non-Compliance" and international sanctions friction. The NSS ensures that Japan's domestic leg of a cross-border transfer is no longer a "black hole" of information, securing Japan's standing in the global financial community.

5. Future-Proofing: Integrating Stablecoins and Tokenized Deposits

As private-sector digital money gains traction, the national clearinghouse must evolve into an Interoperability Layer that prevents the fragmentation of the Japanese Yen into isolated digital "silos."

The NSS External Linkage Strategy

- Stablecoins: The NSS will act as a bridge for issuance and redemption, ensuring that stablecoins issued by various providers can be converted back into central bank-backed or commercial bank money seamlessly.

- Tokenized Deposits: As banks begin to tokenize deposit claims, the NSS provides the common platform required to ensure that a "Tokenized Yen" at Bank A is exchangeable for a "Tokenized Yen" at Bank B.

By building a flexible, API-first architecture, Japan can incorporate "Innovations-turned-Commodities" as they mature. This prevents the need for another total system overhaul in ten years, allowing the NSS to absorb new technologies like Distributed Ledger Technology (DLT) via its interoperability gateway.

6. Implementation Strategy: Rebuild Justification & Risk Mitigation

The strategic decision to pursue a "Total Rebuild" over an "Incremental Upgrade" is justified by long-term ROI and national resilience. However, to ensure social stability, bulk-type payments (salaries, dividends, etc.) will remain on the legacy Zengin system for the time being, allowing for a phased and de-risked migration.

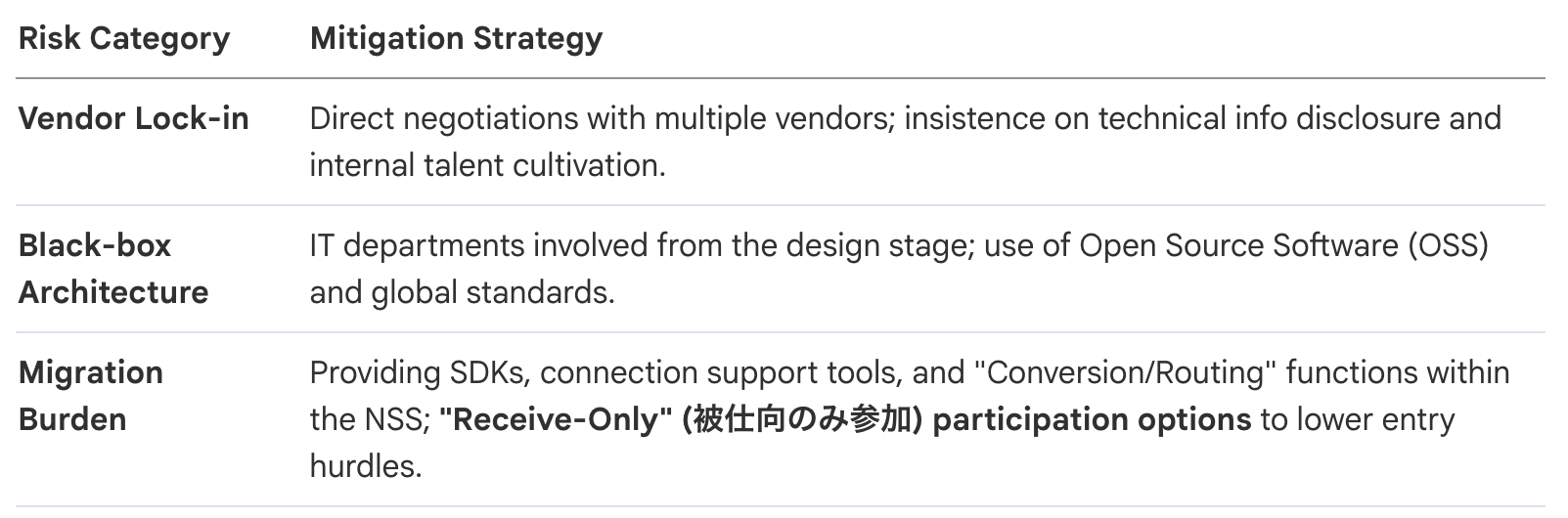

Risk vs. Mitigation

The success of the NSS ultimately relies on the "Network Effect." By offering the "Receive-Only" model, the NSS can rapidly achieve 100% participant reach across traditional banks and new funds transfer providers. This ensures that the system reaches the critical mass necessary to serve as the engine for Japan's modernized economy.