AEON Financial Service Targets JPY 100bn Profit by 2030 Amid Domestic Cost Reform and Rate Shifts

The fiscal year ending February 28, 2026, represented a critical "foundational building" phase for AEON Financial Service, set against the backdrop of Japan’s historic pivot from a zero-interest-rate environment to a "world with interest rates."

While top-line expansion remained resilient, the period was defined by structural shifts in the domestic banking sector and a concerted effort to modernize infrastructure. Performance was characterized by a successful defense of margins in a rising-rate environment, offset by the absence of historical securitization gains and increased procurement costs as the company prepares for its five-year "Vision 2030" transformation.

1. Fiscal Year 2025 Results

1.1 Consolidated Financial Results: Strategic Achievement and Margin Pressure

In a departure from previous years, AEON Financial Service moved toward a revenue base less dependent on securitization gains. While operating revenue saw a 7% year-on-year (YoY) increase, the operating profit trajectory highlights the impact of rising financial expenses and the normalization of credit costs.

Profitability and Cost Offsets

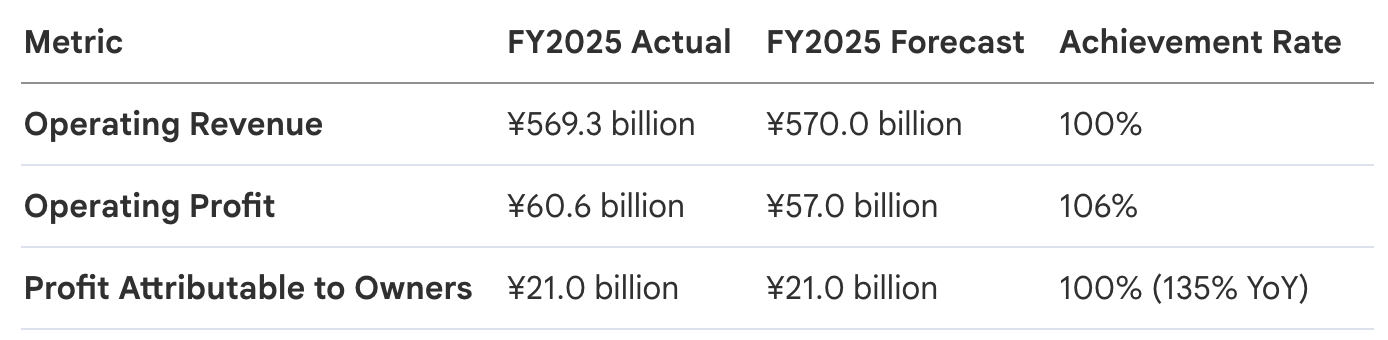

AEON Financial exceeded its revised operating profit forecast, achieving a 106% realization rate despite significant headwinds. The result was notably tempered by the absence of ¥9.9 billion in securitization gains that had bolstered the prior year’s results. The transfer of AEON Allianz Life Insurance resulted in a ¥9.7 billion revenue decrease; however, this was mitigated by a ¥12.3 billion reduction in related expenses, providing a net positive impact on the cost-to-income ratio. Profit attributable to owners reached ¥21.0 billion, a 135% surge compared to the ¥15.5 billion recorded in FY2024, largely due to the reduction of one-time extraordinary expenses.

1.2 Domestic Business: Yield Expansion vs. Rising Funding Costs

The domestic segment faced the dual challenge of navigating rising net interest margin (NIM) pressure while capturing higher yields in the retail lending space.

- Banking and Lending Dynamics: AEON Bank capitalized on its deposit-taking capabilities to shift toward high-yield receivables. The balance of these assets (including revolving/installment payments and unsecured loans) reached a record ¥883.8 billion after securitization. Average yields for revolving and installment payments expanded significantly by 1.37 percentage points. However, this yield expansion was countered by a ¥22.2 billion increase in financial expenses, driven by a 0.16 percentage point rise in domestic deposit interest rates—the primary structural threat to the banking segment in the current interest rate cycle.

- AEON Pay and Digital Integration: As part of the "AEON Living Zone" strategy, valid IDs grew to 59.51 million. AEON Pay transaction volume surged 154% YoY to ¥494.4 billion. Despite this growth, total in-house payment transaction volume reached ¥9.87 trillion, falling just short (99%) of the ¥10 trillion target, as inflation-driven consumer caution persists.

1.3 Overseas Operations: Regional Divergence and Asset Quality

Overseas revenue reached record levels across all territories, though regional profitability was split by local macroeconomic volatility and credit cost normalization.

- Regional Performance:

- Malay Area: Remained the primary growth engine with an 11% YoY profit increase, supported by robust demand for motorcycle and used car installment financing.

- Mekong Area: Operating profit was flat (100% YoY achievement). Performance was hindered by flood damage reserves in Thailand and a ¥900 million impact in Vietnam, which included goodwill expenses related to the PTF acquisition.

- China Area: Achieved a 116% YoY profit increase through aggressive cost-cutting and improved screening protocols, despite stagnant revenue growth.

- Asset Quality Synthesis:

- Hong Kong: NPL ratio declined following a tightening of credit assessment and early-stage delinquency measures.

- Thailand: Maintained stable NPL and expense ratios despite additional provisions linked to Middle East geopolitical volatility.

- Malaysia: The NPL ratio rose, but loan loss-related expenses were managed down through a review of loan classifications and improved recovery rates.

The FY2025 results reveal a company that has successfully stabilized its bottom line but remains burdened by an entrenched high-cost structure and the limitations of its legacy growth model. These missing operational efficiencies necessitated the "Vision 2030", as management shifts from "foundational building" to an aggressive digital-first acceleration phase.

2. Medium-Term Management Plan: The Pivot to "Vision 2030"

The new five-year strategy represents a fundamental review of AEON Financial’s operating model. The plan is a direct response to recent systemic failures, including the Financial Services Agency (FSA) Business Improvement Order issued to AEON Bank and the Q3 2024 card fraud response delays. Management has prioritized a "Safety and Security First" mandate as the non-negotiable prerequisite for its ¥250 billion digital transformation.

2.1 Root Cause Analysis: The Catalyst for Reform

Management’s internal post-mortem identified three systemic failures that led to significant shortfalls in previous targets:

- Delayed Digital Adaptation: A failure to respond to evolving payment structures and UI/UX needs resulted in poor cross-selling performance.

- Structural Inefficiency: Reliance on labor-intensive operations has kept the domestic labor cost ratio high and infrastructure costs fixed.

- Conventional Model Limitations: While competitors made large-scale digital investments, AEON’s overseas growth slowed due to a reliance on traditional business models.

To address these, the company is overhauling its "Three Lines of Defense" to eliminate fragmented risk management across subsidiaries, committing to a governance structure where business strategy and risk assessment are inextricably aligned.

2.2 Five Strategies for Value Creation

The roadmap to FY2030 leverages the "Retail x Finance x Digital" synergy to create a moat that traditional commercial banks cannot replicate:

- AEON Pay Ecosystem: Consolidating scattered services into a single app to reach 60 million members by 2030.

- AI-Driven Lending: Utilizing POS and behavioral data for real-time credit assessment in retail and Supply Chain Finance (SCF) for corporate partners.

- Asian Scaling: Establishing Malaysia, Vietnam, and Cambodia as priority investment hubs for the integrated digital bank model.

- Domestic Cost Reform: A targeted ¥36 billion cumulative cost reduction over five years.

- Robust Governance: Centralized risk management to prevent a recurrence of the "Major Incidents" of 2024.

2.3 Financial Targets and the JPY 250bn Investment Roadmap

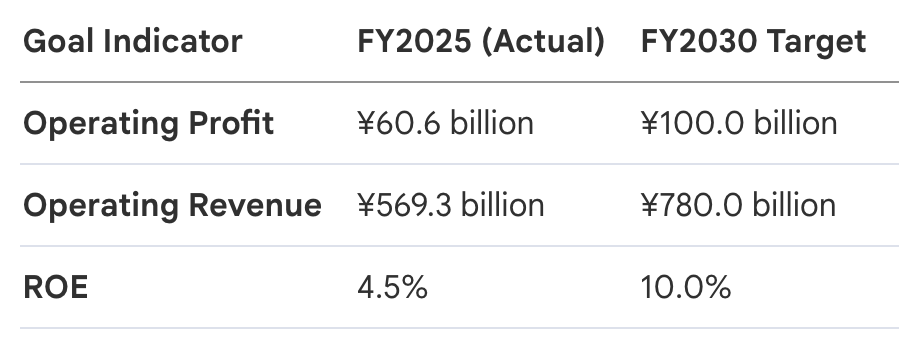

AEON Financial has set a trajectory for record-high profits by FY2028, culminating in an Operating Profit target of ¥100 billion by FY2030.

To realize these targets, the ¥250 billion digital investment plan is allocated as follows:

- Domestic (¥110 billion): Focusing on the cloud migration of financial infrastructure to enable high-capacity data utilization and AI-driven productivity.

- Overseas (¥80 billion): Scaling the retail-finance model in priority growth markets.

- Safety & Security (¥60 billion): Strengthening anti-fraud systems and group-wide governance infrastructure.

2.4 The Path to PBR Recovery

The market currently values AEON Financial at a PBR of 0.8x, reflecting a discount for its high-cost corporate structure. The "Vision 2030" KGI tree identifies the path to a PBR of 1.0x or higher through a combination of high-yield asset growth (targeting a +¥380 billion retail balance increase) and drastic cost reform. The primary mathematical objective is to lower the cost ratio from 9.0% to 7.2%, which management believes will drive the double-digit ROE required for a fundamental stock re-rating.

AEON Financial Service is navigating a high-stakes transition. The "Vision 2030" plan acknowledges that future profitability is contingent on executing a digital pivot while maintaining the industry's most rigorous safety standards. By bridging the gap between its vast retail ecosystem and advanced AI-driven finance, the company aims to fulfill its mandate of bringing "Finance Closer to Everyone."