DCJPY Trial Launches New Era: Tokenized Deposits in Security Settlement

Since the issuance of Japan’s first digital corporate bond in 2020, the nation’s security token (ST) market has faced a persistent structural bottleneck: a "decoupled" settlement process. While blockchain technology allowed for the instantaneous transfer of assets, the "cash leg" of these transactions remained trapped in legacy banking systems, requiring manual wire transfers and creating significant settlement risk. The successful integration of tokenized deposits marks the arrival of the "missing piece" in Japan’s digital finance puzzle—bringing fiat-backed programmability to the settlement layer and enabling the capital efficiency required for a modern secondary market.

On April 24, 2026, a consortium of six financial and technology leaders—including SBI Securities, Daiwa Securities, and SBI Shinsei Bank—announced the successful completion of Japan’s first "Delivery Versus Payment" (DVP) settlement for security tokens using "DCJPY" tokenized deposits. The verification, concluded in March 2026, utilized actual ST corporate bonds and tokenized currency rather than simulations. This milestone proves the technical viability of an atomic settlement architecture where the transfer of assets and cash occurs simultaneously, effectively eliminating the counterparty risks that have historically hindered the growth of the ST secondary market.

The achievement represents a shift from theoretical blockchain experimentation to a robust, practical infrastructure designed to synchronize asset and capital flows.

1. The Mechanism: DCJPY and DVP Integration

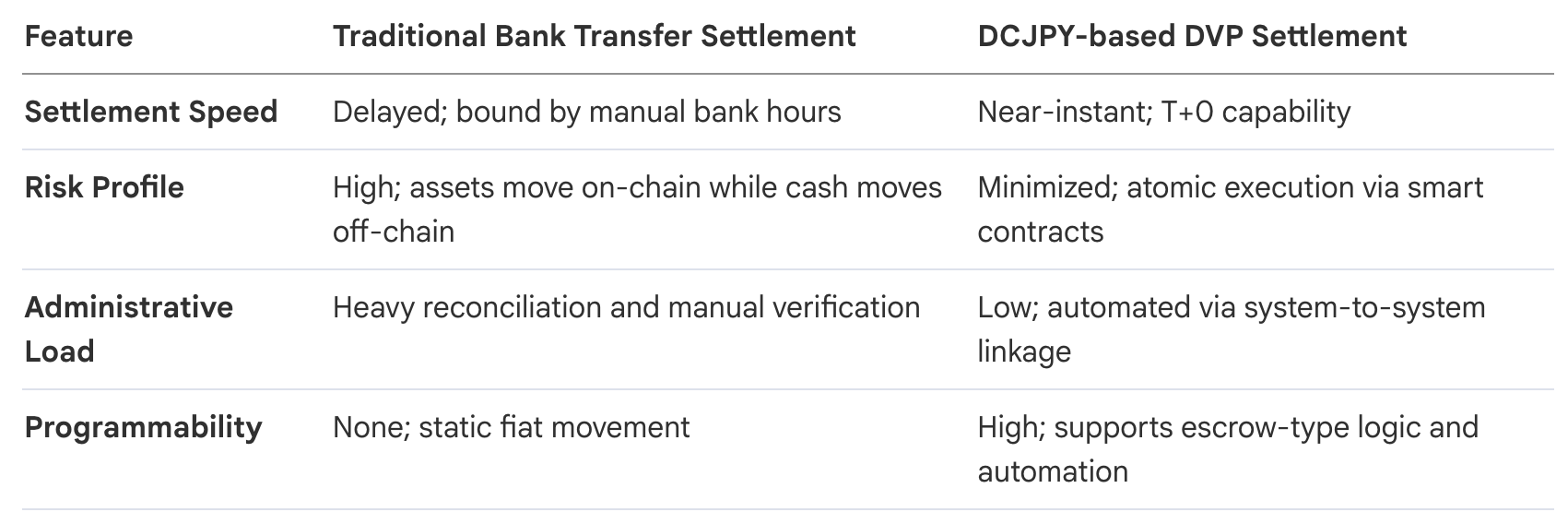

The imperative behind this trial was the elimination of the "settlement gap." In traditional digital bond transactions, the delivery of the security on a blockchain is often separated from the payment in fiat currency. This decoupling forces brokerages to manage high administrative burdens and capital charges due to the time lag between asset transfer and cash confirmation. By implementing blockchain-based DVP, the consortium enables "atomic settlement"—an "if-then" programmable logic where the security only moves if the payment is guaranteed.

The linchpin of this system is DCJPY, a tokenized deposit issued on the DeCurret DCP platform. DCJPY is a digital representation of actual liabilities at SBI Shinsei Bank. The process involves a specific movement where funds are transferred from a standard deposit account to a "dedicated account" (専用口座) for tokenization. This ensures the asset retains the accounting and legal stability of a bank deposit while gaining the programmable "superpowers" of a blockchain asset.

2. Consortium Architecture and Organizational Roles

The successful execution of this DVP protocol required an intricate web of interoperability between brokerage front-ends, banking cores, and specialized DLT platforms.

- SBI Securities & Daiwa Securities (Market Participants): Managed the acquisition and trading of ST corporate bonds. For these entities, the trial validates the ability to reduce capital charges by narrowing settlement windows.

- SBI Shinsei Bank (Issuer of DCJPY): Provided the critical link to the fiat system, managing the 1:1 issuance and redemption of DCJPY against bank-held deposits.

- BOOSTRY (Platform Lead): Developer of the 'ibet for Fin' consortium blockchain, the primary infrastructure for ST issuance and management.

- DeCurret DCP (Network Provider & Issuer): Acted as the issuer of the test ST corporate bonds and provided the "DCJPY Network," the programmable ledger where the tokenized cash resides.

- Osaka Digital Exchange (ODX) (Observer): Participated with a specific focus on integrating DVP settlement into Private Trading Systems (PTS), a crucial step for future institutional market structure.

3. Verification Outcomes: Testing the Secondary Market

Secondary market liquidity is the ultimate benchmark for security tokens. Without the ability to trade assets with near-instant settlement, institutional adoption will remain stalled. The March 2026 trial specifically targeted this hurdle by verifying a multi-stage trade flow involving actual ST Corporate Bonds issued by DeCurret DCP.

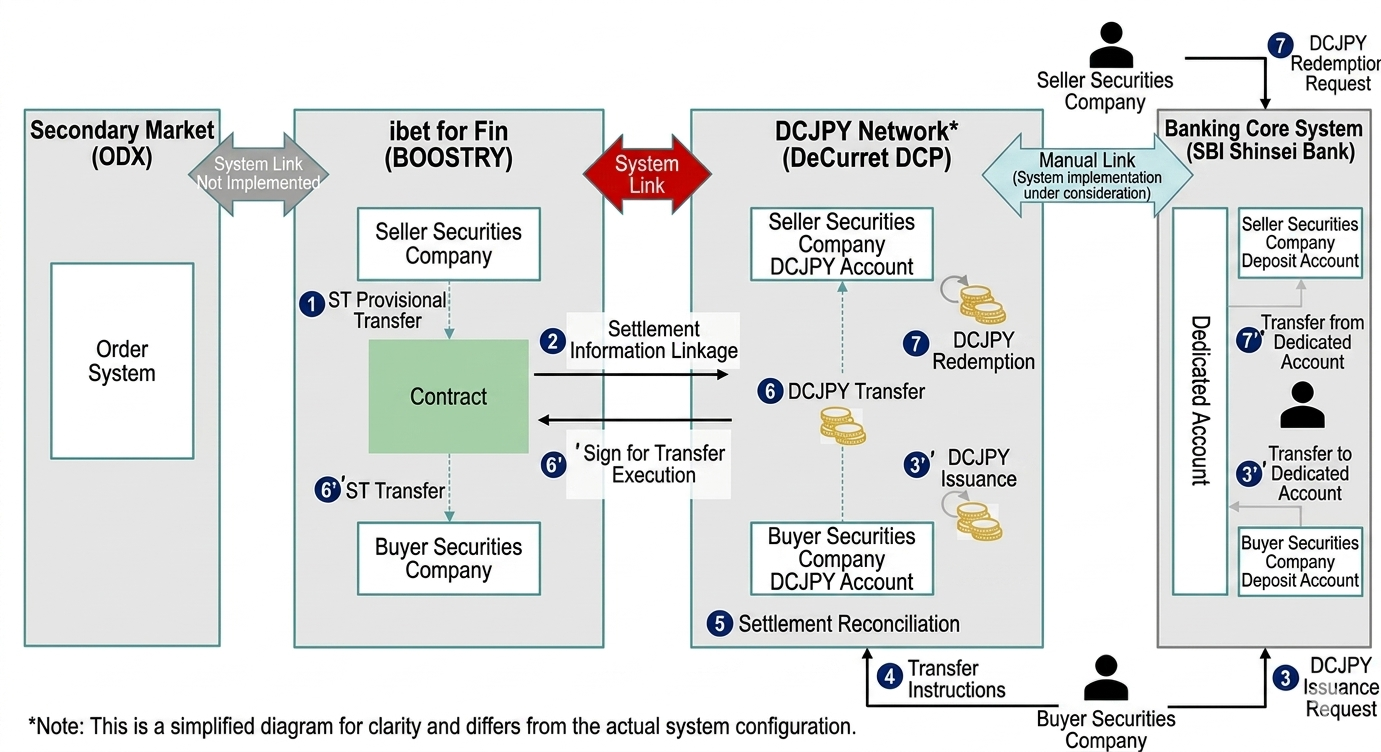

The verification confirmed a rigorous 7-step "escrow-type DVP settlement" process:

- ST Temporary Transfer: The seller initiates a "temporary transfer" (仮移転) of the bonds to a smart contract.

- Information Linkage: Data is synced between the 'ibet for Fin' platform and the DCJPY Network.

- DCJPY Issuance: The buyer triggers the issuance of DCJPY via a transfer to a dedicated bank account.

- Transfer Instruction: The buyer provides the instruction to move the DCJPY to the seller.

- Reconciliation: DeCurret DCP matches the settlement information across both networks.

- Atomic Execution: Simultaneous signature-based execution occurs; the bonds move to the buyer's wallet at the exact moment the DCJPY moves to the seller’s account.

- Redemption: The seller redeems the DCJPY for traditional bank deposits.

By successfully executing this flow in secondary and tertiary trades between Daiwa and SBI Securities, the consortium proved that the linkage between the 'ibet for Fin' asset platform and the 'DCJPY Network' is commercially viable and technically sound.

4. Roadblocks and the Path to Commercialization

Despite the breakthrough, the transition to full-scale commercialization faces significant "Back-office Integration" hurdles. The consortium’s post-mortem identified three primary areas requiring refinement before the system can replace current market infrastructure.

- Technical Refinements: Enhancing the automation of data linkage and improving the UI/UX to ensure that the settlement process is seamless for operational staff.

- Systems Integration: The "last mile" of connectivity involves plugging these DLT networks into the legacy "mainframes" of banks and existing national market infrastructure.

- Operational Governance: Establishing standardized rules for accounting, fund management, and authority/permission protocols to satisfy institutional compliance and audit requirements.

Future Direction

The consortium has signaled a "small start" approach. The immediate goal is to formalize an operational model for inter-brokerage DVP transactions among a limited group of early adopters. Long-term, the vision is to expand the participant base and standardize these protocols into a versatile, nationwide settlement platform that can interface with global markets.

The sentiment across the participants is one of high-octane commitment. As BOOSTRY noted, this trial has produced "standardized results" that will lead to a more reliable ST market. With the technical feasibility of the "cash leg" now proven, Japan is positioned to move from experimental pilots to a high-velocity, blockchain-native financial era.