Central Banks and the Future of Money

To architect the future of digital finance, we must first master the lessons of its history. As Governor Shin observed, "the further you want to look ahead, the further you have to look back." This historical lens reveals that money is a fundamental social institution—a coordination device comparable to a common language. Trust is the essential syntax of this language; for a monetary system to facilitate the division of labor and economic efficiency, users must maintain absolute confidence that a received payment can be seamlessly re-deployed.

This blog post captures the opening session of the Bank of Korea International Conference, held on June 1, 2026, featuring Governor Shin's opening address, Isabel Schnabel's keynote, as well as a policy dialogue between the two.

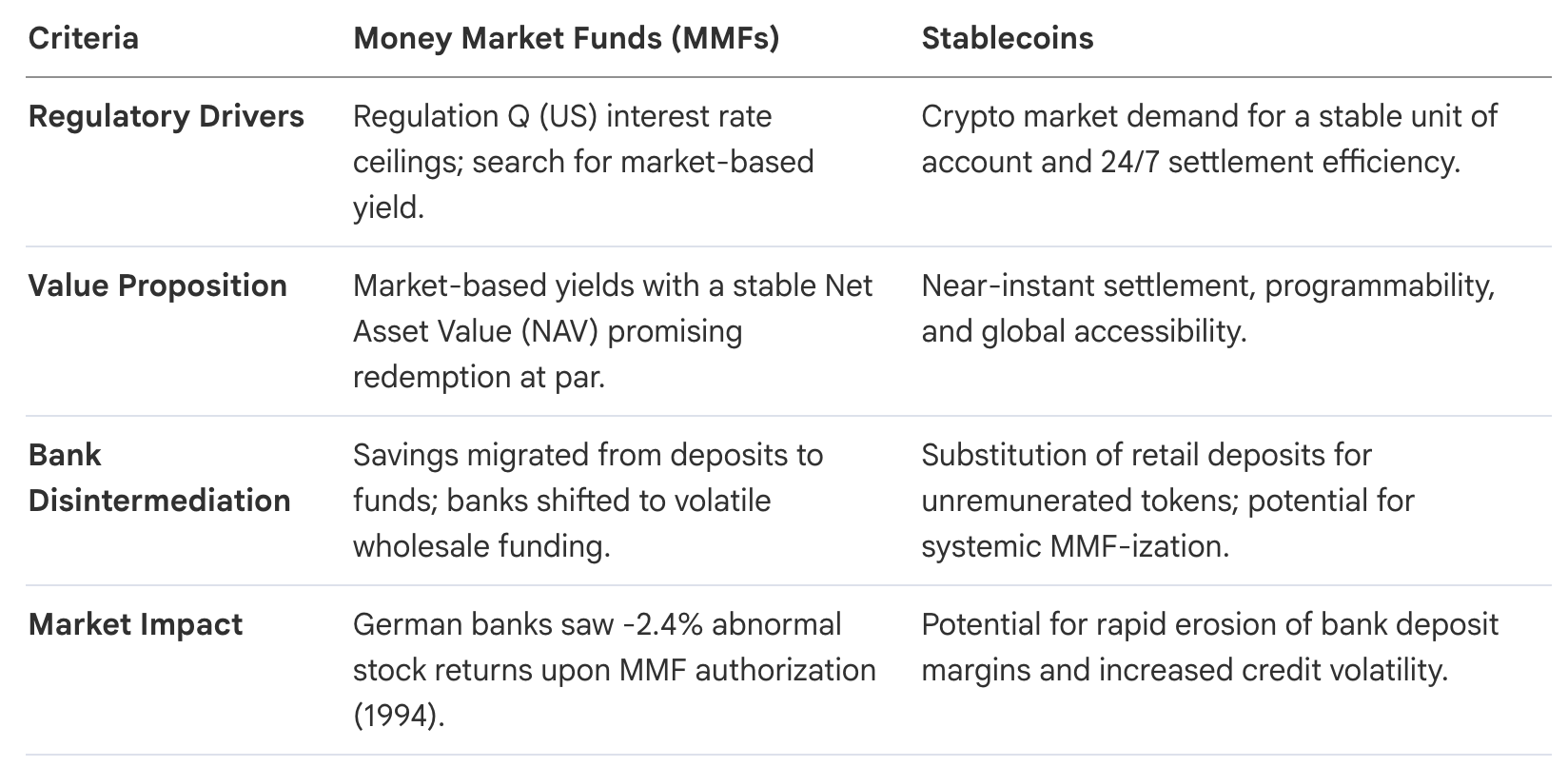

The rise of stablecoins is a modern iteration of the evolution of Money Market Funds (MMFs) in the US (1970s) and Europe (1990s). Just as MMFs emerged to circumvent interest rate ceilings, stablecoins represent a "search for efficiency" in a 24/7 digital economy.

History demonstrates that MMFs transitioned from niche instruments to systemic actors in wholesale funding. This trajectory informs the current $300 billion stablecoin market, where the transition from retail to wholesale funding is already altering market structures. However, the unique technological nature of stablecoins introduces specific fragilities—specifically the friction between instant digital settlement and traditional asset liquidity—that require a more targeted, proactive risk-mitigation strategy than the reactive policies of the past.

1. Analyzing Systemic Fragilities: Liquidity Mismatch and Financial Contagion

Financial stability within the two-tier monetary system relies on the "public anchor" of central bank money backing private innovation. Trust in underlying assets is the foundational requirement for any private money; the historical decline of the Bank of Amsterdam illustrates that even the most trusted proto-central banks can collapse if confidence in the quality and availability of reserve assets dissipates.

The most acute fragility in the stablecoin sector is the "liquidity mismatch." While stablecoins offer 24/7 instant settlement, their reserve assets (sovereign bonds, repos) typically operate on T+1 or T+2 cycles. This temporal friction creates a structural vulnerability during market stress, as issuers may be unable to liquidate assets fast enough to meet redemption waves, necessitating fire sales that trigger broader market spillovers.

We must distinguish between reserve compositions to accurately profile risk. While "USDC" is primarily backed by sovereign bonds and repos, its high-quality assets do not immunize it from contagion. "Tether" remains more opaque, holding illiquid and risky assets like commodities and loans, mirroring the risky lending that eventually doomed the Bank of Amsterdam.

Contagion Channels

- Bank-to-Stablecoin Contagion: Vulnerability arises when reserves are concentrated in a few institutions. USDC’s experience with Silicon Valley Bank proves that even perceived "safe" stablecoins can de-peg if their bank-held reserves are compromised.

- Stablecoin-to-Bank Contagion: A run on a major stablecoin leads to sudden, massive withdrawals of reserve deposits, potentially destabilizing the banks holding those reserves and triggering a systemic banking crisis.

These stability risks directly impair the efficacy of central bank policy by introducing unpredictable volatility into the financial plumbing.

2. Preserving Monetary Policy Integrity and Bank Intermediation

The "bank-based transmission" of monetary policy remains the primary engine for economic stability. Central banks rely on stable retail deposits to allow banks to perform maturity transformation. If this base is eroded, the credit supply to small and medium-sized enterprises (SMEs)—which lack access to capital markets—is structurally impaired.

Stablecoin integration introduces "Two Opposing Forces" on policy transmission:

- Strengthening Transmission (Wholesale Shift): As banks lose stable retail deposits to stablecoins, they become increasingly reliant on volatile wholesale funding. This funding is highly rate-sensitive and reprices rapidly, making the banking sector’s response to policy changes more reactive but also less predictable.

- Dampening Transmission (Substitution Effects): Unremunerated stablecoins often behave like overnight deposits. During contractionary shocks, holders may move back to yield-bearing bank deposits, weakening the central bank's intended tightening impulse.

A significant concern for the Digital Finance Architect is the "Zero Lower Bound." Unremunerated stablecoins create a de facto interest rate floor. If central banks implement negative rates, the stablecoin business model becomes unprofitable, risking market collapse. This effectively "MMF-izes" the entire retail deposit base, potentially paralyzing the central bank's ability to utilize negative rates, much as the US Federal Reserve’s reluctance to pursue such rates was influenced by the systemic scale of the unremunerated MMF industry.

3. The International Monetary Order and the Risk of Digital Dollarization

Monetary sovereignty in the digital age is determined by network effects and first-mover advantages rather than just economic fundamentals. As Isabel Schnabel argues, technological "inertia" can cement the dominance of a currency long after its economic peak.

Currently, US Dollar-denominated stablecoins command over 90% of the market, while Euro or Won-denominated alternatives remain negligible. This is not a reflection of superior economic policy, but of a technology-driven network effect. The consequences are twofold:

- Reinforced Hegemony: USD stablecoins strengthen dollar invoicing and global liquidity holdings at the expense of local currencies, even without a shift in underlying trade dynamics.

- Digital Dollarization: For emerging markets, the adoption of USD stablecoins represents a "Digital Dollarization" driven by technology adoption rather than deliberate policy. This weakens domestic monetary policy autonomy and increases the pass-through of foreign exchange volatility to domestic inflation.

Central banks cannot remain passive. Passive observation in a world of network effects is a recipe for the loss of monetary sovereignty.

4. Strategic Guardrails: Regulatory Frameworks and Infrastructure Responses

The strategic imperative for central banks is a shift from passive observation to active adaptation. The objective is to provide a public settlement asset that anchors and complements private innovation, ensuring the two-tier system remains robust.

Regulatory Frameworks

The EU’s MiCA (Markets in Crypto Assets) regulation serves as the architectural blueprint for containing private fragility:

- Reserve Quality: Strict mandates for high-quality, liquid assets.

- Liquidity Mandates: Requirements to hold 30% of reserves (60% for significant stablecoins) as bank deposits to facilitate redemptions.

- Transparency: Mandatory disclosure of reserve composition to prevent "Bank of Amsterdam-style" asset degradation.

Central Bank Infrastructure Roadmap

To preserve the anchoring role of central bank money, the Eurosystem is deploying a simultaneous dual-track response:

- The Retail Response: The Digital Euro A retail CBDC designed to preserve public access to central bank money. Its purpose is to ensure that the "common language" of money remains a public good, reducing dependence on non-European payment providers and preventing fragmentation.

- The Wholesale Response: Tokenized Central Bank Money This response ensures that central bank money remains the ultimate settlement asset for tokenized finance.

- Project Pontes (The Bridge): A short-term solution providing a technical bridge that links DLT platforms to "Target services" (the Eurosystem's RTGS), allowing immediate settlement of DLT transactions in central bank money.

- Project Appia (The Path): The long-term vision where central bank money, monetary policy implementation, and collateral management exist natively on tokenized platforms, ensuring interoperability between tokenized traditional assets and central bank liquidity.

Trust in the currency is not a byproduct of technology, but of the interaction between regulated private innovation and robust public anchors. By deploying CBDC infrastructure as a public settlement asset, central banks provide the necessary guardrails to prevent private stablecoin fragility from collapsing the two-tier monetary system.