Cracks in the Unlisted Equity Market: FUNDINNO's Q2 Slump and the Radical Pivot to M&A

FUNDINNO reported earnings for the second quarter of its fiscal year ending October 2026, covering its key performance indicators, specifically highlighting the growth in gross merchandise value (GMV) and the expanding number of registered professional investors across its primary and secondary equity platforms.

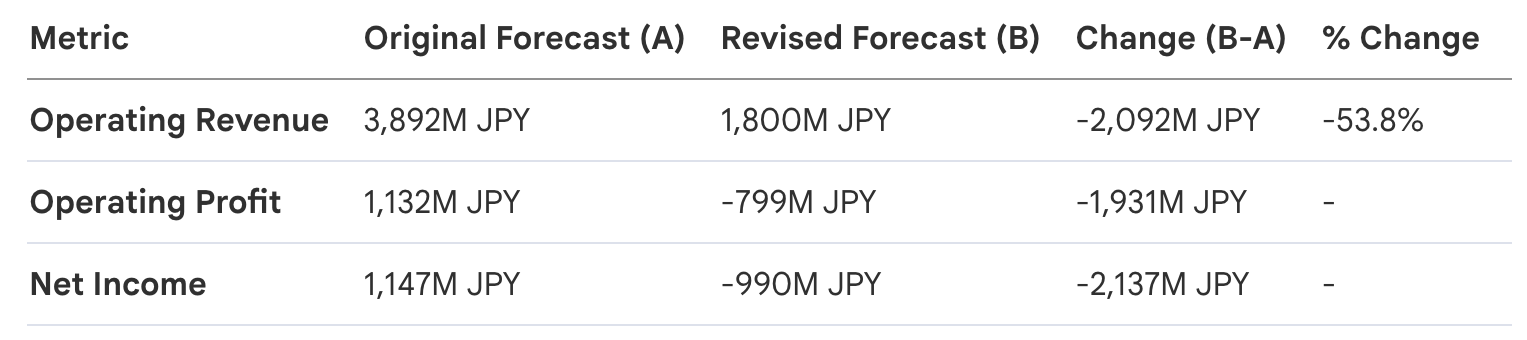

However, due to a challenging startup investment environment and shifting market conditions, the firm has issued a significant downward revision to its full-year earnings forecast. This financial adjustment includes the write-down of deferred tax assets and a projected net loss for the period. To address these difficulties and demonstrate accountability, the company's representative directors have committed to a voluntary reduction in their executive compensation.

Moving forward, FUNDINNO plans to accelerate strategic initiatives aimed at diversifying exit opportunities and strengthening its equity platform for unlisted companies.

1. A Hard Landing for Japan’s Equity Crowdfunding Pioneer

Fundinno (462A), once the standard-bearer for the democratization of Japanese venture capital, has reached a punishing "moment of truth." Its Q2 FY10/2026 results serve as a chilling bellwether for a systemic rot within the unlisted sector: a deep-seated valuation paralysis. While the Nikkei 225 scales historic heights, the platform model that Fundinno championed is witnessing a total decoupling from the public market’s exuberance.

Management brutally capitulated on guidance. The company has scrapped its projected 1.1 billion JPY profit, forecasting instead a nearly 1 billion JPY net loss. CEO Yuki Shibahara’s opening remarks admit to a sluggish response to market shifts, but the reality is more severe: Fundinno is trapped by the very "democratization" it preached. Retail investors are fleeing as the "valuation gap" between optimistic founders and cautious buyers freezes deal flow, forcing the company to seek lifelines from Corporate Venture Capital (CVC) and strategic partners. The following financial autopsy reveals a pioneer now acting as a distressed-market intermediary.

2. Financial Autopsy: Dissecting the Q2 Downward Revision

The financial fallout of H1 FY2026 is an exercise in institutional humility. The primary driver of the collapse is the total write-off of 188 million JPY in deferred tax assets (DTA). In the world of high-tier finance, this is typically seen as a formal admission by management that they no longer expect to generate sufficient taxable income in the foreseeable future to utilize those credits—a stark "vote of no confidence" in their own near-term recovery.

H1 Revenue Breakdown & Sector Performance

- Primary Domain (Fundinno / Fundinno Plus+): 682 million JPY. This is a catastrophic miss, representing a mere 19.3% progress toward the original full-year forecast.

- Growth Domain (Fundoor / MUFG Fundoor): 163 million JPY (45.3% progress). While seemingly stable, this was hampered by "contract development" (受託開発) delays in MUFG-related B2B projects, indicating that even institutional service revenue is not immune to operational friction.

- Secondary Domain (Fundinno Market): 53 million JPY. This is the quarter's lone bright spot. Management originally forecasted a negligible 1 million JPY for this segment; it delivered a 5,200% overperformance. This surge highlights a desperate market hunger for liquidity over new issuance.

The transition from these figures to the strategic failure of the "Plus+" engine reveals a broader market bifurcation.

3. The Valuation Chasm: Why the "Fundinno Plus+" Engine Stalled

The strategic failure of "FUNDINNO PLUS+"—the high-ticket engine meant to handle deals exceeding 1 billion JPY—is the direct result of a "Two-Speed Market." According to source disclosures, capital in Japan is currently bifurcating: money is flowing aggressively into policy-linked sectors like Deeptech, GX (Green Transformation), and Generative AI, while "general startups" are being starved. Fundinno, heavily weighted toward the latter, found itself on the wrong side of this divide.

The Narrative of Paralysis

- Factor A (Valuation Adjustment Delay): A "Founder-Investor Stalemate" has emerged. Many issuers remain anchored to the "High-Valuation Era" of 2021-2022 and refuse to accept down-rounds. Investors, meanwhile, have pivoted to "extreme selectivity," demanding unit economics and immediate profitability.

- The GMV Mirage: Total H1 2026 GMV sat at 4.15 billion JPY. This looks particularly bleak when compared to the record peak of 12.95 billion JPY in Q4 2025. Management now admits that the Q4 spike was an anomaly that set a false, unsustainable baseline for the FY2026 budget.

- Deal Flow Atrophy: The result of this valuation paralysis is clear: Fundinno closed only one deal over 1 billion JPY in H1 2026, compared to three in the preceding half-year.

These headwinds have rendered the "IPO-only" platform model obsolete, necessitating a radical shift toward the M&A horizon.

4. The M&A Pivot: Cap-Table Cleansing and the Corporate Shift

Faced with a frozen IPO market, Fundinno is weaponizing its secondary domain to serve as a pressure valve for the ecosystem. The core of this pivot is the new "Conflict Resolution Function."

Strategic Pivot Mechanics

- Cap-Table Cleansing: Fundinno is now using secondary sales to facilitate exits for early, high-valuation shareholders. By providing liquidity to "old" equity at adjusted prices, the platform can "clean" a startup's cap table, resolving the founder-investor stalemate and making the company attractive to M&A buyers who were previously deterred by messy stakeholder disputes.

- The Corporate Shift: The target investor base is shifting from retail "Specific Investors" to "Strategic Partners" (CVCs and business corporations). The goal is twofold: securing larger checks and finding buyers interested in "business synergy" rather than immediate IPOs. This also solves the "Shareholder Bloat" problem—M&A exits are significantly easier when a company isn't burdened by hundreds of individual retail shareholders.

- Response Policies: New policies for issuers prioritize M&A-oriented deal structures and the use of "Fund-based" investment to consolidate the shareholder register into a single line item.

5. Accountability and the Path Forward: Executive Penance and AI Efficiencies

To salvage investor trust following a guidance failure of this magnitude, Fundinno has turned to executive penance and a desperate technological overhaul to slash burn rates.

Executive Accountability

Representative Directors Yuki Shibahara (CEO) and Manabu Oura (COO) have both committed to 15% monthly compensation reductions from June to October 2026. This joint penance is intended to signal a "return to basics" as the company faces its first major crisis since listing.

The Path to Profitability (DX & AI)

Management is doubling down on "AI-driven DX" to handle labor-intensive back-office and sales processes. By replacing the existing CRM and SFA platforms, Fundinno hopes to decouple its future growth from headcount costs. The goal is to transform the company from a labor-heavy brokerage into a lean, data-driven financial intermediary.

KPIs to Watch

- Specific Investor Count: Growth has slowed to a crawl, with only 274 new registrations in H1 (total: 1,895). Without regaining this momentum, the "Plus+" engine remains dead.

- Secondary-Primary Integration: The success of the "Conflict Resolution" function will be the ultimate test of whether Fundinno can bridge the valuation chasm.

Fundinno has evolved. It is no longer a starry-eyed crowdfunding site for the masses; it is now a distressed-market intermediary. Its survival depends entirely on its ability to force founders into the reality of lower valuations and facilitate the M&A exits that Japan's "Two-Speed Market" now demands.