Inside the Growth Market: the 28th "Council of Experts Concerning the Follow-up of Market Restructuring"

The recently held Market Restructuring Council discussed the findings of a 2026 survey conducted by the Tokyo Stock Exchange to identify the primary hurdles facing companies in the Growth Market.

Data gathered from 145 organizations reveals that while business strategy and resource shortages are significant concerns, the most pressing issues involve investor relations and market valuation.

Many firms struggle with low stock liquidity, a lack of access to institutional investors, and share prices that fail to reflect their actual progress. To address these gaps, respondents requested more practical seminars, sector-specific best practice case studies, and better networking opportunities with peer companies.

Ultimately, the report highlights a broad need for management mindset shifts regarding capital efficiency and more robust support systems to enhance the long-term appeal of the Growth Market.

1. The Strategic Imperative of Market Restructuring

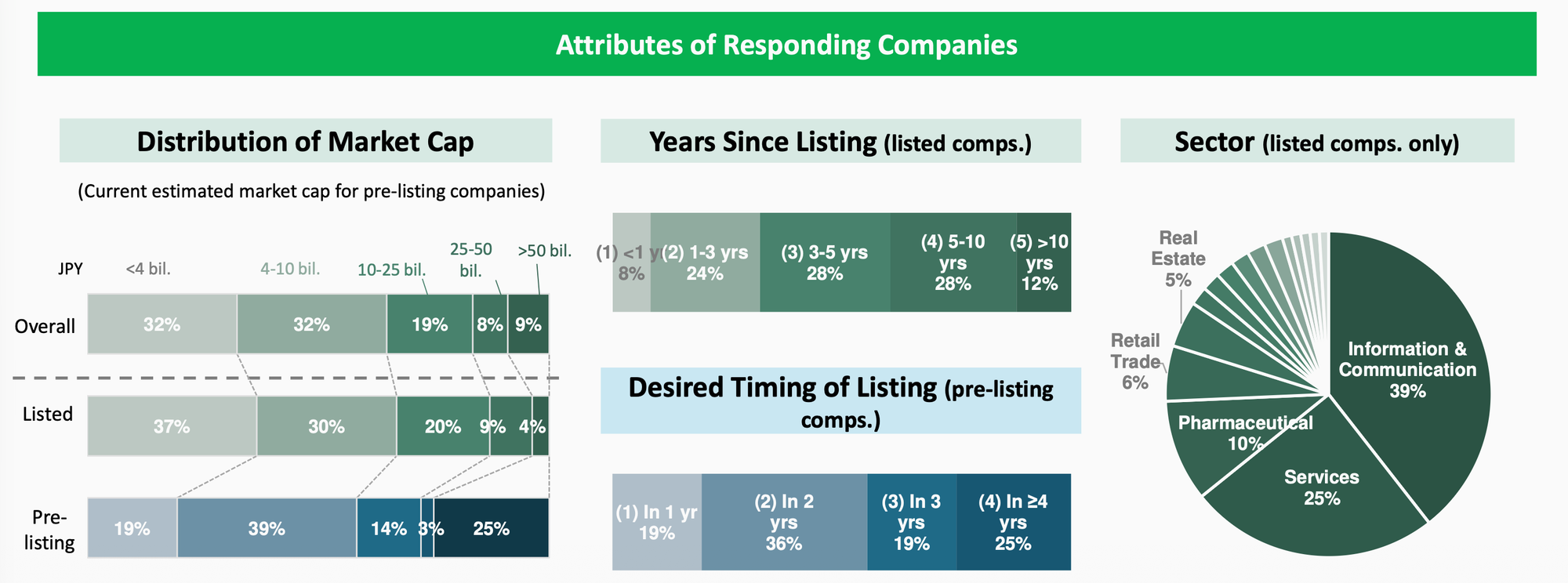

As Japan seeks to invigorate its venture ecosystem, this comprehensive survey of 145 companies—comprising 109 currently listed entities and 36 pre-listing startups—provides a raw, data-driven look into the friction points of capital formation. By capturing the voices of management teams across the full lifecycle of a growth company, the participants' responses address the practical hurdles of going and staying public.

To understand the breadth of this diagnostic tool, one must look at the diverse attributes of the responding companies:

The inclusion of sectors ranging from traditional retail to cutting-edge deep tech, including aerospace and biotechnology, is essential for a representative policy shift. This diversity ensures that the TSE is not merely catering to "standard" software startups but is also addressing the unique, capital-intensive needs of R&D-driven ventures. This demographic foundation sets the stage for an exploration of the operational struggles faced by companies navigating the Growth Market.

2. The Post-Listing Paradox: Growth Constraints and Investor Disconnect

There is a stark dissonance between the intent of a Growth Market listing and the operational reality for many firms. While listing is meant to provide the fuel for expansion, many companies report being "preoccupied" with short-term results and the immediate pressure of attaining forecasted figures, leaving little room for mid- to long-term strategic debate.

2.1 The Resource Chasm

Growth is frequently stifled by a persistent "Resource Chasm" that affects both operations and strategy:

- Talent Scarcity: Intense competition for IT talent acts as a primary bottleneck for business expansion.

- Regional Constraints: Companies headquartered in regional areas report significant barriers to recruitment, leaving staffing situations "strained" and hindering growth acceleration.

- M&A and Expansion Bottlenecks: A lack of specialized resources and expertise for choosing deals and managing post-merger integration (PMI) prevents companies from pursuing inorganic growth strategies.

2.2 IR and Valuation Friction

The survey highlights a significant disconnect between corporate performance and market valuation, as captured in company feedback:

"Growth Market companies are highly susceptible to external environmental factors... it is difficult for a company's intrinsic value to be reflected in its stock price. As a whole, the Growth Market tends to see a lot of short-term-focused trading, with limited inflows from institutional investors."

Specific frustration is directed at the impact of short selling, particularly within the biotech sector, where "minor disclosures" can trigger massive price fluctuations. This volatility discourages individual investors and destabilizes long-term corporate value, making it difficult for intrinsic value to be reflected in the stock price.

This disconnect creates a "growth stop." Many companies target niche markets where growth plateaus once they cover the market, or they operate with "easily imitable business models" that lose their first-mover advantage. Without a compelling growth story, these firms struggle to reach the JPY 10 billion market cap threshold required by the 2030 criteria, creating a looming existential threat for smaller listed entities.

3. Strategic Recommendations for Listed Entity Support

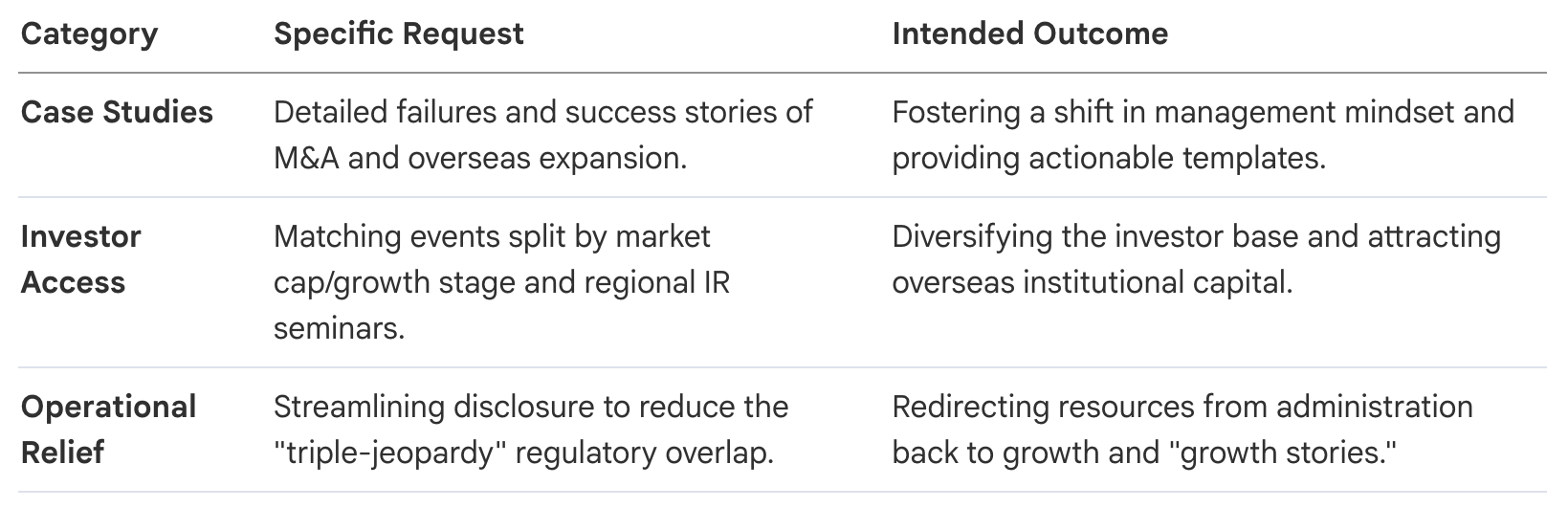

As companies struggle with these systemic issues, their demands for support have shifted from "general theory" toward a desire for practical, replicable case studies that can guide management through complex transitions.

3.1 Demanded Support Pillars

3.2 The Investor Access and Disclosure Gap

The request for "Increased Contact with Investors" is particularly acute for mid-cap companies (JPY 30-100 billion range) that seek formal analyst coverage to attract overseas institutional capital. Simultaneously, the regulatory environment has become a "significant burden." The overlap between the Companies Act (financial statements and business reports), the Financial Instruments and Exchange Act (securities and semiannual reports), and TSE regulations (kessan tanshin and timely disclosure) creates a redundancy that hinders the "accuracy and earlier disclosure" of growth narratives. This triple-layered reporting requirement traps management in administrative loops rather than allowing for the agile communication of corporate value.

4. The Pre-Listing Frontier: Navigating the "Black Box" of IPOs

For startups, the journey to an IPO is often described as a "telephone game." Caught between the conservative pressures of securities firms and the perceived "strict stance" of the TSE, many pre-listing companies find themselves navigating a process shrouded in uncertainty.

The survey identifies several friction points for pre-listing companies:

- The Underwriter Gap: Securities firms often pressure companies into conservative stances by claiming "TSE might view it as a problem," even when no such rule exists. This creates a "black box" environment for issuer representatives.

- The Institutional Minimum: A high-impact friction point involves "internal rules" of lead underwriters. In certain cases, IPOs were cancelled after approval because underwriters required a specific percentage of the offering to be taken by institutional investors—a rule difficult to satisfy for companies whose post-listing base is expected to be primarily individual investors.

- Formalism vs. Volatility: Startups critique a "formalistic approach" toward internal controls, such as requiring detailed monthly checks or avoiding written board resolutions. This is particularly problematic for the AI industry, where high volatility makes it difficult to match forecasts with actual results. A rigid examination process that expects exact alignment is fundamentally at odds with the nature of high-growth tech sectors.

The scarcity of exit strategies other than IPOs forces "small-scale IPOs." VCs often urge immature companies to rush to the public market prematurely to provide liquidity, rather than waiting for the optimal scale.

5. Frameworks for a Mature Venture Ecosystem

The Council’s findings point toward the necessity of a "middle market" that bridges the gap between pre-IPO and post-IPO stages, providing liquidity for employee stock options and executive shares before a formal public debut.

5.1 Proposed Interventions

To revitalize the ecosystem, stakeholders have proposed several tactical interventions:

- Pre-IPO Governance Best Practices Guide: A framework for founder-led startups to implement CEO evaluation and succession planning without stifling autonomy.

- Support for Overseas VC Engagement: Facilitating referrals to international capital to help late-stage companies raise tens of billions of yen without being forced into a premature IPO.

- Technical Modernization: A specific operational request for TDNet to provide multi-OS support (specifically Mac compatibility) to accommodate the modern technology stacks used by current startups.

5.2 Final Synthesis: Beyond Surface-Level Governance

The report concludes with a warning against a "simplistic perception" of M&A. Mergers should not be viewed as a mathematical shortcut to meet listing criteria; the market capitalization of a merged entity "cannot necessarily be expected" to exceed the sum of the individual companies.

Ultimately, the credibility of the Growth Market depends on moving beyond surface-level governance. The Council’s findings emphasize that "appropriate price formation" is only possible when companies provide transparent, high-quality growth stories and the TSE provides the institutional framework to ensure those stories reach the right investors. The focus must remain on market quality, ensuring that listing remains a launchpad for sustained expansion rather than a growth-stifling end goal.