Japan FinTech Observer #47

Welcome to the forty-seventh edition of the Japan FinTech Observer.

Welcome to the forty-seventh edition of the Japan FinTech Observer.

50 yen. That is how close the Nikkei came on February 16 to the bubble-era all-time high, before settling back a few hundred points. As the market is increasingly priced for perfection, the penalty for any mis-step also gets more severe. Enter Sony, which shed around USD 10bn in market capitalization by delivering mediocre results in their gaming division, amid rising doubts whether they have the capability to fully monetize their intellectual property. Nintendo followed on Monday (but that could be a topic for next week’s Observer).

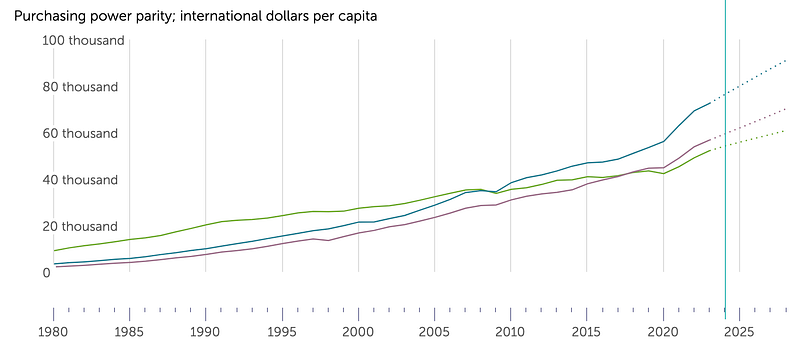

Big news! Japan has fallen behind Germany to become the fourth-largest economy by GDP…..on a nominal basis, with quite a bit of currency weakness as a key contributing factor. On a PPP basis, Japan is still ahead. However, the trend we have been following for a long time is the GDP per capita, in particular in comparison to regional powers South Korea and Taiwan. While on a nominal basis, using IMF data, it is a nearly dead race, with all three countries coming in at around USD 34k, on a PPP basis Taiwan (blue) had overtaken Japan in 2009, and South Korea (red) followed suit in 2018. This is a powerful illustration of the long-term decline in Japan’s international competitiveness.

GDP per capita (PPP basis)

Here is what we are going to cover this week:

- Venture Capital & Private Markets: MUFG Bank takes 15.55% stake in WealthNavi; Mizuho Bank invests up to INR 12 billion in Credit Saison’s Indian subsidiary Kisetsu Saison Finance; KYCC raised a total of JPY 420m from DEEPCORE, JIC VENTURES Growth Investments, NVCC, and others; leading South Korean venture capital firms have identified Japan as their prime target for investment expansion; East Japan Railway Company (JR East) establishes a Corporate Venture Capital (CVC) entity based in Singapore; Ajinomoto set up a new corporate venture capital (CVC) base in Silicon Valley; PowerX has raised an additional JPY 9.5bn through loans from major Japanese financial institutions

- Insurance: The “New Sompo Japan” under new leadership and a new mid-term management plan running from FY2024 to FY2026 aims to bring cross-shareholdings down to zero; Sony obtained approval from the Minister of Economy, Trade and Industry of Japan regarding its Corporate Restructuring Plan for the spin-off of its financial services business

- Banking: Resona enters into retail banking strategic alliance with JUROKU; Kiyo Bank, a regional bank headquartered in Wakayama, will begin an initiative to enhance the calculation of financed emissions with Persefoni

- Payments: PayPay brought home a third consecutive (and third in its history) profitable quarter; Stripe announced that it has been selected by Tokyu Corporation

- Capital Markets & Asset Management: the Government of Japan announced the completion of its first-ever Climate Transition Bond offering; the Tokyo Stock Exchange has published its second monthly “Status of Disclosure” report, with 84 new TSE Prime names added to the previous list published on 15 January; Bloomo, a startup developing an asset building app focusing on US stocks/ETFs, is finally launching in Japan

- Digital Assets: Resona Bank has started a real estate security token business; cryptocurrency exchange bitFlyer announced the listing of its first stablecoin; Nicolas Bertrand has stepped down as Nomura-backed Komainu’s chief executive; Deloitte has developed a baseball-themed NFT game app, a pioneering project on the Astar Foundation zkEVM; Kochi prefecture is moving into the metaverse

- The Last Word: Global Maritime Financial Centers

Training the M&A Muscle Memory

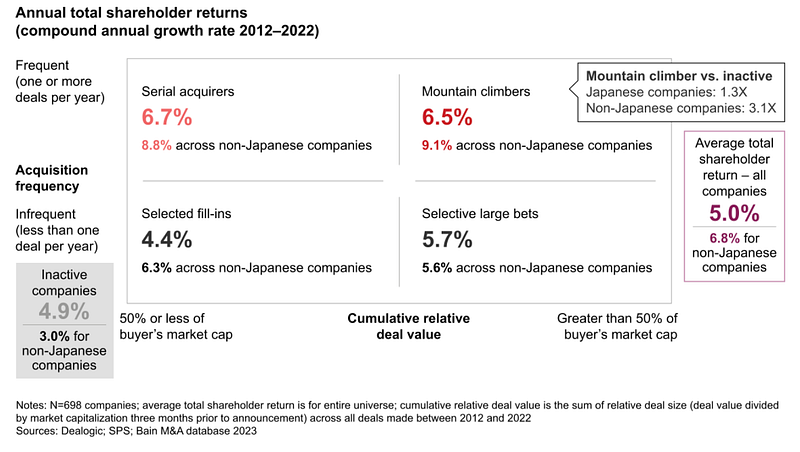

Bain studies of M&A’s contribution to total shareholder returns (TSRs) since 2004 show that frequent acquirers gain a performance advantage over infrequent or inactive acquirers, reflecting the increasing sophistication of their M&A capabilities over time.

Frequent acquirers deploy a repeatable model across the full M&A process — that is, strategy, screening, diligence, and integration — to maximize value creation, but because Japanese companies have been both less active and less mature in their M&A capabilities than their global peers, the TSR benefits are muted as well.

Even the most active Japanese companies — Bain calls them “mountain climbers” — are not yet achieving the advantage of frequent and material acquirers in other regions. For example, mountain climbers in Japan yielded an average TSR 1.3 times the TSR of inactive Japanese companies over the years 2012 to 2022. By comparison, non-Japanese mountain climbers saw returns that were on average 3.1 times that of inactive companies. It’s a situation that will change as Japanese acquirers begin to advance along their journey of building M&A muscle.

Venture Capital & Private Markets

- MUFG Bank takes 15.55% stake in WealthNavi; the partners also reached an agreement on the development and provision of a Money Advisory Platform to solve customers’ financial issues throughout their lifetime, as well as promoting use of its robo-advisor services and “Robo-NISA,” through a combination of MUFG’s wide-ranging customer base and product lineup and WealthNavi’s outstanding capabilities in agile planning and product development

- Mizuho Bank, a subsidiary of Mizuho Financial Group, and Credit Saison have come to an agreement for Mizuho Bank to invest up to INR 12 billion in Credit Saison’s Indian subsidiary Kisetsu Saison Finance (equivalent to JPY 21 billion; equity ratio: equivalent to 15%); in addition, Mizuho Bank will dispatch one director to Credit Saison India, and plans to make it an equity method affiliate

- KYCC raised a total of JPY 420m through a third-party allotment in the Series C investment round; a total of four companies will underwrite the investment: existing investor DEEPCORE, new investors JIC VENTURES Growth Investments, NVCC, and one other operating company

- Leading South Korean venture capital firms have identified Japan as their prime target for investment expansion; this shift comes as Japan, previously seen as lacking in startup activity, is swiftly enhancing its startup ecosystem, fueled by the demand for digital transformation and supportive government policies; Korean VCs are not only investing in Japanese venture funds but are also setting up their funds directly; major Korean VC firms like Atinum Investment, IMM Investment Corp., and Shinhan Finance Venture Investment made strides in Japan by establishing their venture funds

- East Japan Railway Company (JR East) establishes “JRE Ventures Pte. Ltd.,” a Corporate Venture Capital (CVC) entity based in Singapore, which promotes investment in and accelerates collaboration with startups, primarily active in Southeast Asia, where the startup ecosystem has been growing; JRE Ventures sets the capacity of JPY 5 billion dedicated to its investment activity, focusing on startups win the domain of “Lifestyle Solutions

- Ajinomoto set up a new corporate venture capital (CVC) base in Silicon Valley in January 2024; until now, Ajinomoto has been conducting CVC operations from its base in Japan, and the establishment of a new corporate base in Silicon Valley will enable the Company to globally develop partnering strategies with startups and collect information on cutting-edge innovation

- PowerX has raised an additional JPY 9.5bn through loans from major Japanese financial institutions; the funds raised will be used to accelerate the mass production of PowerX’s liquid-cooled battery modules starting from mid-2024; this financing is arranged by Mitsubishi UFJ Morgan Stanley Securities, with the participation of MUFG Bank, JA MITSUI LEASING, The Chugoku Bank, Mitsubishi HC Capital, The Iyo Bank, The Shoko Chukin Bank, and BOT Lease acting as credit investors

Insurance

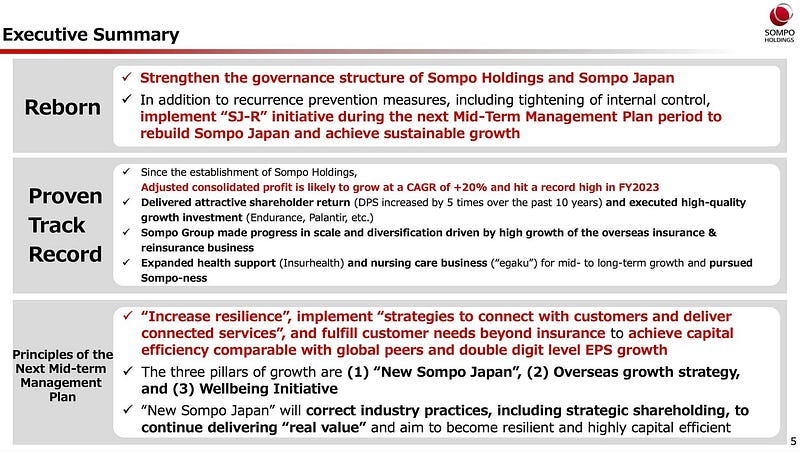

- The “New Sompo Japan” under new leadership and a new mid-term management plan running from FY2024 to FY2026 aims to bring cross-shareholdings down to zero

- Sony obtained approval from the Minister of Economy, Trade and Industry of Japan regarding its Corporate Restructuring Plan for the spin-off of its financial services business (SFGI); Sony has begun concrete preparations for the execution of the listing of the shares of SFGI by October 2025; under the plan, Sony will distribute slightly more than 80% of its shares of SFGI to Sony’s shareholders through dividends in kind; in December, Sony had agreed to sell its payment services business to Blackstone, keeping a similar minority stake

Banking

- Resona enters into retail banking strategic alliance with JUROKU, which has a solid business foundation in the Chukyo region and whose management philosophy is “achieving growth and prosperity for customers and the local community,” in which both companies will cooperate in the physical and digital domains, mutually utilize information and know-how, and further contribute to the local economy and sustainable growth

- Kiyo Bank, a regional bank headquartered in Wakayama, with the support of SCSK Corporation, will begin an initiative to enhance the calculation of financed emissions (i.e., greenhouse gas emissions from the investment and loan portfolios of financial institutions) by utilizing the greenhouse gas (GHG) emissions calculation platform provided by Persefoni, a company that offers a climate management and carbon accounting platform (CMAP) for enterprises, financial institutions, and government agencies

Payments

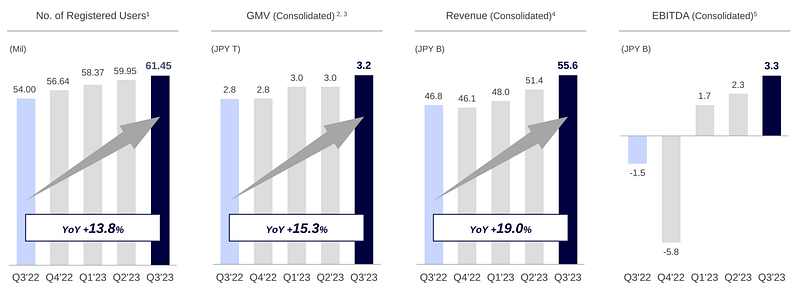

PayPay — Financial Results Q3/FY2023

- PayPay brought home a third consecutive (and third in its history) profitable quarter on disciplined spending for account and merchant acquisitions; PayPay registered users exceeded 60m for the first time, and PayPay Card members 11m; the revolving balance on cards and lending from PayPay Bank have been dialed up substantially over the last twelve months, up 45.5% and 32.1%, respectively; with only about 13% of PayPay users also having opened a PayPay Bank account, there is plenty of growth potential in the ecosystem

- Stripe announced that it has been selected by Tokyu Corporation to power the multinational conglomerate’s new flat-rate subscription accommodation service; TsugiTsugi chose to implement multiple Stripe solutions: Billing to manage subscription billing, Checkout to create checkout pages that can be easily modified to display new subscription plans, and Radar to prevent credit card fraud

Capital Markets & Asset Management

- The Government of Japan announced the completion of its first-ever Climate Transition Bond offering, raising JPY800 billion (USD$5.3 billion) in proceeds aimed at funding efforts to support the country’s transformation to a carbonneutral economy, with a particular focus on decarbonizing hard-to-abate industrial sectors; the issuance of the 10-year bond marks the first tranche in a planned $11 billion transition bond funding round, kicking off the government’s plan to raise as much as JPY20 trillion (USD$133 billion) to fund climate transition efforts over the next decade

- The Tokyo Stock Exchange has published its second monthly “Status of Disclosure” report, with 84 new TSE Prime names added to the previous list published on 15 January; this brings the percentage of companies with disclosed initiatives (we continue to discount “under consideration”) to 44%, up from 40%, and it also includes companies with significantly higher price-book-ratio, such as Daikin and Asics; given the market performance over the past year, the tradable universe of low PBR stocks is becoming quite small

- Bloomo, a startup developing an asset building app focusing on US stocks/ETFs that had raised a JPY 800m seed round in April 2023, and announced that it has completed the registration as a Type 1 Financial Instruments Business Operator (FIBO) in June 2023, has declared that it is finally ready for a limited release of its app to waitlist participants

Digital Assets

- Resona Bank has started a real estate security token business: Resona provides customers with a method of raising funds using real estate trusts, and also offers digital securities (security tokens) that allow small-lot investment in real estate; Resona Bank utilizes its “trust function” and “real estate function” to provide services related to the issuance and management of security tokens as a trustee, as well as provide investment instructions as an asset manager

- Japanese cryptocurrency exchange bitFlyer announced the listing of its first stablecoin, DAI, starting on February 19

- Nicolas Bertrand has stepped down as Nomura-backed Komainu’s chief executive

- Deloitte has developed a baseball-themed NFT game app, a pioneering project on the Astar Foundation zkEVM; this game includes a digital baseball batting practice system where players earn NFT ‘Emblems’, adding a new growth element to the experience of young players improving their batting skills

- The Oasys blockchain, backed by big-name gaming firms Ubisoft and SEGA, saw its OAS token hit an all time high after it announced a partnership with Korean game developer Com2us Corporation

- Kochi, Japan, will move into the metaverse space, with city officials sealing a web3 deal with the Philippines-based Start Lands; the parties said a “virtual Kochi” would likely be open for online visitors by the summer of 2024

The Last Word: Global Maritime Financial Centers

Z/Yen, which for the last 16 years has published two Global Financial Centres Index (GFCI) reports a year, has partnered with the Busan Finance Center for a report on developments in maritime finance & maritime financial centers. For the top 20 maritime financial centers, this study relies on rankings provided by Menon Economics and DNV, which are compared against the GFCI.

The top 12 maritime financial centers are as follows:

- Singapore (3rd in GFCI)

- Rotterdam

- London (1st in GFCI)

- Shanghai (7th in GFCI)

- Tokyo (20th in GFCI)

- Hong Kong (4th in GFCI)

- Oslo (42nd in GFCI)

- New York (2nd in GFCI)

- Hamburg (49th in GFCI)

- Copenhagen

- Busan (30th in GFCI)

- Athens

If you would like to see more of our content, please head over to the Tokyo FinTech YouTube Channel or check out the eXponential Finance Podcast.

We have also created two LinkedIn groups, the “Japan Startup Observer” if your interest in Japan goes beyond FinTech, and the “FinTechs of India” to capture the developments on the subcontinent. We invite you to join both these groups.

Have an awesome week ahead.