Japan Outlines 2040 Economic Outlook under New Growth Strategy and Annual JPY 10trn Fiscal Plan

Japan’s Cabinet Office has released its medium- to long-term economic and fiscal projections through fiscal year 2040. The report analyzes the macroeconomic impact of regular government outlays paired with a mechanical assumption of ¥10 trillion in annual real-term additional fiscal spending starting in FY2027.

The calculations are modeled across three distinct economic growth paths, depending on the efficacy of the government’s growth initiatives:

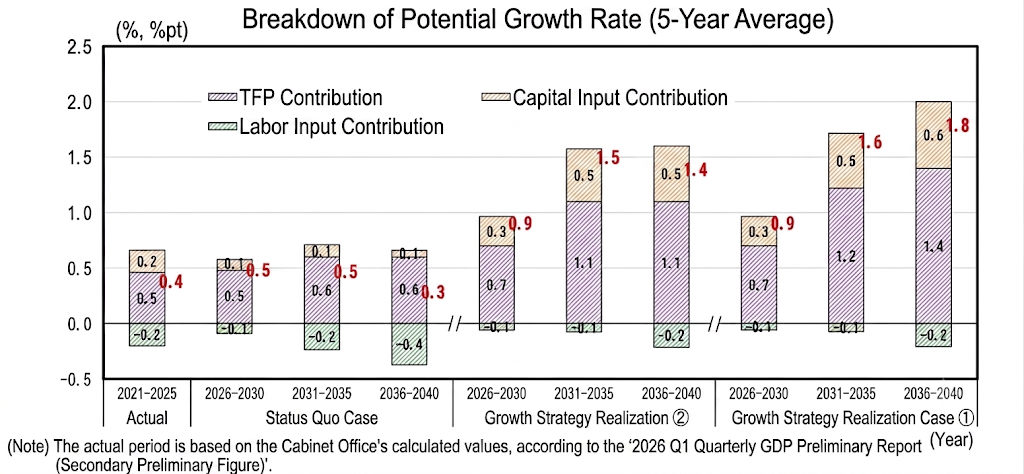

Three Projected Paths for Japan's Economy

Growth Strategy Realization - Case #1

This scenario assumes full integration of the government's growth strategy alongside private sector investment. Driven by AI adoption and innovative technologies, the Total Factor Productivity (TFP) growth rate is projected to rise to 1.1% in roughly five years and reach 1.4% thereafter. Under this path, real GDP growth will rise to the upper 1% range over the medium to long term. Annual nominal private non-residential investment is forecasted to reach over ¥230 trillion by FY2040, driving nominal GDP close to ¥1,100 trillion.

Growth Strategy Realization - Case #2

In this intermediate scenario, the benefits of the public-private investment roadmap materialize, but market uncertainties cap the TFP growth rate at 1.1% after five years. Real GDP growth is expected to stabilize in the mid-1% range. By FY2040, nominal private non-residential investment is projected at approximately ¥220 trillion, with nominal GDP reaching around ¥1,040 trillion.

Baseline Projection Case - Case #3

Assuming that only the demand-side benefits of the additional fiscal spending occur, corporate investment appetite remains flat. TFP growth stays stagnant in the mid-0% range , while real GDP growth hovers in the lower 0% range. In this scenario, FY2040 nominal private investment and nominal GDP are limited to roughly ¥170 trillion and ¥900 trillion, respectively.

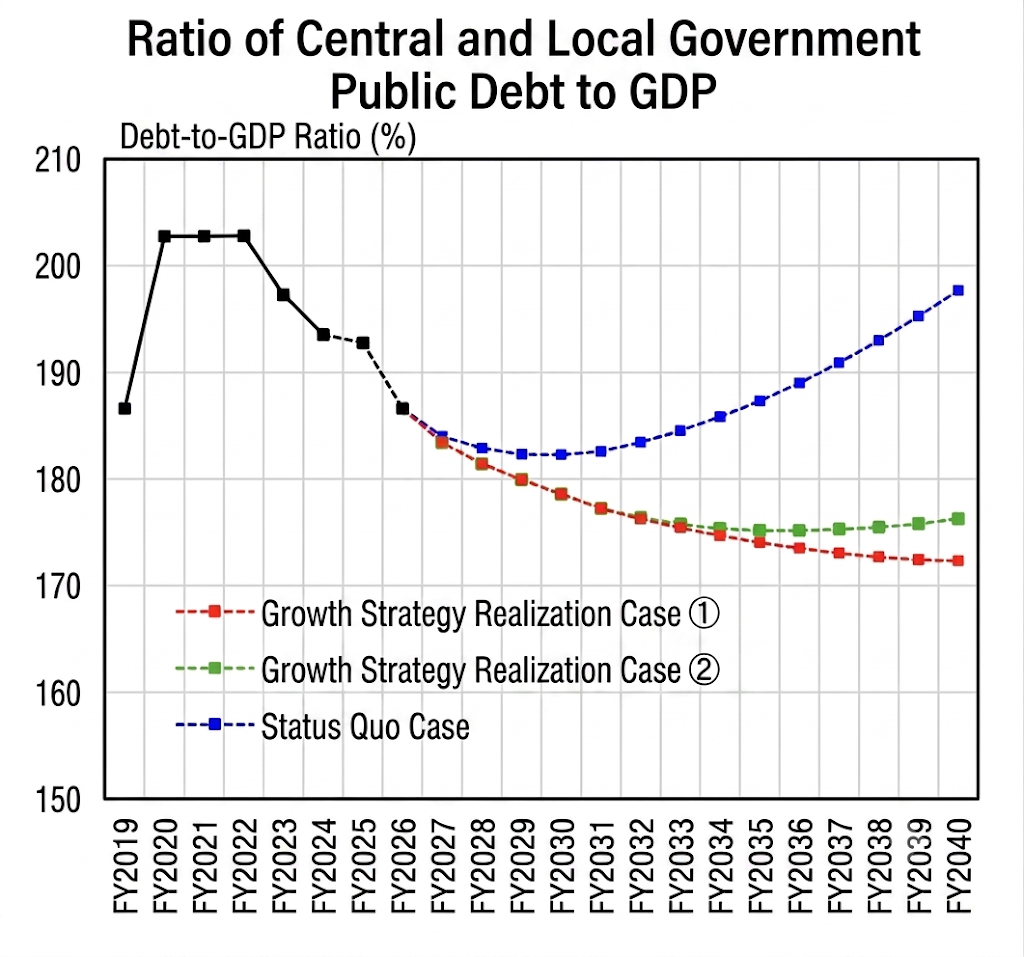

Fiscal Sustainability and Debt Dynamics

The report notes that if sufficient economic growth is achieved (as outlined in Cases #1 and #2), the government and local authority debt-to-GDP ratio will generally follow a steady downward trajectory, even with the added annual fiscal expansion.

Specifically, under Case #1, the debt-to-GDP ratio falls consistently before experiencing a narrower margin of decline in the late 2030s. In contrast, the debt ratio turns upward around the mid-2030s under Case #2, and begins escalating as early as FY2030 under the Baseline Projection Case.

Regarding the primary balance (PB) to GDP ratio, both Growth Strategy cases project short-term deficits followed by a shift into positive territory from FY2028 onward. The surplus is expected to expand through the mid-2030s, after which it will continue expanding in Case #1 but flatten in Case #2. Under the Baseline Case, the primary balance deficit is projected to widen.

The overall fiscal balance deficit relative to GDP is projected to widen gently through FY2040 in both Growth Strategy scenarios, whereas it will expand steadily under the Baseline Projection.