Japan’s Gentle Recovery Collides with Middle East Geopolitical Volatility

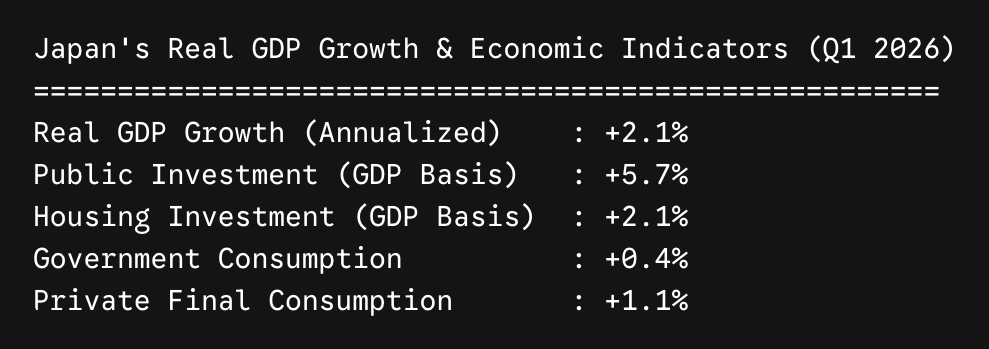

Japan’s economy expanded at an annualized rate of 2.1% in the first quarter of 2026, marking its second consecutive quarter of growth. This expansion was driven by resilient domestic consumption, capital investment, and a rebound in exports to the United States following a slowdown induced by earlier tariffs. However, this recovery faces heavy headwinds due to prolonged Middle East tensions, according to a report by the Development Bank of Japan (DBJ) published today.

Economists project that growth will slow from the second quarter onward, with a moderate rebound expected toward the end of the year. If energy supply constraints drag out, substantial downside risks remain for the broader economy.

Domestic Economy: Consumption and Investment Expand Amid Output Pressures

Industrial Production Flatlines

Industrial output dipped 0.4% month-on-month in March, logging its second consecutive monthly decline. The drop was led primarily by the chemical sector, which has been directly impacted by the geopolitical crisis in the Middle East. While downstream paint and printing ink industries saw a brief spike in demand from buyers hedging against future shortages, steep production cuts in upstream naphtha (-18.7%) and midstream basic petrochemicals (-22.7%) present significant pipeline risks. Government efforts to secure alternative supply chains are underway, but production cuts are poised to impact further downstream.

Conversely, manufacturing forecasts predict a 2.1% output rebound in April—boosted by semiconductor-manufacturing equipment—and a 2.2% rise in May, led by transport equipment.

Mixed Real Estate and Infrastructure Signals

- Public Investment: Real public investment grew by 5.7% annualized in Q1, bouncing back after a three-quarter downturn to sit mostly flat. Leading indicators, including public works contract values and rising defense spending, point to a steady upward trajectory.

- Government Consumption: Up 0.4%, government spending is expected to remain on a growth path, sustained by rising social security costs and expanded fiscal subsidies aimed at capping consumer price inflation.

- Housing Investment: Real housing investment grew 2.1% annualized in Q1 as it continued to recover from a sharp drop-off following the April 2025 mandatory compliance with energy efficiency standards. However, actual housing starts remain weak, held back by high construction costs, rising mortgage rates, and supply constraints on oil-related building materials like paints and insulation.

Labor Market Tightness Delivers Real Wage Growth

The domestic labor market remains exceptionally tight. March’s effective job-openings-to-applicants ratio ticked down slightly to 1.18x, while the unemployment rate edged up to 2.7%. Despite these minor fluctuations, overall employment figures reflect broad improvement.

Crucially, nominal wages surged by 2.7% year-on-year in March, driven by gains in regular scheduled pay. Outpacing inflation, real wages logged their third consecutive monthly expansion. This positive wage momentum is expected to persist, bolstered by the fifth round of spring wage negotiations (Shunto), which yielded an average wage hike of 5.05%—marking the third straight year above the 5% threshold.

Retail Resilience Met with Faltering Consumer Sentiment

Real private consumption grew at a modest 1.1% annualized rate in Q1, directly supported by improving real wages. In retail, March real sales rose slightly month-on-month. Food and beverages experienced a temporary lift from rush demand ahead of a tobacco tax hike, while unseasonably warm weather propelled spring apparel sales. Automotive retail also saw growth, with further gains anticipated in April following the elimination of the environmental performance tax rating.

Despite these positive figures, consumer anxiety is spiking. The Consumer Attitude Index slid for a second consecutive month in April as Middle East uncertainties took hold. The ratio of households anticipating price increases of 5% or more shot up dramatically after March, dragging down overall sentiment. Similarly, the Economy Watchers Survey’s current conditions DI dropped for two straight months, with respondents highlighting rising airfares and an increased focus on household budgeting.

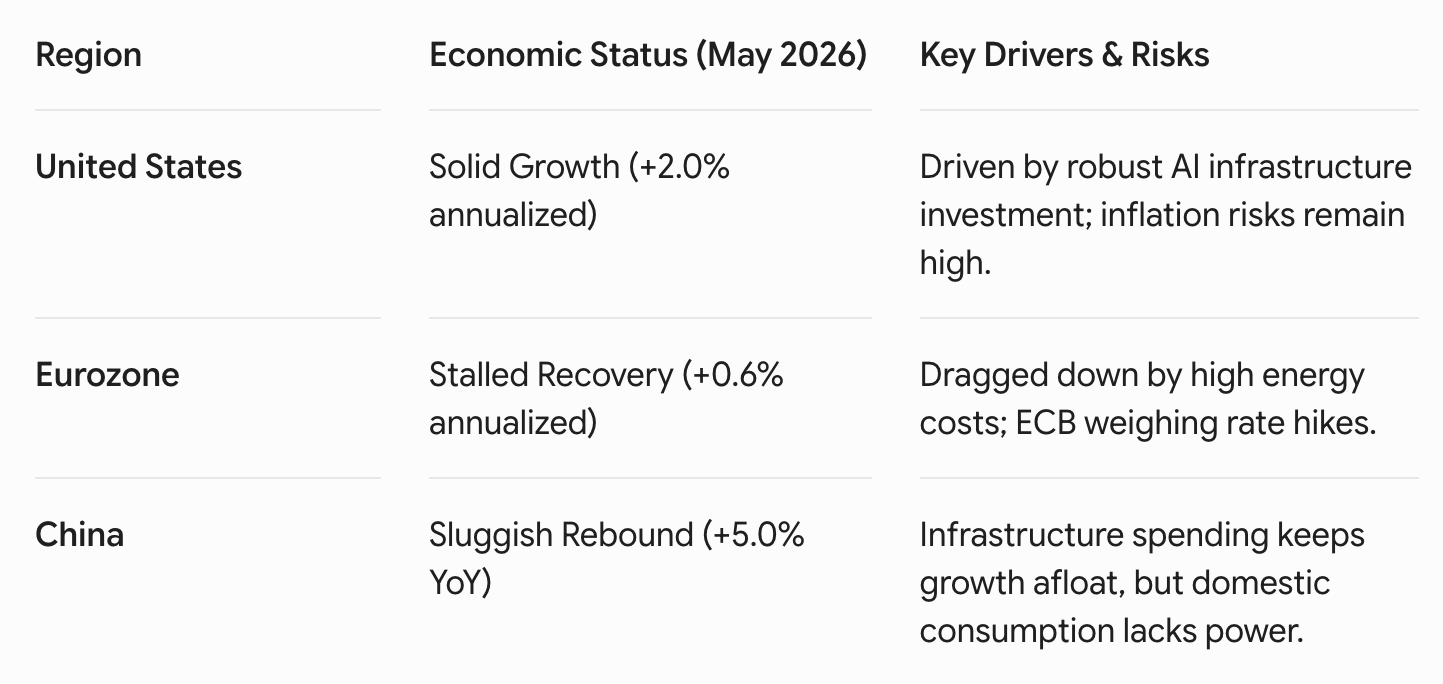

Global Divergence: U.S. Holds Steady While Europe and China Settle

United States: AI Infrastructure Spending Anchors Growth

The U.S. economy displayed solid resilience, with real GDP expanding 2.0% annualized in Q1. Government spending rebounded following the resolution of a previous government shutdown, and capital expenditure accelerated sharply on the back of relentless artificial intelligence infrastructure demand. Hyper-scaler capital expenditure budgets for 2026 are tracking significantly above 2025 levels, boosting demand for information processing equipment and software.

However, inflation continues to flare. April consumer prices climbed 3.8% year-on-year, up from 3.3% in March, driven by rising energy and food costs alongside stubborn housing rents. Producer prices jumped 6.0% year-on-year, signaling further downstream price pressures. While high gasoline prices and tapering tax refunds are expected to cool retail consumption through the second quarter, the U.S. remains insulated from the worst of the energy crisis as the world’s leading crude oil producer.

Europe: Stalled Growth and Energy Vulnerabilities

The European Union’s recovery is stuttering, with Q1 GDP growth slowing to a minor 0.6% annualized rate. While a fiscally expansive Germany managed a modest turnaround (+1.3%), the tourism-driven growth boom previously enjoyed by Southern European nations like Spain has begun to taper. Reflecting this slowdown, the International Monetary Fund (IMF) downgraded its 2026 Eurozone growth forecast from 1.5% to 1.3%.

Compounding the growth slowdown, Eurozone inflation accelerated to 3.0% in April, driven entirely by skyrocketing energy costs. In response, the European Central Bank (ECB) maintained its policy rate for the seventh consecutive meeting but actively discussed the necessity of rate hikes to counter upside price risks, with markets pricing in action as early as June. Structurally, while Europe’s overall reliance on Middle Eastern crude is low (accounting for roughly 10% of imports) and strategic crude inventories remain above the 90-day threshold, a heavy dependence on Middle Eastern jet fuel presents a notable supply risk.

China: Rebound Softens Despite Export Recovery

China’s real GDP grew 5.0% year-on-year in Q1, up from 4.8% in the previous quarter, lifted by front-loaded state infrastructure spending and equipment upgrades. However, this fiscal momentum reversed in April, with fixed-asset investment turning negative. The real estate market also remains severely depressed.

On the trade front, Chinese exports surged 14.1% year-on-year in April. Shipments to ASEAN, Europe, India, and Latin America remained highly resilient, easily offsetting a sharp decline in trade with the Middle East. Furthermore, recent bilateral progress at the U.S.-China summit—including tariff reductions, the removal of non-tariff barriers, and commitments to purchase U.S. agricultural goods and Boeing aircraft—is expected to revive underperforming trans-Pacific trade routes.

Market Dynamics: Yield Curves Steepen as Equities Hit Records

Sovereign Bond Yields Surge

Long-term government bond yields climbed sharply across both sides of the Pacific. In the U.S., hotter-than-expected inflation data pushed the 10-year Treasury yield past 4.6% in mid-May. In Japan, yields experienced an even sharper shock; driven by domestic inflation fears and media reports of an upcoming supplementary expansionary budget, the 10-year Japanese Government Bond (JGB) yield spiked to a 29-year high of 2.8% before settling slightly.

Market Note: A comparison of the JGB yield curve between late February and mid-May reveals a pronounced steepening. Short-term yields remained tightly anchored, indicating that the market is not pricing in aggressive near-term Bank of Japan rate hikes. Instead, the steepening reflects a growing term premium demanded by investors wary of long-term inflation and fiscal expansion.

Corporate Earnings Fuel Equity Rallies

Despite geopolitical headwinds, equity markets in both Tokyo and New York marched to historic highs in mid-to-late May. A granular decomposition of the TOPIX and S&P 500 moves indicates that this rally is fundamentally sound. While price-to-earnings (PER) multiples contracted temporarily at the onset of the Middle East crisis, valuations have since normalized. The primary driver of the equity push has been a sharp upward trajectory in forward earnings-per-share (EPS) since late 2025, powered by corporate earnings in the AI, semiconductor, and technology sectors.

Currency Interventions Offer Only Temporary Relief for Yen

The Japanese Yen faced intense depreciation pressure throughout the spring, collapsing past the 160 per dollar threshold in late April. This slide was driven by safe-haven dollar demand and a steady pushback of Federal Reserve rate cut expectations. The slide prompted massive, unannounced joint interventions by the Ministry of Finance and the Bank of Japan, which deployed an estimated 10 trillion yen across multiple operations to squeeze short positions and drive the currency back to 155.

However, the relief proved short-lived. Due to a widening trade deficit caused by high crude prices and wide interest rate differentials, persistent commercial dollar-buying resumed. By late May, the Yen had retraced its gains, trading back down near the 159 per dollar level.

Energy Markets: WTI Settles Near $100

Crude prices surged to a temporary peak of $119 per barrel following the escalation of tensions in the Middle East. Although prices moderated after initial ceasefire talks, negotiations have since stalled, keeping West Texas Intermediate (WTI) crude tracking around the $100 mark.

According to the U.S. Energy Information Administration’s (EIA) May outlook, global oil inventories are projected to experience major drawdowns through mid-2026, even assuming a June reopening of the Strait of Hormuz. While a projected recovery in global supply is expected to lower prices eventually, the EIA forecasts WTI to sit at $81 by the end of 2026 and $70 by the end of 2027, indicating that cheap energy is unlikely to return anytime soon.