Japan’s three mega banks to stop issuing paper bills and checks

Japan’s three mega banks are expected to stop issuing paper bills and checks in FY2025, with customers seen shifting to electronic payments…

Japan’s three mega banks are expected to stop issuing paper bills and checks in FY2025, with customers seen shifting to electronic payments and bank remittances.

SMBC said Thursday that it will completely end the issuance of paper bills and checks at the end of September 2025. It has already stopped issuing paper bills and checks to new account holders. MUFG Bank and Mizuho Bank are slated to make similar announcements soon, reports Jiji Press.

With the official deadline set for the end of FY2026, the move by the mega banks is seen as creating additional impetus for regional banks to follow suit.

The most recent “Study Group on ‘Full Digitization’ of Check and Bill Functions”, hosted by the Japanese Bankers Association (JBA) at the end of June, showed mixed results in the progress of participants. The meeting covered:

- Public awareness and promotional activities for FY2024 (Secretariat explanation)

- Revision of the voluntary action plan (Secretariat explanation)

- Q&A and exchange of opinions

Public awareness and promotional activities for FY2024

The secretariat explained the following regarding public awareness and promotional activities for FY2024 towards full digitization:

In FY2023, based on the results of the survey on the actual use of checks and bills, further awareness activities were carried out in cooperation with the government and industry. Individual banks also accelerated measures towards full digitization of checks and bills. In FY2024, the government, industry, and financial sectors will continue to cooperate in raising awareness about the abolition/digitization of checks and bills with one voice, and compile an interim evaluation by the end of the fiscal year.

FY2024 is an important year for interim evaluation. To accelerate the speed of digitization of checks and bills, awareness and promotional activities will be carried out focusing on the following four pillars:

- Targeted regional and industry-specific awareness and promotional activities

- Broader awareness and promotional activities to increase social recognition

- Support and educational activities by financial institutions

- Awareness and promotional activities in cooperation with the government (ministries)

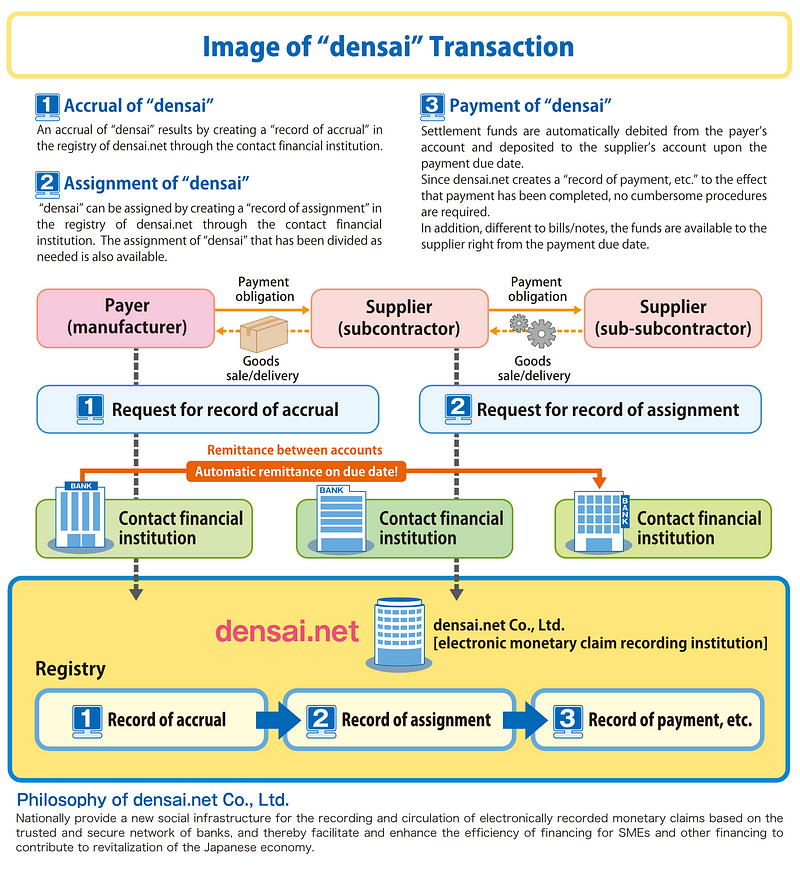

For the first pillar of regional and industry-specific awareness and promotional activities, discussions are underway with the Japan Chamber of Commerce and Industry to add items on the digitization of checks and bills and promotion of electronically recorded monetary claims to the “Digital Support Menu” provided to businesses. Explanatory meetings for companies are also being held in collaboration with Densai.net.

Note of the editor: Densai

Densai (or Densai Net) is the “Zengin Electronic Credit Network”, which refers to electronically recorded claims that are intended to replace bills and nominative claims (accounts receivable, etc.).

For the second pillar of broader awareness and promotional activities, seminars on full digitization of checks and bills are being held from May to July in collaboration with Densai.net. According to survey results, about 75% of participants intend to use electronically recorded monetary claims.

For the third pillar of support for financial institutions, lectures and study sessions for financial institutions will be held, and a system will be established to regularly share best practices across different types of financial institutions.

Regarding the spread of electronically recorded monetary claims by prefecture, interviews were conducted with regional financial institutions in the three Hokuriku prefectures where usage is high. It was found that each bank is implementing multifaceted initiatives and carefully maintaining two-way communication with users.

Revision of the voluntary action plan

The secretariat explained the following regarding the revision of the voluntary action plan:

The Partnership Building Declaration was introduced in 2020 as one of the measures to promote fair transactions to prevent the negative impact of the prolonged COVID-19 pandemic. It is a declaration made by businesses, in the position of “orderer,” under the name of “a person with representative rights,” aiming to improve the added value of the entire supply chain and achieve coexistence and co-prosperity between large enterprises and SMEs.

In light of the revision of the Partnership Building Declaration and the government’s call for revision of the voluntary action plan, it is proposed to include in the voluntary action plan that financial institutions, as supporters of businesses, will comply with the promotion standards and implement the Partnership Building Declaration to show their commitment to improving payment conditions for businesses.

The revised version will include a note on shortening the term of bills and incorporate content related to the Partnership Building Declaration.

An opinion survey will be conducted until noon on July 2, and a written meeting of this study group will be held on July 4 to report the finalized revised version of the voluntary action plan. The revised version is scheduled to be published on the Japanese Bankers Association website on July 19.

Q&A and exchange of opinions

[Committee Member] (Read by the secretariat due to absence)

The change of bill terms to within 60 days for companies subject to the Subcontract Act is highly welcome. It is expected that this will trigger an increase in businesses transitioning from bills to electronically recorded monetary claims, as well as those moving to cash payment on due date. It would be appreciated if related ministries could monitor and promote such future movements.

[Committee Member]

This fiscal year (FY2024) is scheduled for an interim evaluation and is important for achieving full digitization of checks and bills by the end of FY2026. The necessary actions, such as promoting electronically recorded monetary claims and strengthening awareness and promotional activities, have become clear. The key points now are how to increase the number of actions and how to quickly cycle through the PDCA process.

Regarding the initiatives of financial institutions in the three Hokuriku prefectures, how is the information exchange and cooperation among financial institutions within the region?

(Secretariat Response)

While there was no mention of close information exchange among financial institutions in the three Hokuriku prefectures regarding digitization efforts, each financial institution seems to be aware that others in the region are advancing digitization.

During interviews with financial institutions in the three Hokuriku prefectures, examples were found where even non-digitization staff members recognize the need for digitization when bills are brought to the counter, indicating a high sensitivity to digitization.

[Committee Member]

With only three years left until the end of FY2026, we recognize that while checks and bills have significantly decreased, the rate of decrease is slowing down. Our bank also needs to tighten its efforts.

Regarding increasing the number of actions mentioned earlier, our bank has completed the first round of notifications to all customers, including those with relatively high usage of checks and bills who have account managers, as well as those with low usage through direct mail and call center notifications. However, we feel it’s important to continue steadily increasing opportunities for low-usage customers to see and hear about digitization, and we want to focus on further information dissemination in the future. We are also creating a list of service menus and roadmaps to help customers smoothly shift to digital, and we want to use these roadmaps to engage in digitization activities while cycling through the PDCA process.

[Committee Member]

The proposal to newly include the Partnership Building Declaration and guidelines for price negotiations for appropriate labor cost transfer in the voluntary action plan feels timely.

Our federation is also calling on member companies to publish the Partnership Building Declaration and improve its effectiveness. We revised Article 2 of our Corporate Behavior Charter on May 31, adding the phrase “In particular, we will aim for the coexistence and co-prosperity of the entire supply chain based on the Partnership Building Declaration.”

Furthermore, in the “Implementation Handbook for the Corporate Behavior Charter,” which shows specific action plans, we have enhanced descriptions related to promoting fair transactions through appropriate price transfer, including guidelines for price negotiations for appropriate labor cost transfer. Regarding promissory notes, we continue to clearly state, “In payment of consideration, abolish the use of promissory notes and make payments as quickly as possible after receiving goods, etc. In subcontracting transactions, ensure payment within 60 days.” We want to strengthen cooperation to promote fair transactions.

While the financial industry has a relatively high declaration rate for the Partnership Building Declaration, according to our federation’s secretariat, the declaration rate among member banks of the Japanese Bankers Association was 68% as of May. We strongly urge member banks to also publish the declaration.

(Secretariat Response)

We recognize that by including the Partnership Building Declaration in the voluntary action plan in this revision, the initiative will be communicated to each financial institution, and we expect the declaration rate to increase in the future.

The Partnership Building Declaration template includes some descriptions about the use of bills, so by having various industries make the declaration, it is expected that the trend towards abolition and digitization of checks and bills will further progress. Our association also wants to continue cooperating and responding to such initiatives.

[Committee Member]

Regarding the digitization of checks and bills, I feel there is a temperature difference in the approach and awareness of individual banks across the regional banking sector as a whole.

The explanation mentioned cooperation with the Japan Chamber of Commerce and Industry to hold seminars for companies, and I believe such business-oriented initiatives are very important. Our bank is also collaborating with core companies in the prefecture that are already using electronically recorded monetary claims, interviewing them about how much they have reduced costs and how much time they have saved on bill issuance procedures, and creating dialogue sheets based on this to show to customers. In addition, we simulate how much customers can reduce costs and create materials that visually show the results for proposal. I believe it’s very important to visualize the benefits of digitization from a business perspective and make proposals.

Although we regularly share case studies of digitization efforts within the regional banking sector, I feel that some parts are not fully permeating, which is a point for reflection. Regarding the overall reduction rate, while other sectors have achieved their targets, the regional banking sector remains at just under 80%. This is partly due to having 62 member banks, but we want to work together as a unified whole.

The Regional Banks Association of Japan, of which our bank is a member, is also changing the names of meetings from “seminars” and “study sessions” to “promotion meetings” to reform consciousness, and we want to respond to the reduction of checks and bills as a whole membership.

[Committee Member]

While the situation differs in each prefecture, in urban areas, there are multiple financial institutions such as megabanks, regional banks, credit unions, and credit cooperatives. Due to differences in temperature towards check and bill digitization among financial institutions, the penetration of awareness from a customer perspective is not progressing in reality.

Although our bank has achieved corresponding results by implementing measures in stages, we recognize that continuing to penetrate awareness among customers will be an ongoing challenge. The dialogue sheets mentioned by the previous committee member were very informative. While our bank is also approaching customers who issue many checks and bills individually, we consider ourselves halfway there, so we want to promote this while gathering various information through this study group.

Please follow us to read more about Finance & FinTech in Japan, like hundreds of readers do every day. We invite you to also register for our short weekly digest, the “Japan FinTech Observer”, on Medium or on LinkedIn. Our global Finance & FinTech Podcast, “eXponential Finance” is also available through its own LinkedIn newsletter, or via our Podcast Page.

Should you live in Tokyo, or just pass through, please also join our meetup. In any case, our YouTube channel and LinkedIn page are there for you as well.