Prudential Life Japan Net Income Halves Amid Employee Fraud Scandal and Sales Suspension

Prudential Life Insurance (Japan) concluded its fiscal year ending March 31, 2026, under the shadow of a self-inflicted operational crisis that has severely eroded its bottom line. While the insurer’s massive foundation of existing policies provided a veneer of "steady growth," the fiscal year was defined by a precipitous decline in profitability and a near-total collapse of its new business engine. This contraction is the direct result of internal misconduct involving the mishandling of funds by sales employees, which triggered a voluntary—and costly—suspension of all new sales activities starting February 9, 2026. Management’s attempt to frame the results as "sufficient" cannot mask the strategic tension between preserving its 45.74 trillion yen book of business and navigating the reputational wreckage of an internal integrity breach.

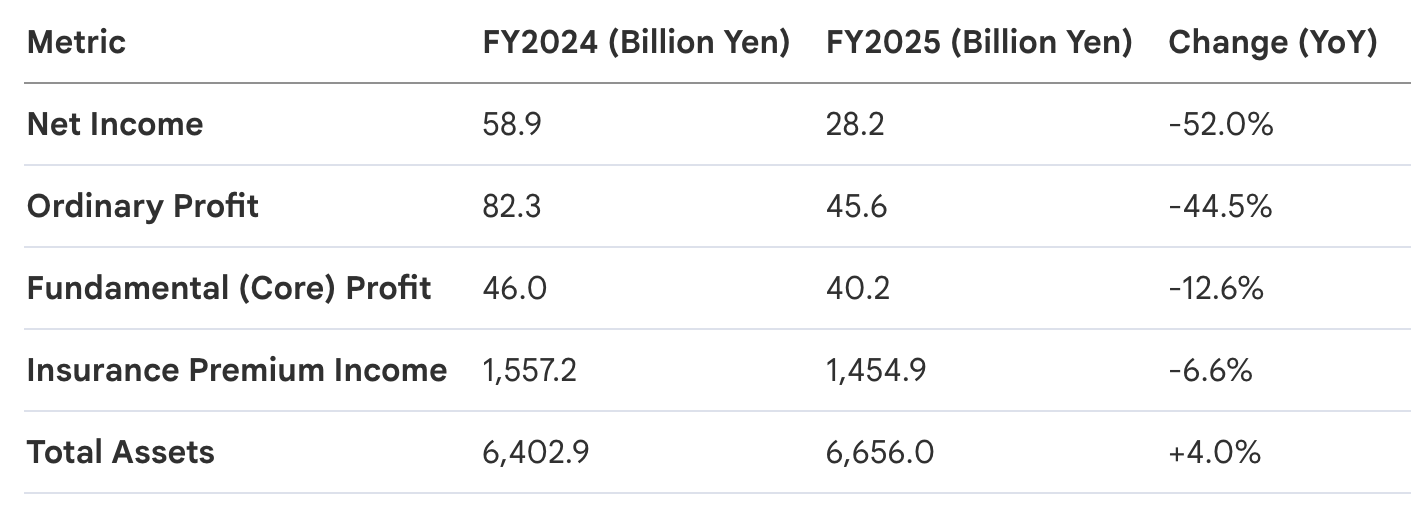

The headline figures for FY2025 reveal a business in retreat. While external market conditions provided significant tailwinds, the company’s internal failures resulted in net income and ordinary profit falling by nearly half year-over-year.

This erosion of profitability was compounded by a heavy extraordinary loss specifically provisioned to handle the financial aftermath of employee-led fraud.

1. The Fraud Scandal: Cost of Misconduct and Compensation Framework

For a firm whose brand is predicated on the strategic pillar of trust, the discovery of "inappropriate acts involving money" by both current and former sales staff has necessitated a drastic overhaul of its operational model. The decision to halt all new sales activities in early February was a move of necessity rather than choice, intended to provide the administrative space required for a total compliance audit. However, the price of this pause is reflected in the hard data of the company’s "special losses."

Prudential Life Japan recorded a specific extraordinary loss of 4,748 million yen in FY2025 dedicated to customer compensation. To manage the remediation, the firm has established a "Customer Compensation Committee" with a mandate that is as much about regulatory appeasement as it is about customer service. Key components include:

- Independence: The committee is composed entirely of third-party experts to ensure an unbiased adjudication of claims, a move essential for restoring credibility with the Financial Services Agency (FSA).

- Purpose: It is tasked with a granular review of individual customer reports to judge the necessity and precise amount of payouts.

- Provisional Nature: The 4,748 million yen figure is a "best estimate" based on current internal investigations; management admits this figure remains subject to upward revision as more misconduct potentially comes to light.

While these direct compensation costs are substantial, they are merely the entry fee for the company’s survival. The broader damage is seen in the destruction of the new business pipeline, which has effectively been frozen at the request of regulators.

2. Operational Fallout: Sales Suspension and Market Performance

The internal crisis effectively neutralized Prudential’s primary growth engine during the critical fourth quarter, transforming a potential year of expansion into a period of market-facing contraction. Perhaps most damning is the fact that this internal chaos caused the company to waste a historic bull market. While the Nikkei 225 hit an all-time high of 59,000 and 10-year JGB yields ended at 2.345%—lifting the firm’s asset management income to 296.1 billion yen—these external gains were cannibalized by the costs of the sales halt and an increase in policy cancellations (解約の増加) as news of the scandal broke.

The damage to the new business pipeline is stark and precise:

- New Business Volume: Fell 22.9% to 3.507 trillion yen.

- New Annualized Premiums: Dropped 13.0% to 70.0 billion yen.

- New Business Policy Count: Collapsed by 23.8% to approximately 276,000 policies.

The only factor preventing a full-scale liquidity crisis is the "steady" performance of the existing portfolio. Existing policy volume rose 1.8% to 45.74 trillion yen, serving as a defensive moat. However, this dichotomy is unsustainable. With Insurance Premium Income falling 6.6% to 1.45 trillion yen, the company is now entirely reliant on its legacy book to fund the rising costs of internal reform and system upgrades.

3. Remediation and Structural Reform: Investing in Recurrence Prevention

The 12.6% drop in "Fundamental Profit" (Core Profit) to 40.2 billion yen is the clearest indicator of the crisis’s impact on the company’s underlying health. Stripped of accounting noise, this metric shows a business burdened by the administrative weight of its own misconduct. Management has characterized this as a strategic prioritization of "system reinforcement" and "prevention of recurrence," as business expenses surged to fund a total rebuild of internal compliance and monitoring infrastructure.

To reconcile the more dramatic 52.0% collapse in Net Income, one must account for a high-water mark in the prior year. FY2024 results were artificially inflated by a 29 billion yen post-tax gain from reinsurance transactions intended to bolster financial stability. Without that one-time windfall, and with the new 4,748 million yen fraud provision, the current bottom line reflects the "new normal" for a firm under intense regulatory scrutiny.

In summary, while Prudential Life Japan’s 6.65 trillion yen in total assets provides a sufficient capital cushion for now, the long-term outlook remains precarious. The path to recovery is not merely financial; it depends entirely on the "Customer Compensation Committee" successfully purging the legacy of fraud and convincing the FSA that the firm is fit to resume its sales activities. Until then, the company remains a giant on the defensive, spending its core profits to fix a broken internal culture.