Resona Bank Launches FlexPay Multi-Bank Corporate Payment Platform

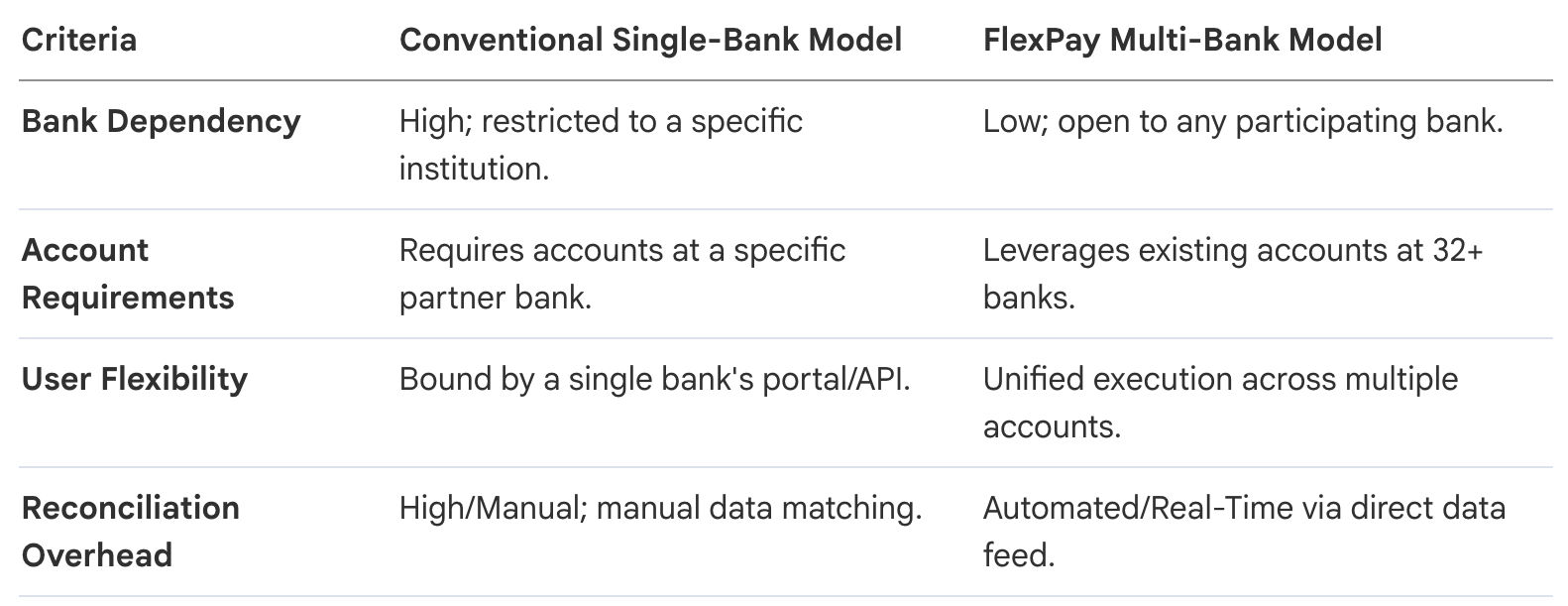

Resona Bank has announced the launch of FlexPay, a pioneering corporate payment platform designed to streamline accounting workflows for small and medium-sized enterprises. This service marks the first multi-bank payment scheme in Japan, integrating with 32 regional and major banks to allow companies to use their existing accounts for automated transactions.

By connecting cloud accounting software directly with banking functions, the system eliminates the need for manual data entry during invoice processing and reconciliation. The initiative aims to address labor shortages and low productivity by creating a seamless digital link between financial records and actual fund transfers.

Ultimately, FlexPay serves as an open infrastructure that simplifies complex fiscal management through strategic partnerships with major cloud service providers.

1. Executive Context: The Crisis of Fragmented Corporate Finance

The Japanese corporate landscape, particularly for Small and Medium-sized Enterprises (SMEs), is navigating an acute operational crisis. This is driven by the intersection of a severe, structural labor shortage and the technical friction characterizing the "last mile" of payment execution. While many firms have adopted cloud accounting for internal record-keeping, the actual movement of capital remains tethered to legacy banking interfaces. Solving this disconnect is a strategic necessity for national productivity; until banking settlement is natively embedded into the accounting workflow, digital transformation (DX) remains an unfinished project. One must view the automation of these workflows as a "Digital Labor" solution—deploying software to reclaim the massive human capital currently lost to manual treasury administration.

The Core Inefficiencies of Traditional Workflows

Synthesizing the current state of SME finance reveals three primary friction points where productivity is lost:

- Manual Invoice Entry: Personnel must manually transcribe data from invoices into accounting systems, a high-latency process prone to human error.

- Disconnected Banking Execution: Payment completion requires users to exit the accounting environment and log in to separate, proprietary internet banking portals to manually trigger transfers.

- Manual Reconciliation (Keshikomi): Post-payment, treasury teams must manually match deposit/withdrawal records against ledger entries to ensure accuracy—a redundant task that provides no strategic value.

Historically, DX has stalled at the banking interface due to a fundamental fragmentation between agile cloud software and closed financial silos. Banking services have operated as proprietary products rather than interoperable utilities, requiring manual CSV exports or bespoke API connections that are often cost-prohibitive for SMEs. This fragmentation creates "data silos" that necessitate manual intervention, effectively capping the scalability of corporate finance operations. FlexPay emerges as a structural intervention to provide the missing interoperability layer between the accounting cloud and the banking core.

2. Architectural Paradigm Shift: From Single-Bank to Multi-Bank Schemes

The launch of FlexPay signals a transition from "Single-Bank" models toward a "Multi-Bank" type scheme, a shift that aligns with the global trend of Banking-as-a-Service (BaaS) logic. In a conventional model, a business is often locked into a specific institution to access digital efficiencies. The Multi-Bank paradigm democratizes financial access, allowing an enterprise to utilize its existing, diverse banking relationships through a single interface, thereby reducing institutional lock-in and enhancing treasury flexibility.

The scale of the FlexPay network represents a significant "network effect" in domestic infrastructure. With 32 participating banks, the scheme provides unprecedented geographical and institutional breadth:

- National & Group Leaders: Resona Bank, Saitama Resona Bank, Kansai Mirai Bank.

- Hokkaido/Tohoku Cluster: North Pacific Bank (Hokuyo), 77 Bank, Toho Bank.

- Kanto/Tokai/Chubu Cluster: Joyo Bank, Gunma Bank, Keiyo Bank, Hachijuni Nagano Bank, 16 Bank, Ogaki Kyoritsu Bank, Hyakugo Bank.

- Kansai/Chugoku/Shikoku Cluster: Kyoto Bank, Shiga Bank, Nanto Bank, Minato Bank, San-in Godo Bank, Awa Bank, Shikoku Bank, Momiji Bank, Yamaguchi Bank.

- Kyushu/Okinawa Cluster: Fukuoka Bank, 18 Shinwa Bank, Nishi-Nippon City Bank, Kitakyushu Bank, Kumamoto Bank, Ryukyu Bank.

Additionally, Yokohama Bank, Ikeda Senshu Bank, and Chugoku Bank are currently scheduled to participate, further extending the platform’s reach. This broad participation ensures that FlexPay functions not as a proprietary silo, but as a shared, national utility.

3. Functional Deep-Dive: The Integrated Workflow (Ikkan-Tsukan)

The strategic value of FlexPay is realized through "ikkan-tsukan"—an end-to-end, seamless integration that eliminates manual silos. By collapsing the distance between accounting systems and settlement functions, FlexPay creates a multiplier effect: the reduction in time-to-settlement allows corporate capital to be redeployed faster, while the removal of manual tasks frees labor for higher-value activities.

The FlexPay Integrated Workflow

- Invoice Verification: The process initiates within the accounting cloud where invoices are digitized and verified against records.

- Seamless Payment Execution: Payment instructions are transmitted directly to the linked bank accounts via FlexPay’s API interoperability layer, bypassing separate banking portals.

- Automated Reconciliation: The system confirms the transaction in real-time, automatically matching it to the invoice and generating the journal entry.

This "Open Infrastructure" is powered by strategic front-end partnerships. FlexPay has launched in coordination with RAKUS (via their "Rakuraku Denshi Hozon" platform) and freee. These cloud providers serve as the primary interface for users, hiding the underlying technical complexity of the banking settlement behind a streamlined, business-oriented front-end. This partnership model is the cornerstone of the transition from banking as a product to banking as an embedded service.

4. Strategic Assets: Patent-Driven Innovation and Open Infrastructure

Resona Bank’s platform represents a pivot toward "Embedded Finance," where banking services act as a utility layer supporting diverse business partners. This move transforms the bank’s role from a simple deposit holder to an infrastructure provider.

The Patent as a Strategic Moat

The significance of Patent No. 7618082 is foundational. This patent protects the specific domestic multi-bank corporate settlement scheme, serving as a defensive moat that prevents competitors—including traditional megabanks—from easily replicating the 32-bank scale and connectivity method. It establishes a standardized framework for financial interoperability, ensuring that this Multi-Bank approach becomes the "de facto" standard for domestic corporate payments.

Infrastructure for "New Challenges"

The ultimate mission of FlexPay is the enhancement of SME resilience. By automating the administrative "back-office" burden, the infrastructure empowers firms to pivot their human resources toward "new challenges," such as innovation and strategic growth. In an era of labor scarcity, the ability to automate mundane treasury tasks is a competitive advantage that directly impacts a firm’s capacity to survive and thrive in a digital economy.

5. Summary of Strategic Implications

FlexPay represents a permanent shift in the Japanese corporate payment landscape, creating a bridge between the cloud software industry and the financial sector that is built for long-term interoperability.

Key Strategic Takeaways

- Infrastructure Openness: The platform moves away from bank-specific dependency, allowing firms to maintain legacy relationships while accessing modern fintech efficiencies.

- Operational Excellence: The "one-stop" system significantly reduces risk management overhead by minimizing human error and providing real-time reconciliation.

- Future Scalability: With 32 founding banks and a roadmap for expanding both banking participants and cloud partners, the infrastructure is positioned for nationwide dominance.

FlexPay is the new blueprint for domestic financial infrastructure. It redefines the relationship between banking and accounting, transforming settlement from a disconnected administrative task into a natively integrated component of the digital enterprise.