Resona Holdings' FY2025 Results and the FY2028 Path to Value Creation

The FY2025 results serve as the demonstrable proof-of-concept for the Resona Group’s interest-rate sensitivity and its pivot from historical capital recovery to an aggressive value-creation phase. Having moved past the "DNA of reform" and the full repayment of public funds, the Group is now uniquely positioned to capitalize on a normalizing rate environment. The current performance confirms that the Medium-Term Management Plan is an active engine driving the transition from qualitative enhancement to the strategic utilization of capital.

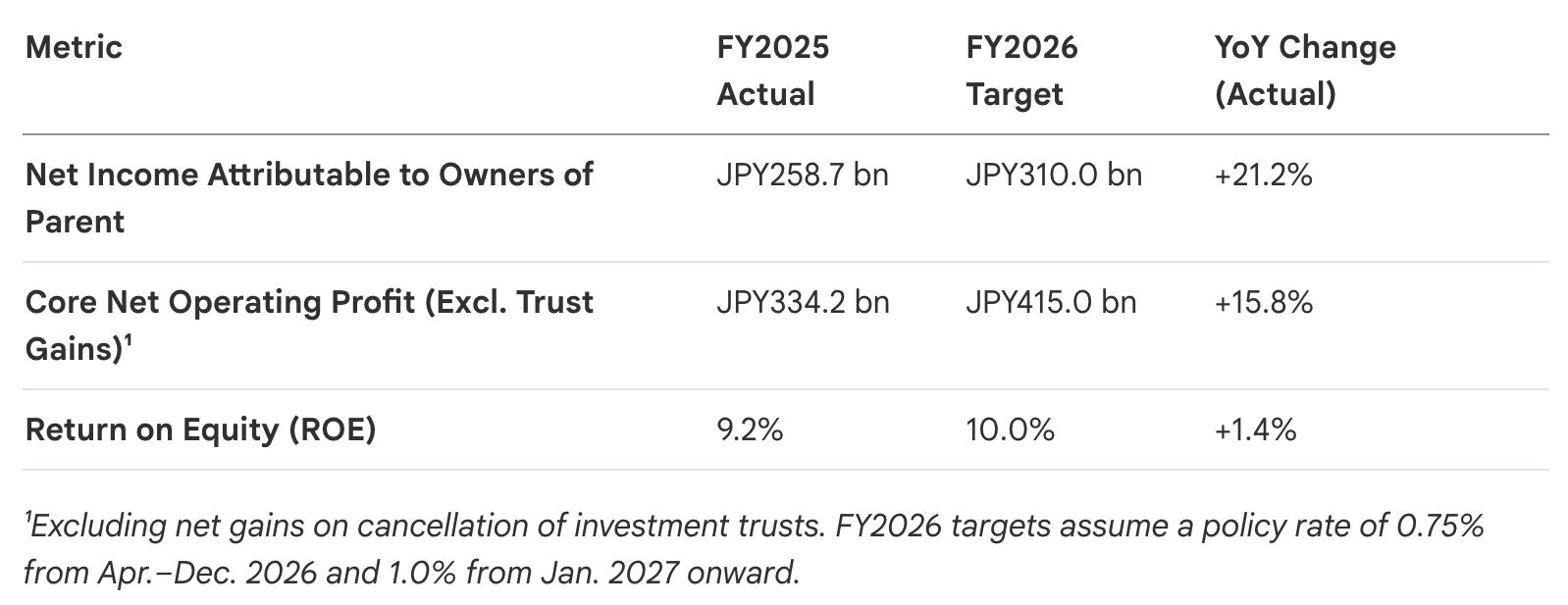

FY2025 Net Income reached JPY258.7 billion, a 21.2% year-on-year increase that comfortably outpaced initial guidance. The FY2026 target of JPY310.0 billion represents a continued acceleration of this momentum, predicated on the bank’s inherent leverage to rising yen interest rates. This bottom-line expansion is fundamentally fueled by a structural shift in core earning power, specifically the widening of interest margins within the dominant retail franchise.

1. Net Interest Income (NII) and Domestic Loan Performance

The shifting interest rate environment has fundamentally revitalized the bank’s traditional lending model, transforming the balance sheet into a primary driver of ROA improvement. The strategy focuses on maximizing the spread between a low-cost, retail-heavy funding base and a rate-sensitive loan portfolio.

- Precise Attribution Analysis: NII growth was driven by a sophisticated mix of volume and rate factors. The JPY57.8 billion increase in NII from domestic loans and deposits is attributed to a +JPY21.5 billion volume factor and a +JPY36.2 billion rate factor, demonstrating that repricing is now the primary catalyst for revenue expansion.

- Lending Momentum: Average loan balances grew by 4.76% in FY2025, while loan rates saw a 27bps increase.

- Residential Housing Dominance: New origination reached JPY1.53 trillion (+19.8% YoY). Critically, 96% of these are variable-rate products, ensuring margin expansion as policy rates rise.

- "Retail No. 1" Funding Moat: The funding base is anchored by a 61.8% personal deposit ratio and 10.37 million Banking App downloads. This high digital engagement and personal touch create immense "stickiness" and higher switching costs, allowing Resona to expand a JPY63.7 trillion deposit base without incurring the excessive procurement costs that plague competitors.

This "sticky" funding base provides the necessary liquidity to diversify income streams into non-interest sectors without sacrificing the tailwinds of the current rate cycle.

2. Fee Income Evolution and Business Solutions

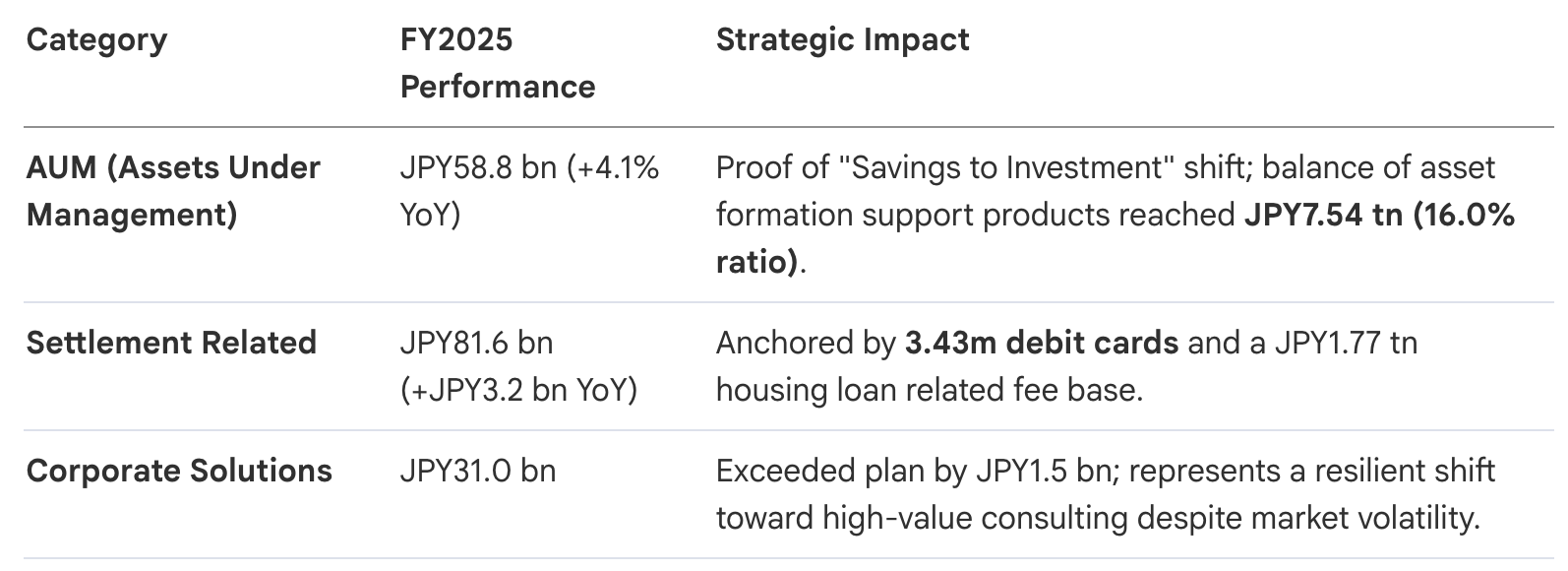

Fee income remains the bedrock of Resona's revenue stability, achieving record-high profits for five consecutive years. Resona is actively shifting its fee composition from transactional services to a "Solution Group" model that emphasizes long-term asset growth and corporate consulting.

Beyond current segments, Resona is institutionalizing next-generation growth through the JR West alliance and the "BaaS and Payment Model." These initiatives leverage Resona's status as Japan’s largest retail bank to create regional value circulation. However, this revenue growth is only one half of the valuation equation; the other is the radical efficiency of Resona's management platform.

3. Structural Reform: Overhead Ratio (OHR) and Cost Management

Reducing the OHR is the non-negotiable cornerstone of Resona's "Structural Reforms of Management Platforms." Resona is aggressively optimizing the P&L to ensure that every yen saved in legacy operations is redirected toward Digital Transformation (DX) and human capital.

- Efficiency Trajectory:

- FY2024 Actual: 64.2%

- FY2025 Actual: 57.5% (Significantly ahead of the 59% target)

- FY2026 Target: ~55%

- FY2028 MMP Target: Range of 40%

In FY2025, Resona lowered the OHR by 6.6% YoY. This was achieved despite a JPY21.6 billion increase in operating expenses. A sophisticated breakdown shows Resona is cutting deep into non-strategic costs - personnel expenses (-8.5 bn) and non-personnel expenses (-10.9 bn) - to fund the P&L impact of growth initiatives, such as the JPY45.0 billion Digital Garage (DG) goodwill amortization. This disciplined management ensures the P&L is leaner and focused exclusively on high-return assets.

4. Capital Strategy and Shareholder Returns

The financial flexibility harvested through OHR reduction and cost discipline is the primary catalyst for Resona's aggressive new shareholder return framework. Resona has transitioned from "capital enhancement" to "capital circulation," focusing on improving capital efficiency to maximize total shareholder return.

Shareholder Return Framework (Announced May 2026):

- Total Shareholder Return Ratio: Established a clear floor of 50% or higher.

- Dividends: FY2026 forecast of 37 yen (+8 yen YoY).

- Share Buybacks: Up to JPY35.0 billion announced for the current period.

- DOE Target (FY2029): Upwardly revised from 3% to 3.5%.

Strategic Capital Creation: Resona's commitment to reducing policy-oriented stock holdings (targeting a 2/3 reduction in book value by 2030) is a critical engine for value. In FY2025 alone, the gain on sale reached JPY106.5 billion. This divestment strategy is projected to create capital equivalent to JPY300.0 billion (representing 1.5% of the CET1 ratio). This provides the "dry powder" necessary for both inorganic growth and accelerated returns.

5. Strategic Outlook: The Path to FY2028

The "Shift to the Next Stage" vision represents the first 1,000 days of Resona's Corporate Transformation (CX). By evolving into a "Solution Group" with an impregnable retail base, Resona is positioning itself for a quantum leap in profitability as macroeconomic conditions normalize.

MMP Targets & Sensitivity Analysis (FY2028):

- Net Income: JPY390.0 billion.

- ROE Sensitivity: Resona anticipates a range of 12% ROE (at a 1.0% policy rate) to 14% ROE (at a 1.5% policy rate).

Sensitivity Spotlight: Resona's earnings model shows a highly predictable tailwind: every significant hike in the policy rate provides a massive uplift to the bottom line. Based on provisional calculations, Resona expects an increase in Gross Operating Profit of approximately +JPY230.0 billion once the impact of a 1.5% policy rate hike is fully materialized.

Resona Holdings is no longer a bank in recovery; it is a high-efficiency growth engine leveraging its unique balance sheet, "Retail No.1" funding moat, and disciplined capital circulation to realize sustainable, industry-leading value creation.