SBI Sumishin Net Bank delivers solid FY2024 results, disappoints on FY2025 forecast

SBI Sumishin Net Bank (SSNB) has delivered a strong financial performance for the Fiscal Year 2024, concluded on March 31, 2025. The results are characterized by robust growth in both income and profitability, although slightly missing targets on ordinary profit (95% of forecast), mortgage loan origination (97%), and number of accounts (92%).

Key financial achievements for FY2024 include an Ordinary Income of ¥146.5 billion and a Profit Attributable to Owners of Parent of ¥28.1 billion, translating to a Basic Earnings Per Share (EPS) of ¥186.54.

However, the FY2025 forecast came in substantially below expectations, in particular as the Bank of Japan policy rate increases of July 2024 and January 2025 will be reflected in an expanded net interest margin only with some delay, i.e. even if the Bank of Japan stays pat, as many analysts expect now, there should be a significant increase in profitability based on the interest sensitivity of results that bank management had communicated during prior quarters.

FY2024 Financial Performance Overview

SBI Sumishin Net Bank reported a commendable financial performance for the fiscal year ended March 31, 2025, demonstrating significant growth across its primary financial metrics compared to the previous fiscal year.

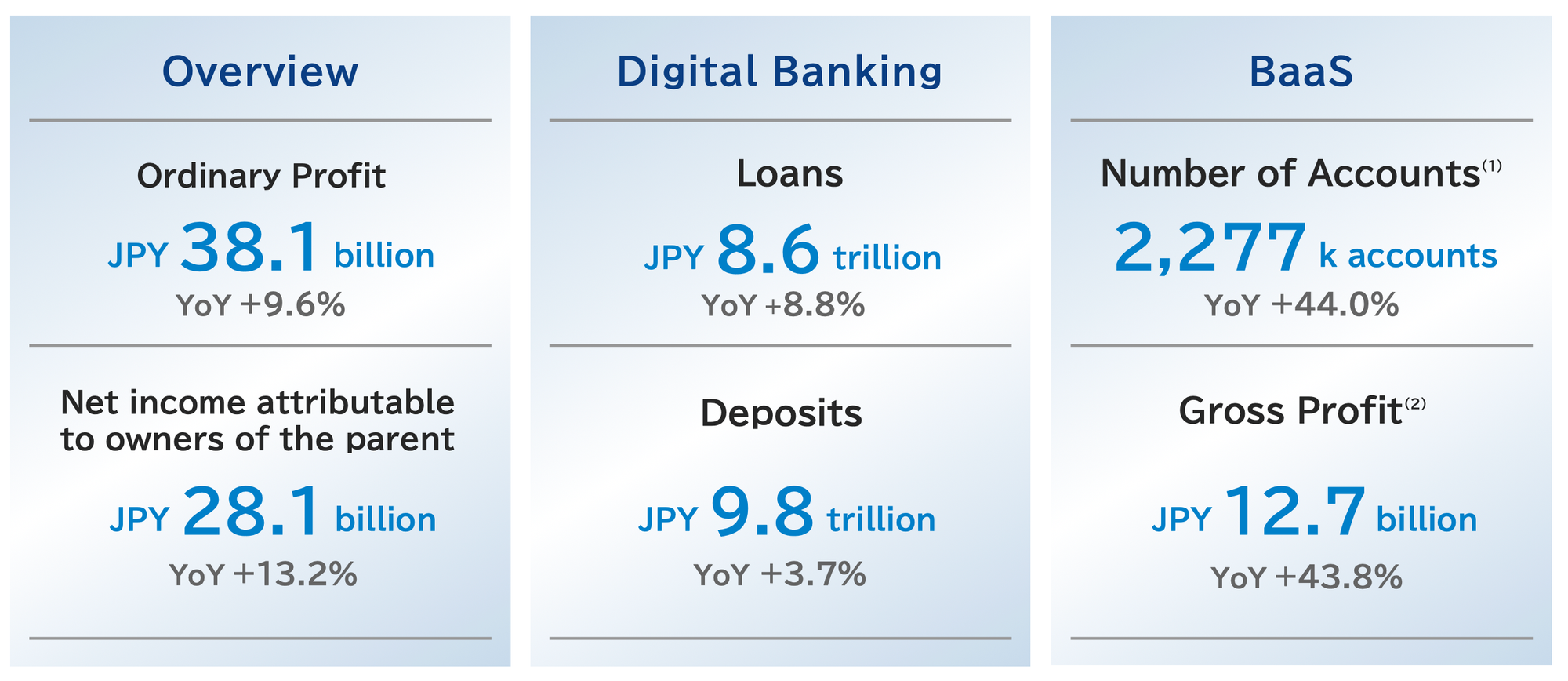

- Ordinary Income (equivalent to revenue for a non-financial company, encompassing interest income, fee income, and other operating income) reached ¥146,521 million for FY2025. This marks a substantial increase of 23.6% from ¥118,572 million recorded in FY2024.

- Ordinary Profit (representing profit before extraordinary items and income taxes) grew to ¥38,189 million, up 9.6% YoY from ¥34,846 million in FY2024.

- Profit Attributable to Owners of Parent (Net Profit) saw a robust increase of 13.2% YoY, rising to ¥28,127 million from ¥24,845 million in the prior fiscal year.

The comparison between the nine-month growth rates and the full-year growth rates suggests an acceleration in performance during the fourth quarter. For instance, Ordinary Profit grew by 6.5% in the first nine months, but the full-year growth was 9.6%. This implies that Q4 FY2024 Ordinary Profit (¥11,464 million) grew approximately 17.6% compared to Q4 FY2023 (¥9,749 million), indicating a strong finish to the fiscal year, likely driven by the effects of the Bank of Japan July 2024 policy rate increase making themselves felt.

Segment Performance Review

SBI Sumishin Net Bank's operations are structured across distinct business segments, each contributing differently to the overall performance in FY2024.

| Segment | Gross Profit (¥bn) | YoY Change (%) | Expenses (¥bn) | Ordinary Profit (¥bn) | YoY Change (%) |

| Digital Bank | 70.6 | +7.9% | 36.9 | 33.7 | +7.9% |

| BaaS | 12.7 | +43.8% | 7.9 | 4.7 | +30.1% |

| THEMIX | N/A | N/A | N/A | (0.2) | N/A |

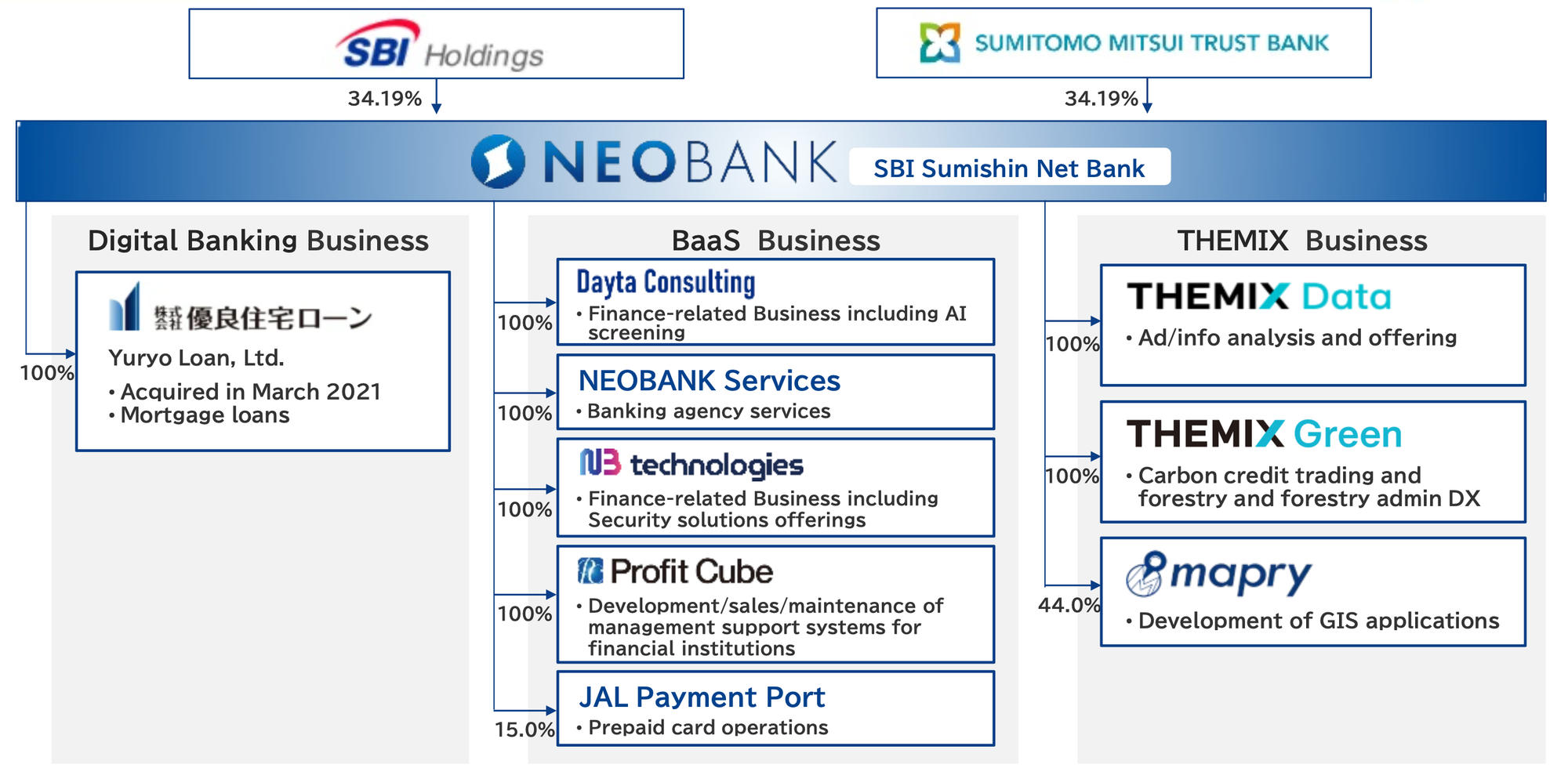

Digital Bank Business

- Gross Profit: ¥70.6 billion (a 7.9% increase YoY).

- Expenses: ¥36.9 billion (a 7.8% increase YoY), attributed to higher personnel costs, advertising and promotion, and outsourcing related to operations.

- Ordinary Profit: ¥33.7 billion (a 7.9% increase YoY). The growth in this segment was driven by higher commission income, particularly from housing loan origination and settlement-related fees spurred by the increasing adoption of cashless payments. Rising domestic and international interest rates also boosted interest income. The parallel growth in gross profit and ordinary profit suggests a relatively stable margin profile for this mature segment.

BaaS (Banking as a Service) Business

- Gross Profit: ¥12.7 billion (a significant 43.8% increase YoY).

- Expenses: ¥7.9 billion (a substantial 53.4% increase YoY), reflecting ongoing system investments and promotional activities for the "NEOBANK®" service.

- Ordinary Profit: ¥4.7 billion (a strong 30.1% increase YoY). Key drivers for the BaaS segment's expansion included higher account fees from an increasing number of accounts both within SSNB itself and through its NEOBANK® partners, alongside increased fees from the origination of housing loans and asset formation loans via this platform. While the BaaS segment is a clear growth engine, its expense growth (53.4%) outpaced its gross profit growth (43.8%). This pattern is common for rapidly scaling technology-driven services that are investing heavily in platform development and customer acquisition. The focus will be on achieving operating leverage in the future, where revenue and gross profit growth eventually outstrip expense growth, leading to margin expansion.

THEMIX Business

- Ordinary Loss: ¥200 million. Management indicates this is due to the segment being in a startup phase, where expenses are incurred ahead of significant revenue generation. This represents a longer-term strategic investment.

Shareholder Returns and Capital Management

SBI Sumishin Net Bank has demonstrated a commitment to enhancing shareholder returns, as evidenced by its dividend policy and declarations for FY2024, alongside positive indications for the upcoming fiscal year.

| Fiscal Year | Dividend Per Share (¥) | YoY Absolute Change (¥) | YoY % Change |

| FY2024 (Actual) | 16.50 | - | - |

| FY2025 (Actual) | 19.00 | +2.50 | +15.2% |

| FY2026 (Forecast) | 22.50 | +3.50 | +18.4% |

Dividend Policy and Declaration (FY2024)

- For the fiscal year ended March 31, 2025, SSNB declared an actual dividend of ¥19 per share.

- This represents a ¥2.50 increase from the ¥16.50 per share dividend paid for FY2023. The company issued a "Notice regarding Dividends of Surplus (Dividend Increase)" to formalize this.

Projected Dividend for FY2025

- Looking ahead, the bank has forecasted an annual dividend of ¥22.50 per share for FY2025 (ending March 31, 2026).

- This projection indicates a further planned increase of ¥3.50 per share compared to the FY2025 actual dividend, signaling management's confidence in sustained profitability.

Management Discussion and Business Overview

Management's commentary accompanying the FY2024 results highlighted key operational achievements and strategic directions that underpin the reported financial success.

Management's Commentary on Results

- Strong Loan Growth: Continued demand for loans, particularly the bank's core housing loan products, led to higher interest income.

- Favorable Interest Rate Environment: Increased interest income was also derived from securities investments, benefiting from the rise in both domestic and international market interest rates.

- Gain on Subsidiary Sale: The net profit for FY2024 was positively impacted by a gain realized from the sale of shares in a subsidiary, NetMove Co., Ltd., which was excluded from the scope of consolidation during the fiscal year. This divestiture might suggest a strategic sharpening of focus on core digital and BaaS banking activities, allowing the bank to reallocate capital and management attention to its primary growth engines.

Key Operational Achievements

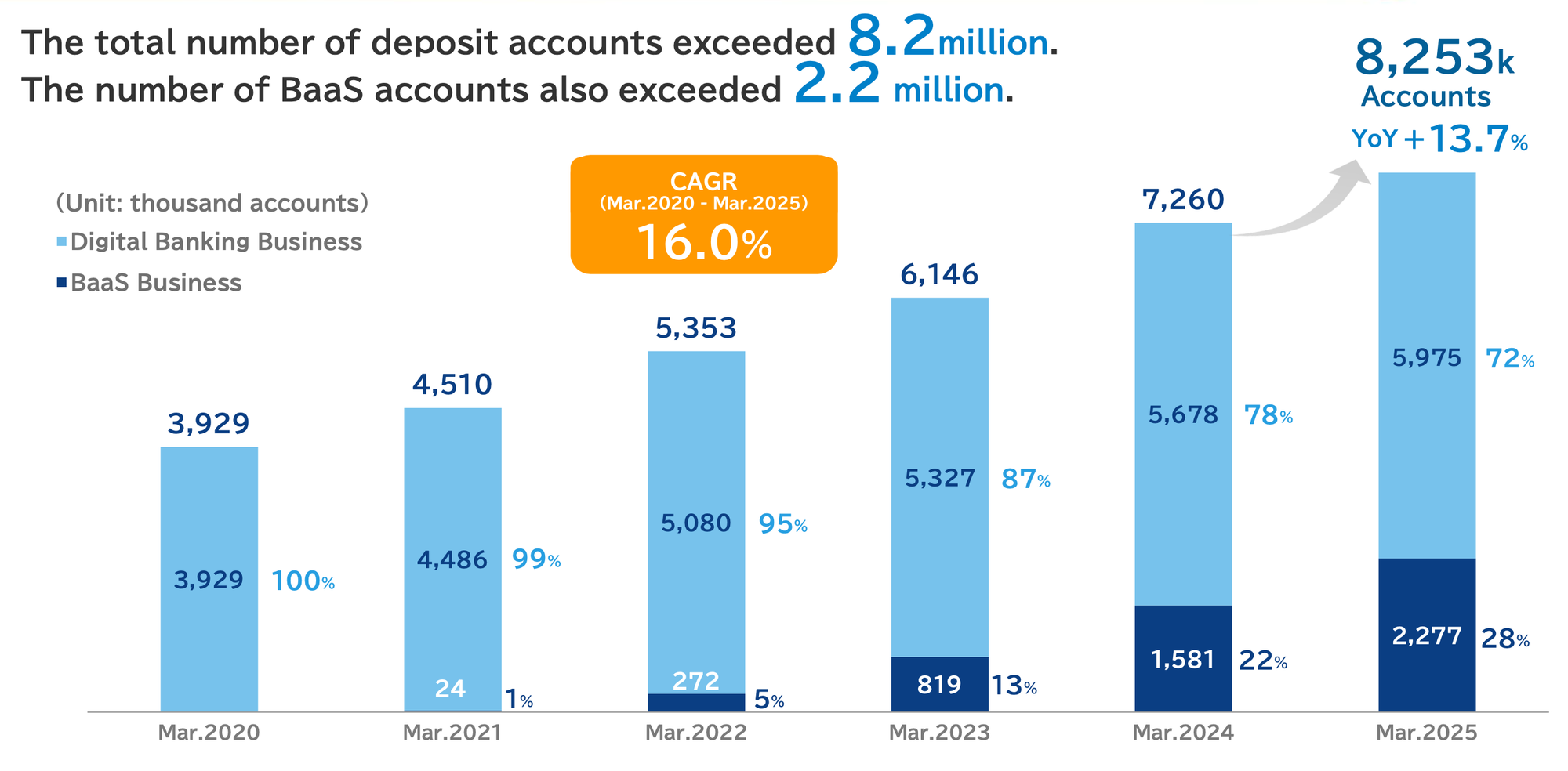

- Customer Base Expansion: SSNB continued its impressive track record of customer acquisition. A press release in January 2025 announced that the number of deposit accounts had surpassed 8 million, reflecting ongoing accumulation throughout FY2024. This growing customer base is fundamental to scaling its operations and fee-generating potential.

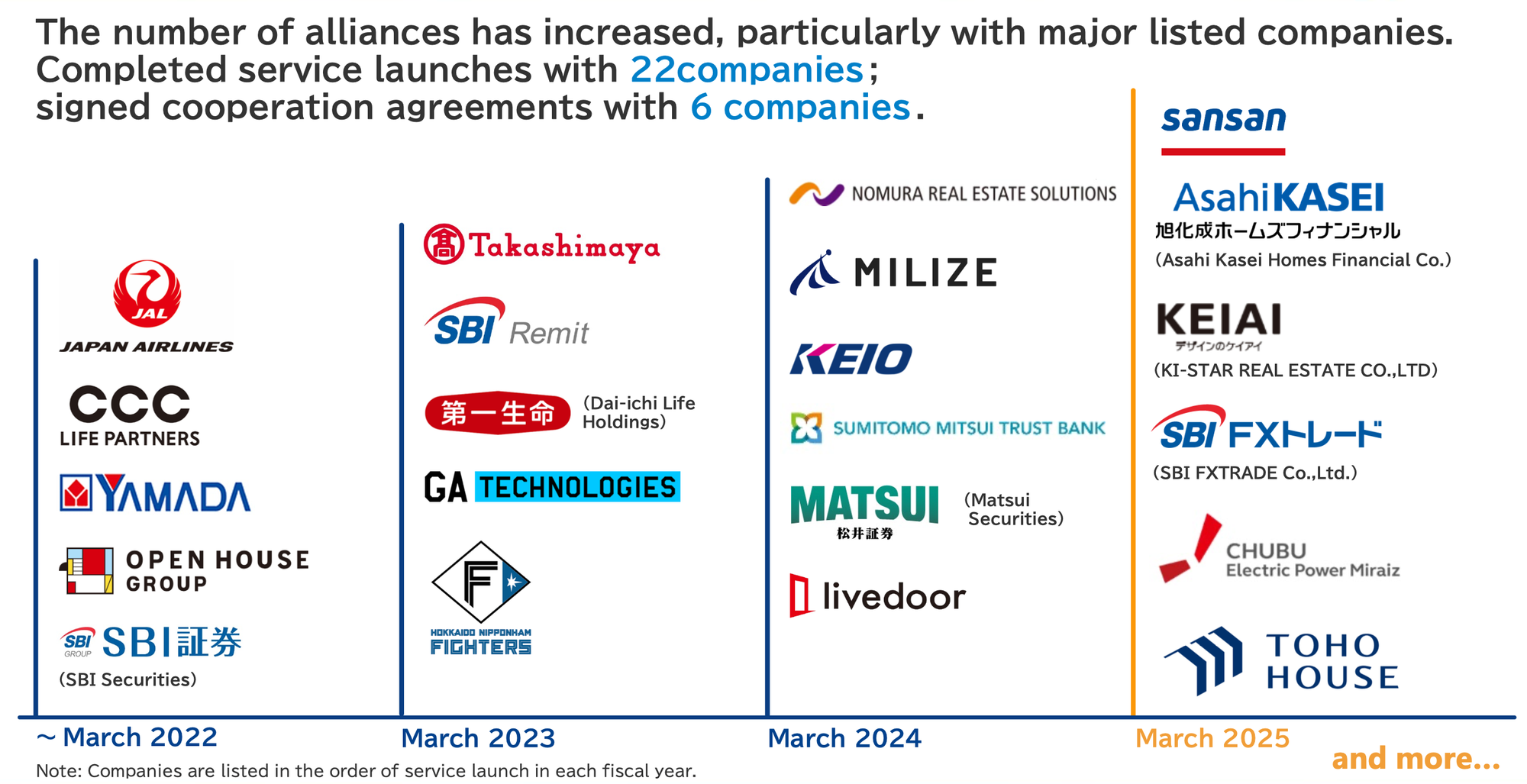

- NEOBANK® Service Traction: The BaaS platform, NEOBANK®, has shown significant progress, with deposit accounts acquired through this service exceeding 2 million. Notably, management highlighted that approximately 70% of new accounts opened in the recent past were via NEOBANK® partnerships. This validates the BaaS strategy as a highly effective and potentially more efficient customer acquisition channel compared to traditional direct-to-consumer marketing, as it leverages the existing customer ecosystems of its partners.

Strategic Initiatives and Market Positioning

- SSNB emphasizes its customer-centric principle and the strategic leveraging of technology to enhance service delivery and convenience.

- The bank maintains a dual focus on strengthening its core Digital Bank business while aggressively expanding its BaaS (NEOBANK®) offerings.

- The THEMIX business is being nurtured as a future pillar of growth, despite currently being in an investment phase.

- The overarching vision is to be a "fintech that goes beyond banking services," indicating ambitions to innovate and broaden its role in the financial lives of its customers and partners.