South Korea's Wealth Fund Expands to Tokyo

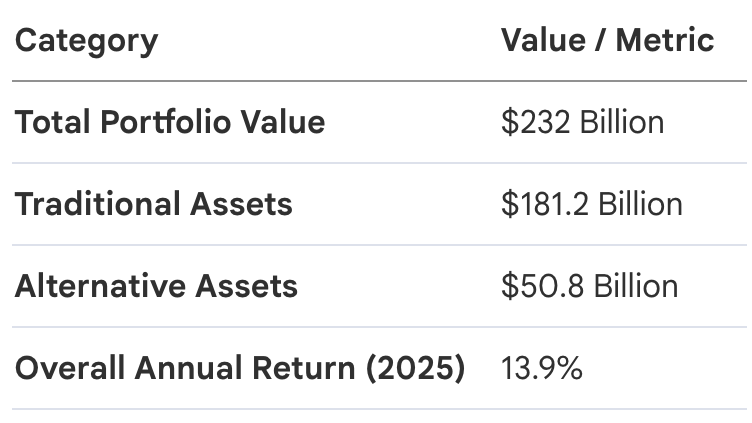

The Korea Investment Corporation (KIC) is set to establish a definitive boots-on-the-ground presence in Japan, taking a significant step in the $232 billion sovereign wealth fund's regional strategy. Led by President Park Il-young, the fund’s move to open a Tokyo branch in early July 2026 represents a sophisticated play to capture unrealized value within a Japanese market undergoing its most significant structural transformation in decades.

This sixth global outpost arrives at a moment of deepening financial integration across the Asia-Pacific. By transitioning from a remote allocator to a local participant, KIC aims to institutionalize its access to "unique investment opportunities" catalyzed by the Tokyo Stock Exchange’s (TSE) aggressive valuation mandates and a broader shift in the nation's capital recycling ecosystem.

The Governance Catalyst: Unlocking Value in the Nikkei

The strategic impetus for the Tokyo expansion was a primary focus of the 54th Public Investor Overseas Investment Council recently held at KIC’s headquarters in Seoul. During the council, industry leaders analyzed a Japanese macroeconomic environment where policy-driven governance reforms are finally meeting attractive valuation entry points.

Lee Hoon, KIC’s Chief Investment Officer, noted that Japan is currently entering a period of "structural expansion." This sentiment was echoed by Hirano Hiro, KKR’s Asia-Pacific Vice Chairman and CEO of Japan, who identified several core drivers currently fueling the market's evolution. According to the council’s findings, the primary structural growth catalysts include:

- Corporate Governance & Capital Efficiency: The TSE’s "Value-Up" initiatives are forcing a fundamental rethink of balance sheet management, particularly for the approximately 40% of Tokyo-listed companies still trading at a Price-to-Book Ratio (PBR) below 1.

- Conglomerate Rationalization: Large-scale Japanese conglomerates are increasingly divesting non-core business units to optimize operations, creating a robust pipeline for corporate carve-outs.

- The Rise of Public-to-Private (P2P) Deals: A surge in voluntary delistings is providing private equity (PE) funds with opportunities to restructure assets away from the quarterly pressures of public markets.

- Yield Compression and Valuation Gaps: Significant valuation discrepancies remain compared to global peers, offering fertile ground for alpha generation through active management.

Capital Recycling: Anchoring the $232B Portfolio in Alternatives

KIC’s expansion into the Japanese market is inextricably linked to its broader mandate of portfolio diversification. To combat global volatility and traditional yield compression, the fund has aggressively scaled its exposure to alternative assets. By the close of 2025, alternatives accounted for $50.8 billion—representing approximately 21.9% of the total assets under management (AUM)—validating the fund’s commitment to high-alpha private markets.

The growth potential in Japan is particularly compelling when contrasted with other developed markets. While Japan’s PE transaction volume has reached record highs—consistently exceeding 3 trillion yen annually over the last five years—the overall "involvement" level of private equity remains significantly lower than that of the United States. This gap suggests a long runway for growth, positioning KIC’s Tokyo office as a strategic bridgehead for securing high-quality assets before the market reaches full maturity.

A Global Network: Tokyo as the Final Piece of the APAC Puzzle

For a sovereign wealth fund of KIC’s scale, local presence is the ultimate competitive advantage in the pursuit of alternative deal flow. The Tokyo office joins an established network of global hubs—New York, London, Singapore, Mumbai, and San Francisco—completing a circuit that allows for 24-hour market coverage and localized risk assessment.

The mandate for the Tokyo team will be dual-faceted, reflecting a sophisticated understanding of cross-asset synergy. While the office is tasked with hunting for mid-market PE deals, private debt, and hedge fund opportunities, it will also maintain rigorous oversight of traditional asset classes. This allows KIC to monitor macro shifts in Japanese Government Bonds (JGBs) and fixed income while simultaneously executing on value-creation opportunities in the private sector.

As Japan continues to reform its corporate identity, KIC’s permanent presence in Tokyo ensures the fund is no longer just a spectator to the "Value-Up" era, but a primary beneficiary of its long-term trajectory.