Elevating the Equity Story: Japan’s FSA Issues 2025 Benchmark for Corporate Transparency and Sustainability Disclosure

The Financial Services Agency (FSA) has released its "2025 Collection of Good Practices in Descriptive Information Disclosure." This document serves as a strategic playbook for listed companies, moving toward a model of "narrative reporting" that bridges the gap between ESG initiatives and financial value creation.

As the Japanese market continues to attract record levels of foreign capital, the demand for "decision-useful" information has never been higher. The FSA’s 2025 report makes it clear: investors are now demanding quantified financial impacts, clear linkages between human capital and profit, and granular roadmaps for the dissolution of cross-shareholdings.

I. From Compliance to Connectivity

The core philosophy of the FSA’s latest report is "Connectivity." The agency emphasizes that sustainability data is meaningless if it is divorced from the company’s core business strategy. According to the report, leading companies are now integrating their Annual Securities Reports (Yukashoken Hokokusho) with their Sustainability Reports, ensuring a consistent equity story.

Investors and analysts have identified a critical need for companies to define "financial materiality." While many Japanese firms have historically listed environmental and social issues under a broad "CSR" umbrella, the 2025 guidelines require a shift toward the Sustainability Standards Board of Japan (SSBJ) framework. This means identifying risks and opportunities that have a "reasonable likelihood" of affecting a company’s cash flows, access to finance, or cost of capital over the short, medium, or long term.

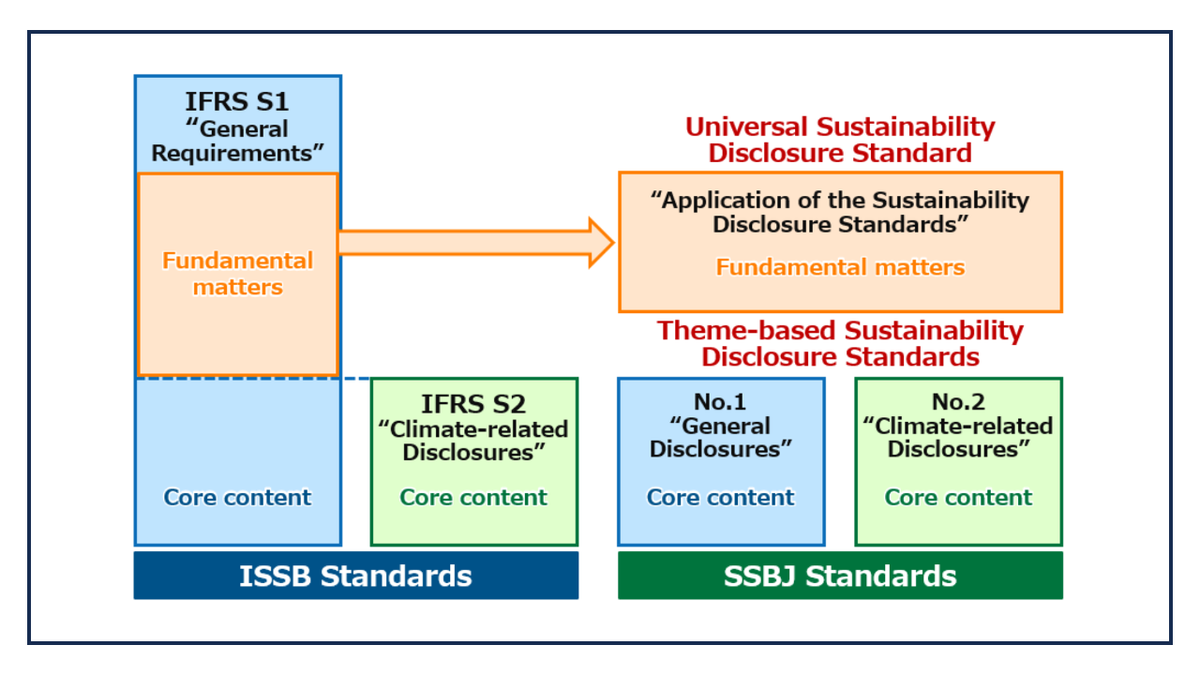

II. Sustainability and the SSBJ Frontier

A significant portion of the document is dedicated to the new SSBJ standards. The report highlights that while many companies list "Materiality Items," they often fail to explain the process of how these items were selected or how they are prioritized.

Case Study: Ricoh

The FSA identifies Ricoh as a benchmark for governance in sustainability. Ricoh provides a detailed diagram of its "ESG Committee" chaired by the CEO, which reports directly to the Board. Crucially, Ricoh has integrated ESG targets into executive compensation. The report notes that 20% of the evaluation for representative directors is now tied to ESG indicators, such as the Dow Jones Sustainability Index (DJSI) rating and internal female management ratios. This provides the "teeth" that institutional investors look for when assessing the legitimacy of a company’s sustainability claims.

The ICP Mandate: Internal Carbon Pricing

The report underscores the rising importance of Internal Carbon Pricing (ICP). Leading firms like Tokuyama Corporation and INPEX are now using ICP as a tool for capital allocation. For instance, Tokuyama disclosed a carbon price of 10,000 JPY/t-CO2, which is integrated into the ROI calculations for all new investment projects. This allows investors to see how a potential "carbon tax" would impact the firm’s future profitability.

III. Climate Change and Scenario Analysis

While TCFD (Task Force on Climate-related Financial Disclosures) reporting has become standard in Japan, the FSA is pushing for higher resolution in scenario analysis. Investors are no longer satisfied with general statements about "4-degree vs. 1.5-degree" worlds; they want to know which specific factories are at risk of flooding and what the specific cost of mitigation will be.

TOPPAN Holdings is cited for its "Environmental Correlation Map." This visual tool links the company’s dependency on natural capital (such as forest resources for paper) to specific financial risks. TOPPAN’s disclosure breaks down financial impacts into three categories: Small (less than 1 billion JPY), Medium (1 to 10 billion JPY), and Large (over 10 billion JPY). This level of quantification is exactly what analysts need to build accurate discounted cash flow (DCF) models.

Furthermore, the report highlights the transition from TCFD to TNFD (Taskforce on Nature-related Financial Disclosures). Companies like Bridgestone are praised for their "Nature-Positive" roadmap, which identifies specific water-stressed regions in their global supply chain and sets measurable targets for water neutrality.

IV. Human Capital: The ROI of Talent

Perhaps the most scrutinized section of modern Japanese reports is Human Capital. With Japan’s shrinking labor force, "Human Capital ROI" has become a vital metric for evaluating long-term competitiveness.

The Hitachi Model: Digital Talent and Lumada

Hitachi’s disclosure is highlighted for its direct linkage between human capital and its "Lumada" growth strategy. Hitachi reports the specific number of "Digital Professionals" (reaching 107,000 in FY2024) and how their skills align with the company’s pivot toward a software-centric business model. By showing a 119% increase in digital talent alongside a corresponding rise in Lumada-related revenue, Hitachi provides a clear "Proof of Concept" for its human capital investment.

Nissui and the "Human Rights Due Diligence" (HRDD)

In the seafood industry, labor rights are a high-risk area. Nissui is recognized for its transparent reporting on human rights audits in its Vietnamese shrimp supply chain. Nissui admitted to identifying specific areas for improvement and disclosed the exact percentage of suppliers who have signed the company's "Sustainability Action Guidelines" (98.2%). This transparency builds trust with ESG-focused funds that prioritize supply chain integrity over polished PR statements.

V. The Dissolution of "Cross-Shareholdings"

For decades, the "silent" ownership of shares between business partners—known as cross-shareholdings—has been a point of contention for foreign investors who view it as a barrier to capital efficiency. The 2025 FSA report shows that the tide has finally turned.

J. Front Retailing is lauded for its aggressive and transparent reduction plan. The company disclosed a "Heat Map" of its shareholdings, categorized by "Strategic Necessity" and "Capital Efficiency." Any shareholding that falls into the "Low Necessity/Low Efficiency" quadrant is slated for immediate sale. The company provided a clear timeline for these sales, pledging to return the proceeds to shareholders or reinvest them in high-growth areas like digital transformation (DX). This moves the conversation from "keeping old ties" to "optimizing the balance sheet."

Executive Compensation and Accountability

The report also highlights NTT Data Group for its disclosure on executive pay. The company now provides a "Pay-for-Performance" graph that shows the correlation between total shareholder return (TSR) and CEO compensation. This alignment ensures that management is incentivized to think like owners, a key requirement for the "Corporate Governance Code."

VI. Risk Management: Quantifying the Unthinkable

Risk disclosure in Japan has historically been criticized for being too vague (e.g., "There is a risk of earthquakes"). The 2025 "Good Practices" collection points toward firms like Meidensha Corporation and DIC Corporation as leaders in risk quantification.

Meidensha’s report includes a "Risk Velocity" metric—how fast a risk can manifest (e.g., a cyberattack has high velocity, while climate change has low velocity). This allows the board to prioritize resources effectively. DIC Corporation is noted for its "Financial Impact Scale," where every identified business risk is assigned a potential loss value, allowing investors to stress-test the company’s equity value against various black-swan events.

VII. Management Discussion and Analysis

The MD&A section is the heart of the Annual Securities Report. The FSA report highlights that the best MD&A sections do not just repeat the financial tables but explain the variance.

Takeda Pharmaceutical Company is cited for its transparent explanation of "Non-GAAP" metrics like Core Operating Profit. By stripping away one-time acquisition costs and explaining the underlying performance of its "five key business areas," Takeda provides a cleaner view of its earning power.

Capital Allocation Transparency

Investors are also looking for a clear "Capital Allocation Policy." Organo Corporation provided a three-year cash flow forecast, showing exactly how much cash would be generated, how much would be used for R&D, and how much would be returned as dividends. This "Cash Waterfall" chart is noted as a best practice for companies looking to reduce their "conglomerate discount."

VIII. Machine Readability and the AI Era

In a forward-looking note, the FSA report mentions that as more analysts use AI and Large Language Models (LLMs) to scan reports, the structure of descriptive information is becoming as important as the content. The agency encourages companies to use standardized headings and clear, concise text that can be easily parsed by machine-reading tools. This ensures that a company’s positive ESG data is actually captured by the "scoring algorithms" used by global index providers like MSCI and Sustainalytics.

IX. Conclusion: The Road to 2026 and Beyond

The FSA’s "2025 Good Examples" is a declaration of Japan’s intent to lead in corporate disclosure. The agency concludes that the ultimate goal of disclosure is to facilitate a constructive dialogue between companies and their investors.

For the C-suite of Japanese corporations, the message from the FSA is clear:

- Quantify Everything: If a risk or opportunity is material, it must have a yen value attached to it.

- Link Strategy to People: Human capital is the engine of growth; show the mechanics of that engine.

- Be Transparent About Weakness: Investors value a company that admits to a 5% female management ratio but provides a 5-year plan to reach 20%, more than a company that hides behind vague promises.

- Optimize the Balance Sheet: The era of "strategic shareholding" is ending. Use that capital for growth or give it back.

As we move toward the 2026 reporting season, the companies highlighted in this report—Ricoh, Hitachi, TOPPAN, and others—will set the standard. The gap between the "disclosers" and the "non-disclosers" is likely to widen, and the market will respond accordingly with its capital.