LY Corporation: Navigating Subsidiary Headwinds to Forge a Post-Search AI Powerhouse

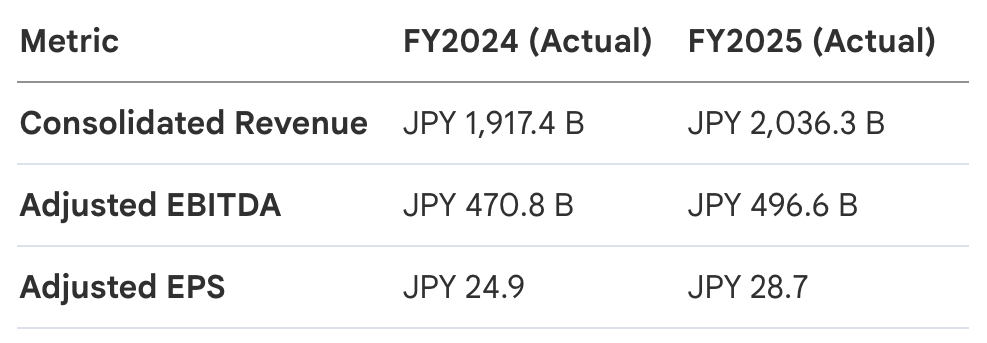

LY Corporation’s Fiscal Year 2025 performance was a masterclass in operational resilience. The company successfully navigated a significant internal crisis—the system outage at its subsidiary ASKUL—while maintaining both top-line and bottom-line expansion. This ability to absorb a temporary shock to its Commerce segment without derailing group-wide momentum highlights a robust underlying business structure. While consolidated growth was steady, it masked the aggressive 13.3% revenue growth and 12.6% Adjusted EBITDA growth achieved when excluding the ASKUL impact, signaling that the company’s core pillars are performing at a higher velocity than the surface-level figures suggest.

LY Corporation maintained a healthy Adjusted EBITDA margin of 24.4% despite a massive JPY 137.4 billion total increase in COGS and SG&A expenses. This stability is evidence of high operating efficiency; the Media and Strategic segments essentially subsidized the ASKUL recovery and the company's substantial investments in generative AI. By keeping margins firm amid rising costs, management has demonstrated that its financial engine is primed to fund the next stage of its evolution across its three primary business pillars.

1. Segment Analysis: Media, Commerce, and the PayPay "Strategic" Engine

The revenue mix at LY Corporation is undergoing a calculated shift. The company is pivoting away from its historical reliance on traditional search-based media and toward a high-margin, transactional ecosystem fueled by financial services and integrated commerce.

Media Business

The Media segment remains a tale of two trajectories. While Account Advertising surged by 15.3% (reaching JPY 145.7 billion), traditional Search Advertising is being fundamentally disrupted. Management has identified a 13% displacement of search queries by AI-generated answers—an "unavoidable trend" where users receive answers in chat formats, reducing traditional impressions. Rather than fighting this tide, LY Corporation is evolving Search into "Agent-based ads" and doubling down on LINE Official Accounts (OA). With 493,000 paid accounts globally and a double-digit rise in pay-as-you-go billing, LINE OA is now the primary growth engine for the segment.

Commerce Business

Commerce remains the recovery story for FY2026. While the ASKUL incident weighed heavily on current profits (a JPY 28.4 billion EBITDA hit), segments like Reuse and Travel/F&B grew by 14.0% and 15.5% respectively. A critical pivot is set for September 2026: Yahoo! JAPAN Shopping will transition from an advertising-dependent model to a sales-based royalty (commission) model. This move is designed to stabilize the ship; by ensuring the total fee burden on merchants does not rise, management is prioritizing merchant satisfaction while building a more predictable, transaction-linked revenue stream.

Strategic Business

PayPay has officially transitioned from a cash-burn startup to a cash-flow engine. The Strategic segment's Adjusted EBITDA surged by 85.0% YoY, with PayPay Consolidated crossing the JPY 100.0 billion EBITDA milestone (reporting JPY 111.1 billion). This performance was so strong that it drove a JPY 10 billion upward revision to the consolidated Group EBITDA guidance. With 73.36 million registered users, PayPay now provides the reliable capital base necessary to fund the Group’s aggressive AI transformation.

2. The "Agent i" Strategy: Evolving the LINE Ecosystem for the AI Era

The "Agent i" initiative is a fundamental self-transformation. With over 80% of the Japanese population not yet using generative AI daily, LY Corporation sees a vacuum it is uniquely positioned to fill. By integrating AI agents directly into the LINE interface—where the user base is already captive—the company aims to reclaim the search volume currently being lost to standalone chat interfaces.

The strategy targets specific, high-interest domains to drive user adoption:

- Agent i (Consumer): Evolving services into personalized agents for domains such as Manga, Fan Activities, Healthcare, and Finance.

- Agent i for Business: Deploying "AI Staff" and "AI Concierges" to automate customer engagement and operations for the over 1 million business accounts.

- LINE Revamp: A fundamental redesign of the Home Tab to serve as a personalized, AI-first gateway, increasing user dwell time and engagement frequency.

Crucially, management has secured the "cost-preceding-revenue" flank. Through an agreement with SoftBank Group, LY Corporation has capped OpenAI licensing costs at approximately JPY 10 billion per year. This stable cap allows the company to scale "Agent i" usage aggressively without the fear of runaway operational expenses. The monetization roadmap is equally clear: expanding LYP Premium billing, introducing agent-based advertising to replace lost search volume, and charging for the new "AI Mode" within LINE Official Accounts.

3. Capital Allocation and Shareholder Return Policy

LY Corporation has set an ambitious target of 8% ROE by FY2030, a significant spread over its current cost of equity, which sits between 4.1% and 5.1%. This roadmap signals a move toward aggressive capital efficiency.

The shareholder return policy has been upgraded to reflect management’s confidence:

- Dividend Hike: A significant increase to JPY 11 per share is forecast for FY2026.

- Equity Base Reduction: Management is intentionally using a total payout ratio target of 70%—including strategic share buybacks—as a tool to reduce the equity base. Shrinking the equity base is a tactical move to accelerate the path toward the 8% ROE target.

- Growth Buffer: The company is carrying over approximately JPY 100 billion in "buffer" capital. This provides the flexibility to fund additional M&A or further shareholder returns without straining the balance sheet.

This shift from "stable dividends" to "dividends aligned with profit growth" indicates that management views the company as a mature cash generator ready to return value while simultaneously reinventing itself through AI.

4. FY2026 Outlook: Guidance and Market Expectations

Heading into Fiscal Year 2026, LY Corporation is projecting double-digit growth across the board as it moves past the ASKUL headwinds.

Forward-Looking Targets (FY2026)

- Revenue: JPY 2.24 T (+10.0%)

- Adjusted EBITDA: JPY 585.0 B (+17.8%)

- Adjusted EPS: JPY 30.0

A notable driver for the "Other/Adjustments" segment’s improved profit outlook is the tapering of the "Next Career Support Program," with both participants and overall costs expected to decline significantly. Furthermore, cybersecurity licensing fees are projected to drop from JPY 8 billion to approximately JPY 2–3 billion.

While Adjusted EPS growth appears modest at +4.4% due to the reversal of one-time tax impacts, the operational reality is one of accelerating momentum. With ASKUL expected to return to pre-incident profit levels and the Strategic segment projected to grow revenue by 32.1%, FY2026 will serve as the "Proof of Concept" year for LY Corporation’s AI-first, transactional business model.