Sony Financial Group Posts 71% Surge in Adjusted Net Income

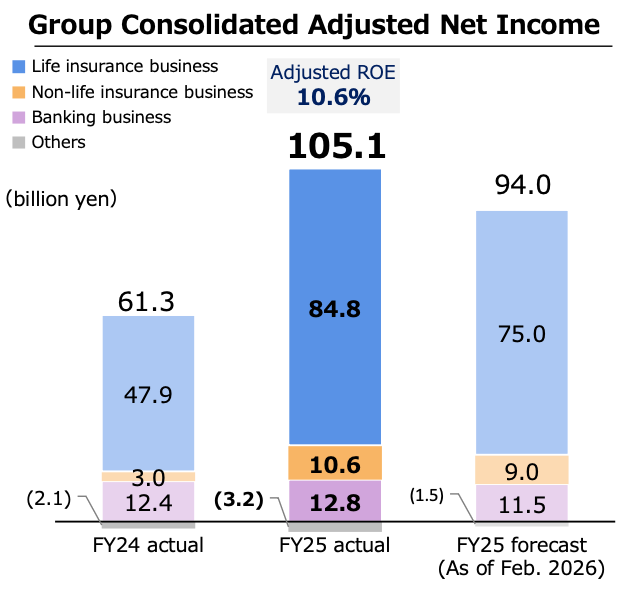

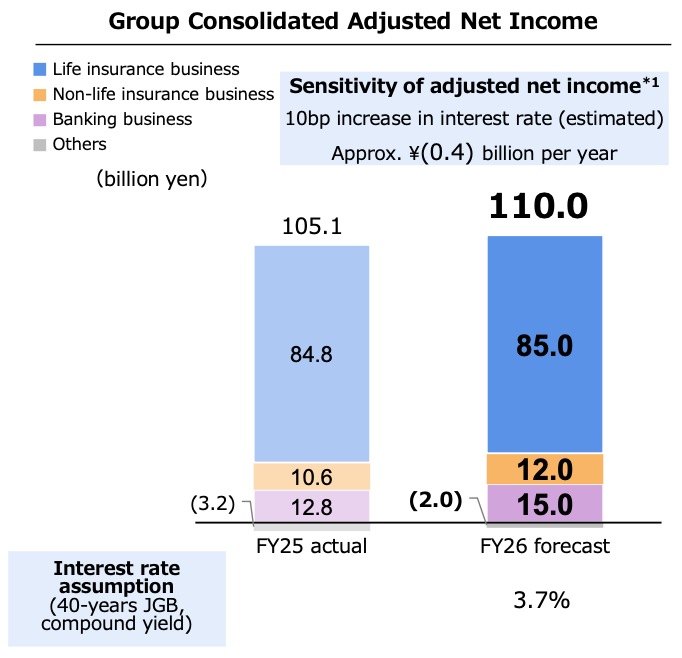

Sony Financial Group (SFG) has delivered a standout performance for the fiscal year ended March 31, 2026 (FY2025), underpinned by a 71% year-on-year surge in adjusted net income. As the Group navigates its full transition to International Financial Reporting Standards (IFRS), "Adjusted Net Income" has emerged as the definitive metric for assessing sustainable earning power. By filtering out market-driven volatility and one-time items, this indicator highlights SFG’s success in expanding its core business through a disciplined cycle of investment and returns. The ¥105.1 billion result not only marks a recovery from previous periods but signals a significant expansion of the group's underlying profitability.

This performance comfortably surpassed the group’s previous forecast of ¥94.0 billion. The Life Insurance segment remains the primary driver of the bottom line, contributing ¥84.8 billion, but the diversification benefits from the Non-Life Insurance (¥10.6 billion) and Banking (¥12.8 billion) segments were critical in exceeding targets. This tripartite growth demonstrates the resilience of the group’s unique business model in a shifting macroeconomic climate.

While the group overall is on an upward trajectory, a closer examination of the Life Insurance segment reveals a complex interplay between record growth and structural interest rate pressures.

1. Sony Life: Balancing Record Growth with Structural Headwinds

Sony Life continues to serve as the group's central profit engine, currently undergoing a strategic shift toward a "capital-light" model. This strategy prioritizes protection-type products, which are less capital-intensive and facilitate a more efficient release of the Contractual Service Margin (CSM)—the unearned profit representing future earnings potential.

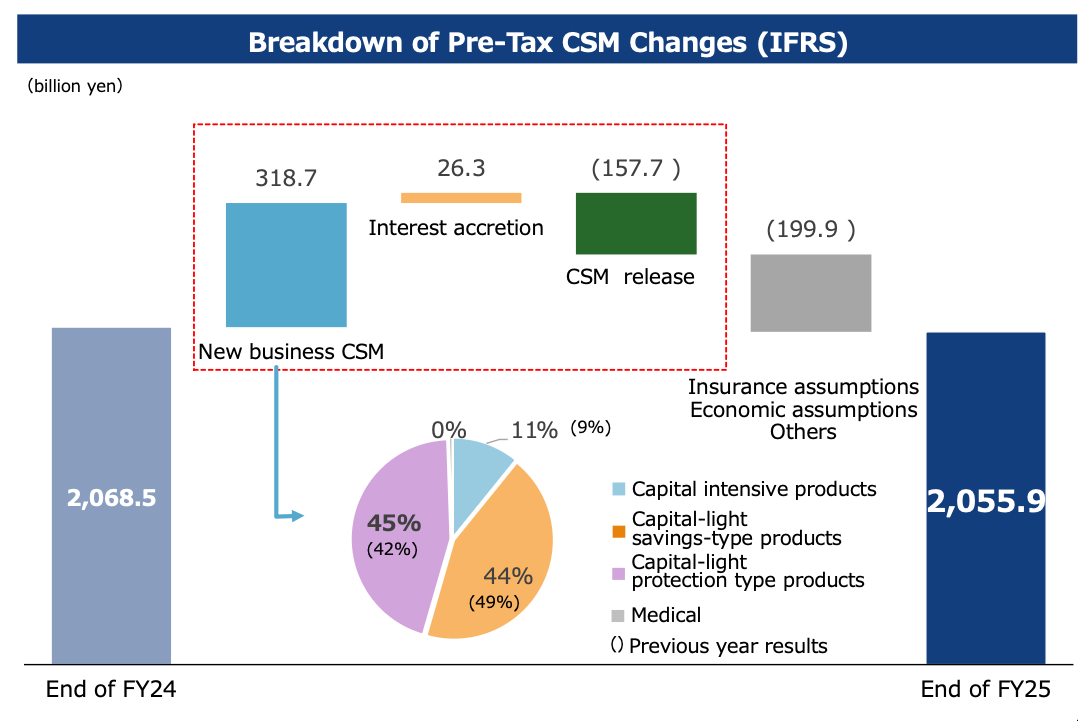

The segment’s adjusted net income rose 76.9% to ¥84.8 billion. The rationale behind this sharp increase is found in a combination of fundamental growth and specific tailwinds. Performance was significantly boosted by the absence of the impact of the defense special corporation tax introduction that occurred in FY2024 (+¥21.0 billion) and a reduction in repurchase costs (+¥12.0 billion). From a business standpoint, the growth was supported by ¥173.0 billion in annualized premiums from new policies, driving a 5% increase in CSM release to ¥157.7 billion. However, it is important to note that the total CSM balance saw a slight decline from ¥2,068.5 billion to ¥2,055.9 billion, as the accumulation of new business was offset by assumption revisions.

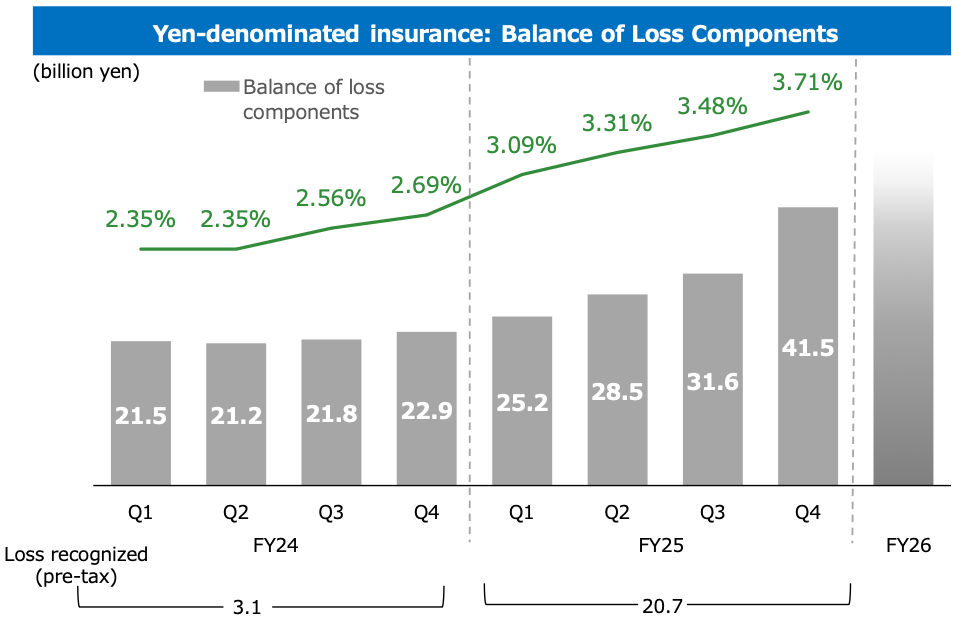

The segment is also navigating structural pressures from "Loss Components." As the 40-year JGB yield rose significantly—climbing 102 basis points from 2.69% to 3.71%—certain legacy contracts from the 2000s and early 2010s have become onerous. This interest rate volatility necessitated a re-estimation of fulfillment cash flows. Behavioral factors have compounded this, with a trend of surrenders and switches in these specific older contract groups as customers move through different life stages, further elevating loss components.

Regarding governance, Sony Life is addressing an investigation into alleged misconduct involving approximately 30 customers. Following an April 30 reporting order under Article 128 of the Insurance Business Act, the company has implemented immediate preventive measures, including a "disclosure of authority" process to alert customers during applications and the adoption of a "paperless standard" for applications to eliminate fraudulent opportunities. A progress report on customer verification and the future schedule is expected by the end of May.

As Sony Life manages these legacy and structural hurdles, the more agile Non-Life and Banking segments have shown remarkable market resilience.

2. Sony Assurance and Sony Bank: Efficiency and Market Resilience

The diversification provided by SFG’s Non-Life and Banking segments continues to distinguish the group from traditional Japanese financial institutions. Sony Assurance’s direct-to-consumer model and Sony Bank’s foreign currency expertise provide operational flexibility that is particularly effective in the current market environment.

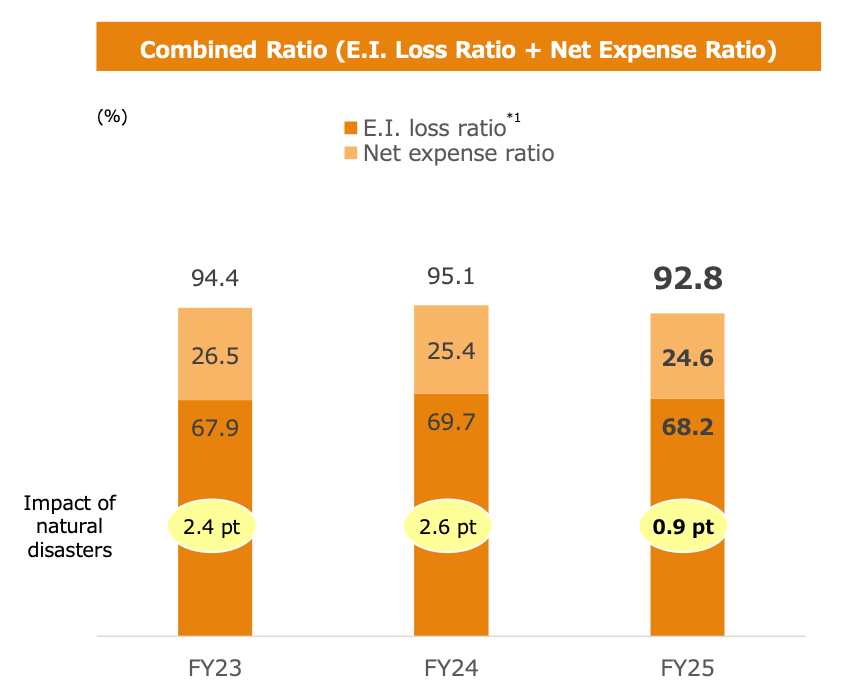

Sony Assurance delivered a 247.3% surge in adjusted net income, underpinned by a combined ratio that improved to 92.8%. This was driven by a lower loss ratio—benefiting from fewer natural disasters—and rigorous cost control. Despite implementing semi-annual premium rate revisions for auto insurance, policy retention remains high at over 90%, reflecting strong brand loyalty.

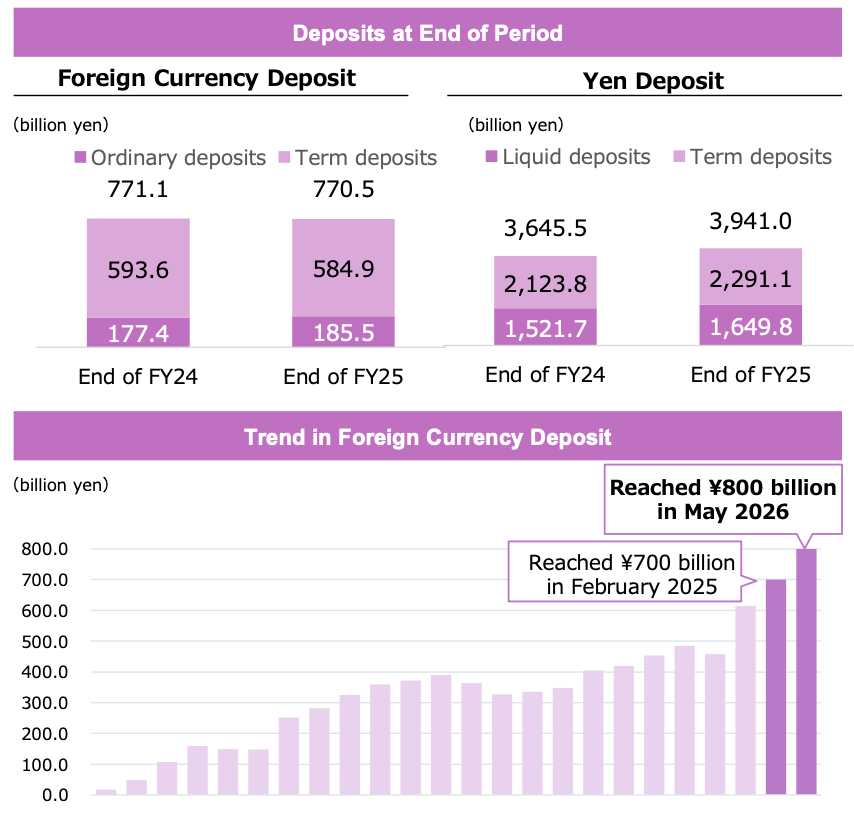

Sony Bank demonstrated resilience amid the yen’s depreciation. Although foreign currency deposit balances dipped to ¥770.5 billion due to profit-taking sales, most proceeds remained within the bank as yen deposits. This "fund circulation" secures stable interest margins. Crucially, Sony Bank’s deposit balance per account stands at ¥2.17 million—nearly 2.5 times the ¥0.85 million average of other online banks—highlighting a high-quality, sticky customer base. Additionally, the bank proactively adjusted mortgage and deposit rates in response to the Bank of Japan’s policy hike, successfully improving yen interest margins.

The operational strength of these segments bolsters the Group’s capital base, supporting a sustainable framework for shareholder returns.

3. Capital Solvency and the Shareholder Return Framework

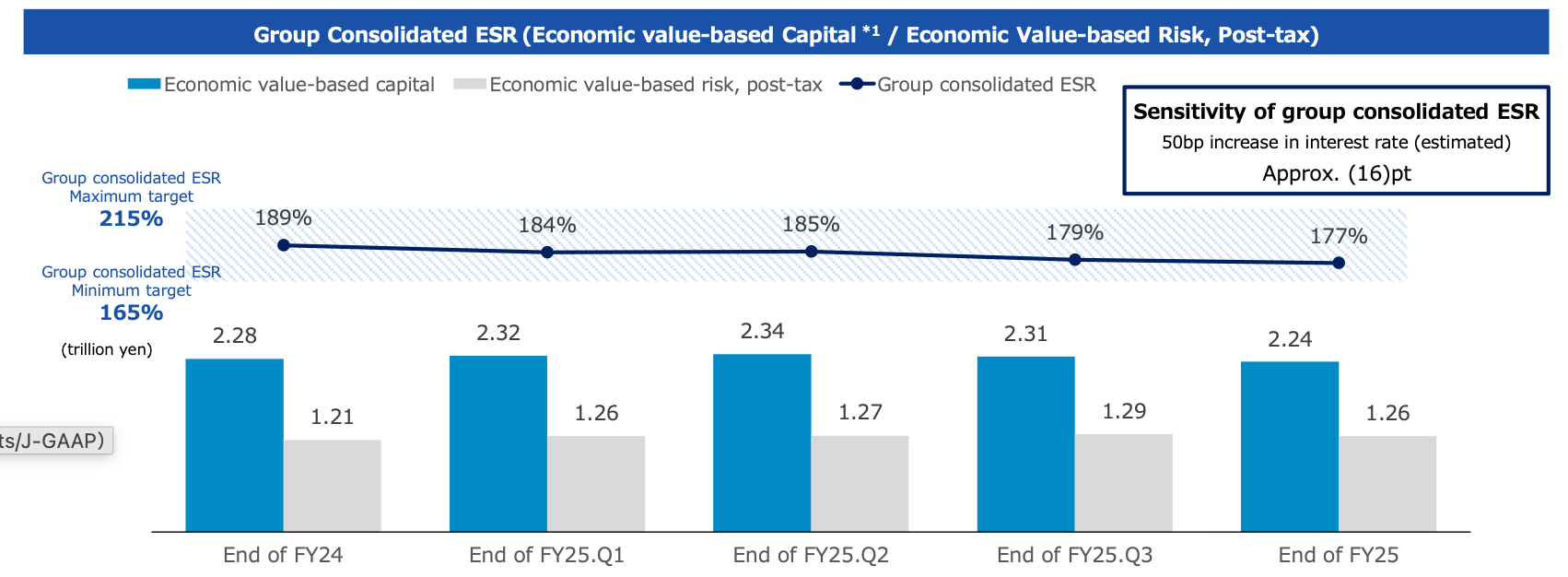

SFG maintains a rigorous focus on the Economic Solvency Ratio (ESR), a measure aligned with European Solvency II standards. A healthy ESR is the cornerstone of the group’s ability to manage risks in a volatile interest rate environment.

The Group Consolidated ESR ended FY2025 at 177%, a 12-point decrease year-on-year. This decline was primarily a result of:

- Macroeconomic Headwinds: A 36-point decrease caused by the sharp rise in interest rates (40-year JGB yield).

- Shareholder Actions: A 6-point decrease due to share repurchases.

- Mitigation and Growth: These were partially offset by an 8-point gain from new policy acquisition and a 23-point increase from financial measures, including the use of derivatives, FX hedges, bond sales, and subordinated financing.

Despite this decline, SFG is raising its FY2026 dividend forecast to ¥8.0 per share, a 5% increase. The group's "Basic Shareholder Return Policy" remains focused on stable dividend growth, targeting a payout ratio of 40% to 50% of IFRS adjusted net income.

4. Strategic Outlook: FY2026 Forecast and the IFRS Transition

The first quarter of FY2026 will mark SFG’s official transition to IFRS for its primary accounting standards, a move designed to enhance international comparability and transparency for the global investment community.

However, management has revised the FY2026 Adjusted Net Income forecast to ¥110 billion, down from the previous Mid-Range Plan target of ¥125 billion. This revision accounts for structural "weights" at Sony Life, specifically the continued emergence of loss components linked to the rising 40-year JGB rate and behavioral trends in legacy contract groups.

On an IFRS basis, the group anticipates a pre-tax loss of ¥20.0 billion for FY2026. This projected loss is a strategic byproduct of "ALM (Asset-Liability Management) rebalancing." Specifically, the group plans to execute bond sales to strengthen its long-term financial base, prioritizing portfolio stability and capital efficiency over short-term accounting profits.

As SFG enters FY2026, the focus is twofold: formulating the next Mid-Range Plan to return Sony Life to a growth trajectory and leveraging the robust efficiency of its Banking and Non-Life businesses to navigate a complex macroeconomic landscape.