PayPay Hits FY2025 Milestones as Financial Services Growth Outpaces Payments

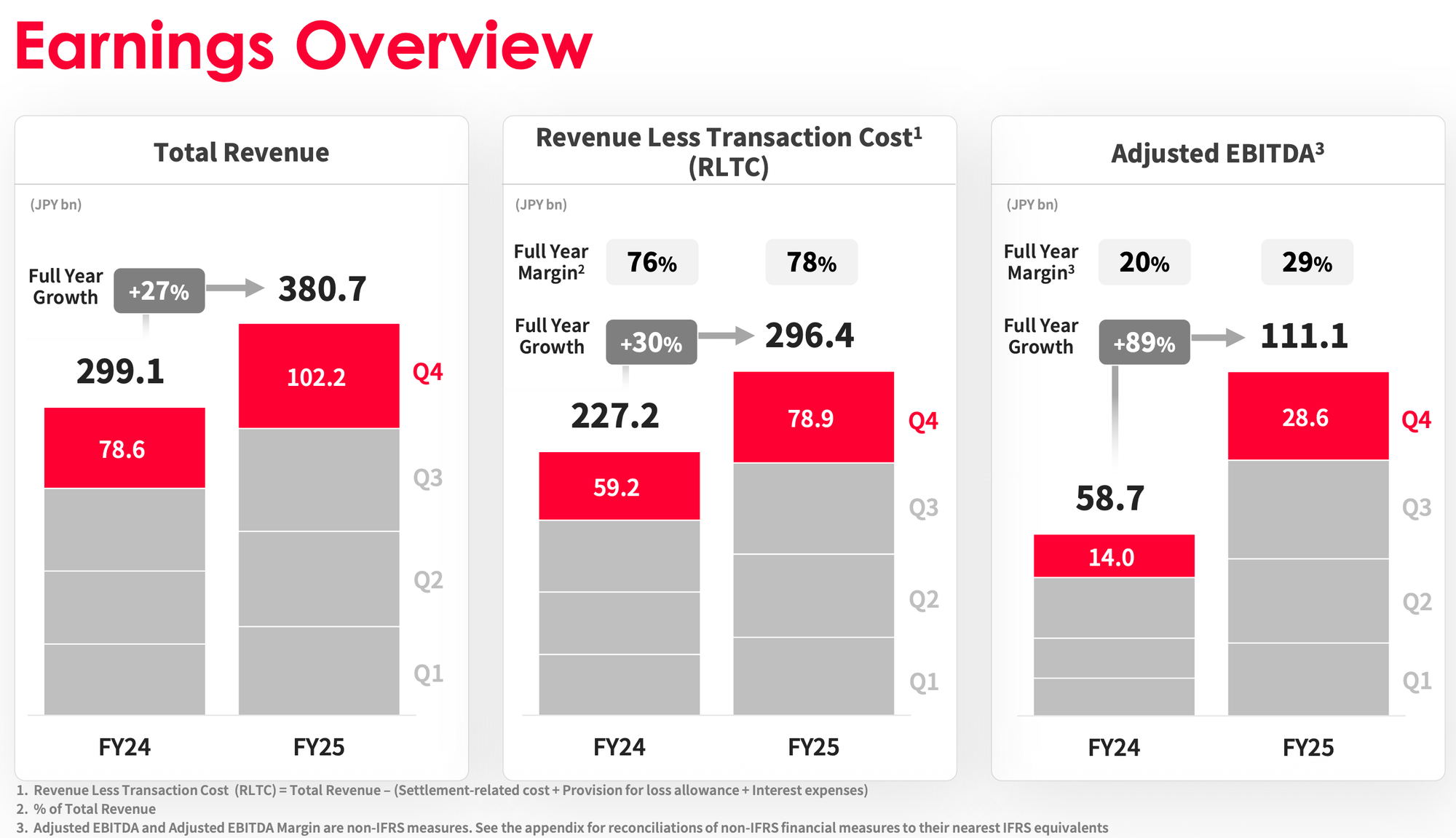

In his opening remarks for the fiscal year ending March 2026 (FY2025), PayPay CEO Ichiro Nakayama signaled a balanced model of sustainable, high-margin profitability. The hallmark of this strategy is the achievement of a "Rule of X" score of 56—a metric combining the firm's 27% revenue growth with a 29% Adjusted EBITDA margin. This result validates PayPay's strategy of converting a massive, utility-based payment network into a self-sustaining financial powerhouse. For professional investors, the message is clear: PayPay is harvesting the platform’s "earnings power" through disciplined cost control and high-margin service integration.

The 78% RLTC margin is particularly telling; it underscores the platform’s increasing efficiency by isolating core revenue from variable transaction costs, providing a clean look at the underlying profitability of PayPay's infrastructure.

1. Segment Deep-Dive: The Financial Services Surge and CAC-Free Growth

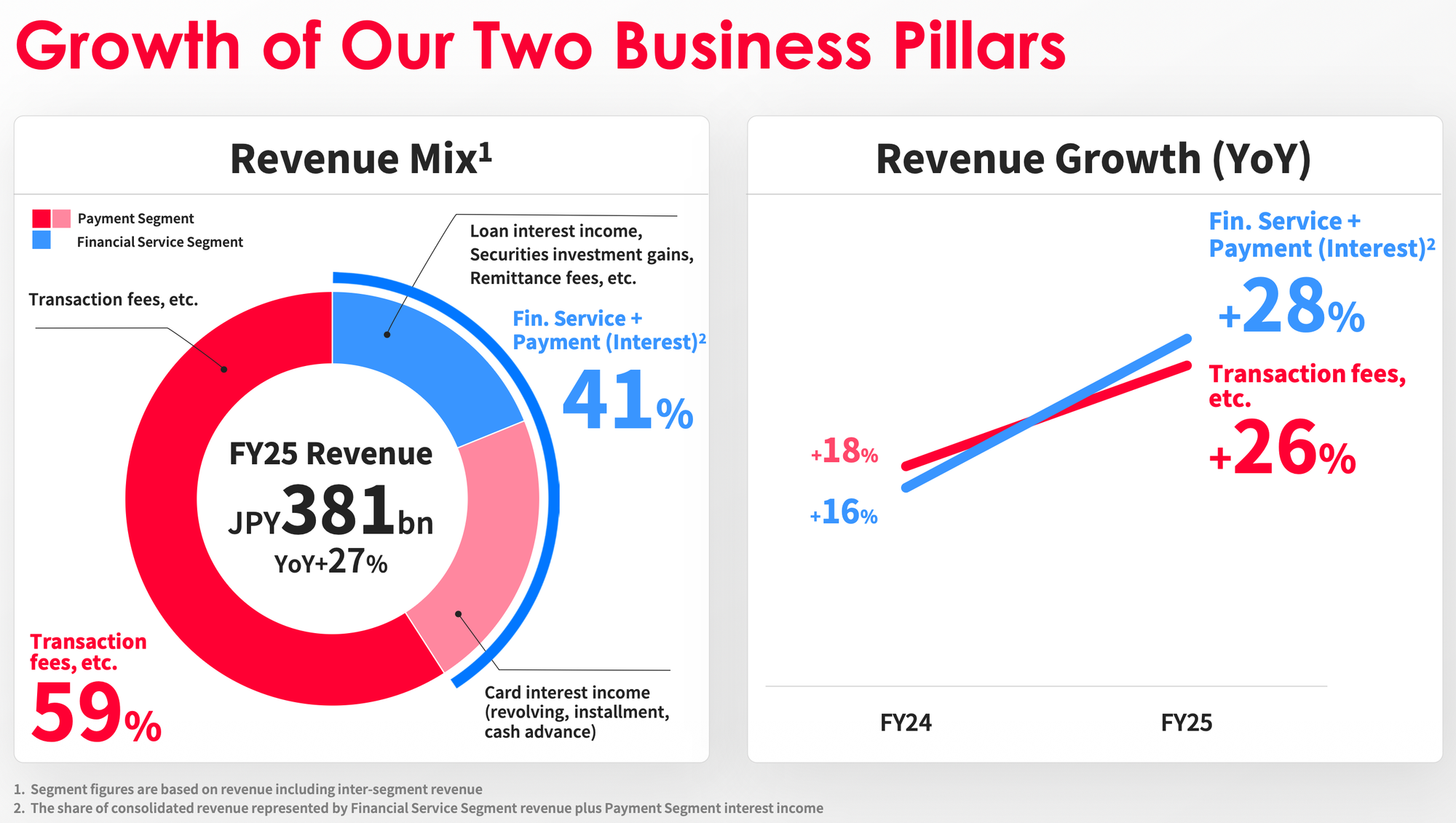

While the Payment segment remains the ecosystem's foundation with 27% YoY growth, the strategic center of gravity has shifted to Financial Services, which surged 47% in FY2025. This segment now accounts for 41% of total revenue, illustrating a "redefinition of everyday finance." PayPay’s primary competitive advantage is its ability to bypass traditional Customer Acquisition Costs (CAC). By weaponizing its 41 million Monthly Transacting User (MTU) base, PayPay is cross-selling banking, credit, and brokerage services with near-zero marketing burn—a feat traditional banks with aging infrastructure cannot replicate.

Key performance indicators for the three pillars of the segment include:

- PayPay Card: Ranked #1 in domestic net new card additions for CY2025. Leveraging proprietary underwriting, the card’s financing balance—including revolving and installment credit—grew by over 100 billion yen YoY.

- PayPay Bank: Reached the 10 million account milestone in April 2026. Growth is increasingly skewed toward the "lifetime value" demographic; accounts for users aged 12–28 have grown fourfold over the last five years.

- PayPay Securities: Achieved its first full-year operating profit in FY2025. A standout regulatory milestone was the distribution of PayPay’s own IPO shares via the "Public Offering Without Listing" (POWL) framework—a technically complex mechanism that added 360,000 new accounts and demonstrated PayPay's ability to navigate Japan's stringent retail brokerage regulations.

This "CAC-free" conversion of transacting users into financial clients is the primary engine behind the group’s margin expansion.

2. Strategic Catalyst: Data-Driven Lending and Underwriting Alpha

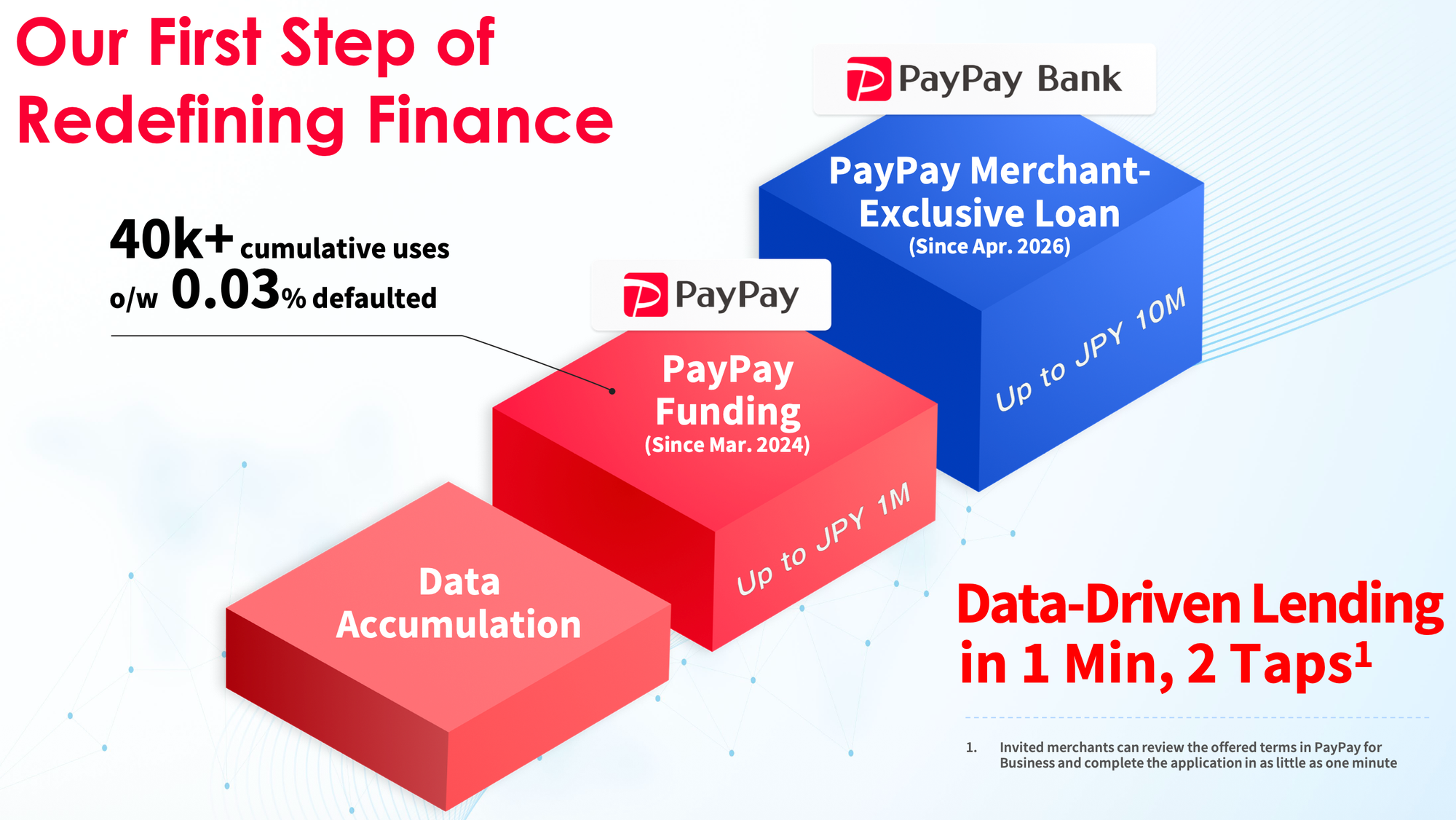

PayPay’s move into B2B lending via "PayPay Funding" (launched March 2024) and the "Merchant-Exclusive Loan" (full rollout April 2026) represents a direct challenge to the transactional banking sector. By integrating credit offers directly into the "PayPay for Business" app, the firm provides capital access in as little as one minute based on real-time transaction data rather than static collateral.

The effectiveness of PayPay’s proprietary underwriting is evidenced by a bifurcated risk profile: while the B2C PayPay Card maintains a highly disciplined 0.58% net charge-off rate, the merchant-side data-driven model has processed over 40,000 cumulative uses with a negligible 0.03% default rate. This "underwriting alpha" proves that real-time ecosystem data allows for more precise risk pricing than traditional banking models, enabling faster credit delivery without compromising asset quality.

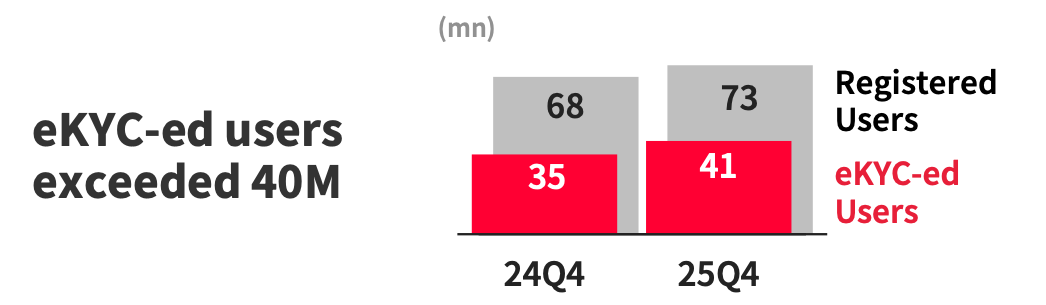

3. The EKYC Strategy: Strategic Filtering for High-LTV Growth

PayPay’s 41 million EKYC (Electronic Know Your Customer) verified user base is a filter for profitability. The expansion of this verified base is critical for:

- Cross-sale conversion: Verified users move into banking and securities at significantly higher rates.

- User Loyalty: EKYC unlocks advanced features like withdrawals and full fraud compensation, driving deeper app "stickiness."

- Societal Alignment: Meeting high security expectations reduces regulatory risk.

Management has signaled a "strategic filtering" of its user base with a point reward revision effective June 2026. By limiting standard rewards to EKYC-verified users, PayPay is creating a profitability lever that reduces expenses associated with low-engagement or unverified users while prioritizing the high-spending, high-LTV (Life Time Value) customers who drive the bulk of Gross Merchant Volume (GMV).

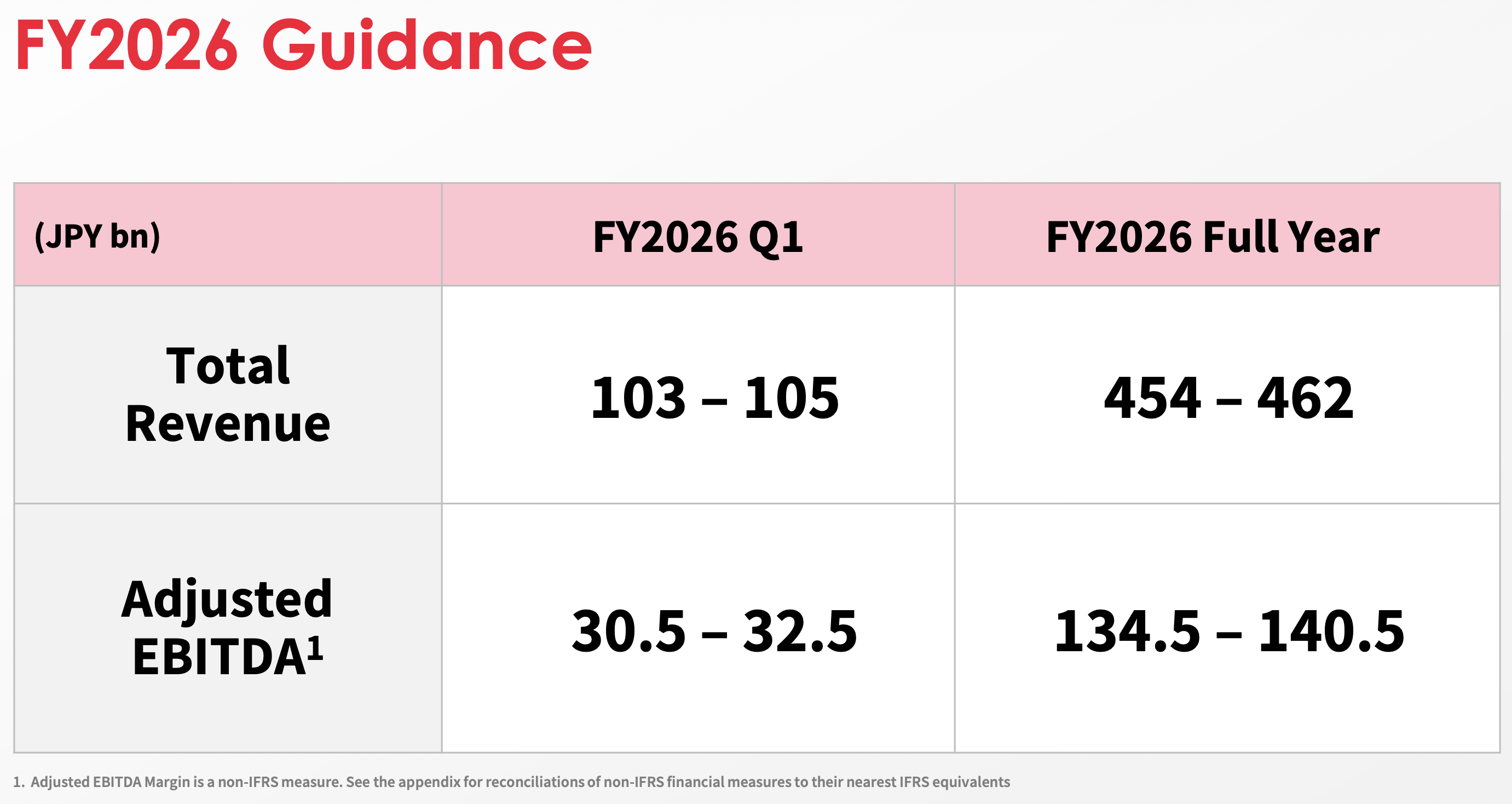

4. Balance Sheet Strength and FY2026 Defensive Positioning

PayPay concludes FY2025 with 5.2 trillion yen in total assets and an impressive 24% Adjusted ROE. Despite this strength, management's FY2026 guidance reflects a sophisticated understanding of the current macroeconomic volatility in Japan.

FY2026 Guidance Assumptions

- CPI Growth: ~2% YoY.

- Monetary Policy: Two 25-bps hikes assumed (July 2026 and January 2027).

- FX Rate: 155 yen per USD.

CFO Kagechika has adopted a conservative stance on short-term banking margins due to a specific "time lag" in interest rate pass-through. While deposit rates must be raised immediately following Bank of Japan hikes, mortgage loan yields typically reset on a six-month delay, creating temporary margin pressure. To mitigate this interest rate risk, the bank has proactively shortened the duration of its JGB (Japanese Government Bond) portfolio.

Despite these macro headwinds, management remains committed to its "beat and raise" philosophy. By leveraging its dominant user base to update Japan’s aging financial infrastructure, PayPay is positioning itself as the indispensable digital utility of the Japanese economy.