Riding the Demographic Wave: How Japan's Post- Peak Society Previews the Global Consumer Contraction

As the developed world marks a historic inflection point in consumer behavior, Japan stands as the global vanguard. According to an extensive bottom-up empirical evaluation of approximately 3,000 corporate entities by Goldman Sachs Research, the long-forecasted "Demographic Dilemma" has ceased to be a distant structural concern; it is actively altering corporate revenue profiles, redefining capital allocation, and forcing an aggressive reorganization of corporate portfolios.

For decades, macroeconomic models have warned that falling fertility rates and longer lifespans would create an unsustainable fiscal drag on advanced economies. However, the latest data from the UN Population Prospects and regional household surveys reveal a much more immediate operational hazard for corporate boards: a severe contraction in domestic addressable volume across prime-spending age cohorts. While emerging markets and select Western economies are only beginning to feel the initial deceleration of their core consumer engines, Japan has already crossed the crest of the demographic wave, offering an invaluable case study for investors trying to navigate the coming global shift.

1. The Post-Peak Trajectory: Japan's Contraction in Numbers

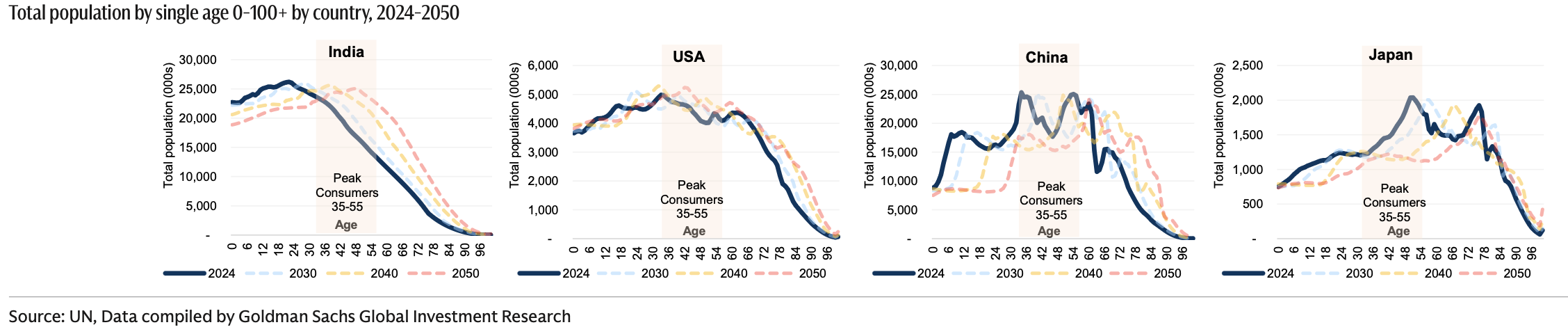

Japan's domestic market its numerical apex during the 2009–2010 period, peaking at an absolute population of approximately 128.2 million individuals. In the years since, the island nation has entered a structural downshift that has steadily accelerated. Recent census figures indicate that the Japanese population is contracting by an absolute net of 600,000 individuals per annum. According to internal demographic tracking compiled in recent corporate models, this contractionary velocity is set to widen into an absolute net decline of 700,000 individuals annually starting in 2028.

The medium-variant baseline projection maps out a steady and remorseless shrink: Japan’s aggregate population is model-forecasted to contract from 124 million in 2023 down to 119.5 million by 2030. It will hit 112 million by 2040 and collapse to 105 million by the midpoint of this century. Under strict zero-migration variants, these terminal figures drop even more sharply, threatening a near-halving of the nation's historical domestic consumer footprint by 2100.

Crucially, this population drop is not distributed evenly across age cohorts. The defining feature of Japan’s contemporary economy is the severe hollow-out of the "peak consumer" bracket—defined as individuals aged 35 to 55. This age group has historically driven the highest absolute quantities of discretionary consumer credit, vehicle purchases, and family-level retail consumption. As these cohorts age out into retirement without a matching replenishment from younger generations, the consumer core shrivels. The sole expanding cohort in the country is the senior demographic; the population aged 60 and older is projected to rise from 43.3 million in 2023 to a peak of 47.8 million by 2040, before stabilizing at 45.5 million by 2050 as absolute mortality curves catch up with the broader population decay.

2. The Corporate Diagnostic: Goldman Sachs' DDD Framework

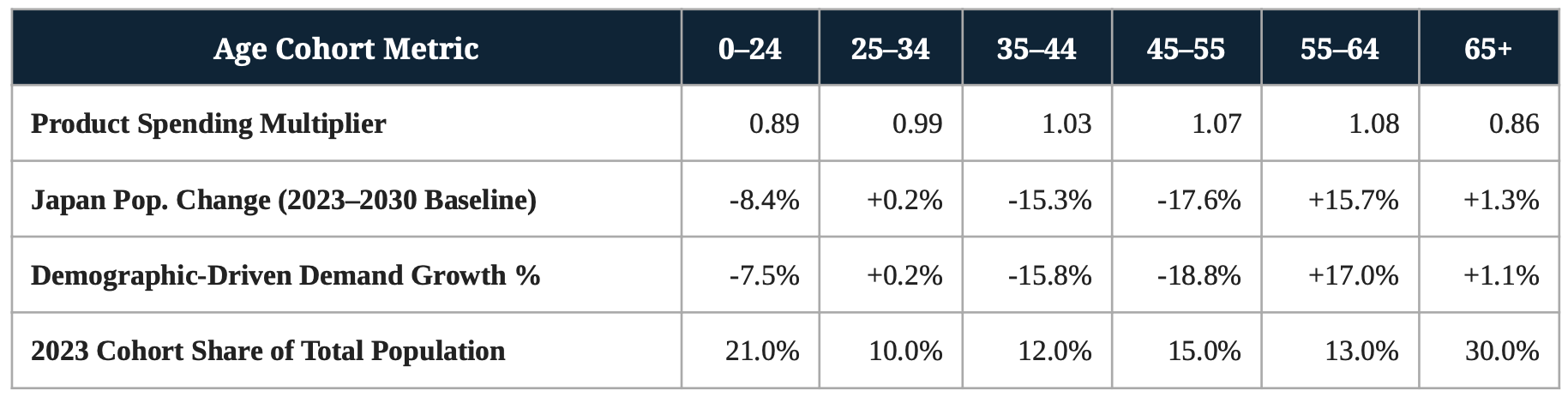

To quantify the precise operational impact of this shift, equity analysts have deployed a bottom-up framework known as Demographic-Driven Demand (DDD). This methodology blends granular government consumer spending surveys with company-specific product segments and regional geographic revenue exposures. The framework operates on a foundational premise: different age cohorts exhibit starkly immutable consumption multipliers across specific product lines. By running country-level age distribution shifts through these multipliers, analysts can accurately simulate the pure demographic tailwinds or headwinds acting on a specific business's top line, assuming corporate strategy and product mix remain constant.

The output of the DDD model for Japanese domestic revenue is striking. When mapping out a standard segment exposed to general consumer products within Japan, the pure demographic drag results in a structural headwind. As illustrated in the model's technical blueprints, an empirical baseline example reveals the mechanics of this drag:

When these age-specific growth figures are weighted by their respective population shares and aggregated, the model calculates a net final country-level demand impact of -3.8% through 2030 for standard consumer-facing segments. This implies that before accounting for brand strength, pricing power, or changing corporate strategy, a domestic Japanese firm in this segment faces a mandatory structural revenue headwind. Conversely, identical corporate operations positioned in the United States or India experience demographic tailwinds of +3.1% and +5.4% respectively over the same time horizon, strictly due to the more favorable positioning of their national consumer cohorts on the demographic wave.

3. The Retail and Apparel Trap: The Price of a Shrinking Youth Core

Nowhere are the consequences of this downshift more painfully evident than in the domestic Japanese retail and apparel sectors. In a standard consumer economy, fashion trends and volume demand are heavily dictated by the under-29 age bracket. In Japan, data from the Statistics Bureau indicates that an individual under the age of 29 spends approximately 1.3 times the median national consumer on clothing and footwear. In stark contrast, an individual in the 70+ demographic spends just 0.7 times the median consumer on apparel.

As a direct consequence of this divergence, the absolute structural volume of the Japanese fashion industry has been locked in a multi-decade downward slide. Total domestic consumer expenditure on clothing and footwear has tracked the contraction of the under-29 population nearly perfectly since 1994. With the youth cohort projected to shrink by an additional 6% by 2030, 16% by 2040, and a catastrophic 22.3% by 2050 relative to the 2023 baseline, the domestic addressable clothing market faces a severe drop in volume.

This structural pressure has induced two distinct survival behaviors within the Japanese retail landscape.

3.1 The Explosion of Second-Hand and Thrift Ecosystems

As the primary consuming base shrinks and real disposable wages remain constrained, consumers have increasingly migrated toward circular fashion economies and digital thrifting platforms. This trend has successfully captured the value-conscious mindset of the remaining youth core but has fundamentally cannibalized first-hand, high-margin manufacturing pipelines.

3.2 The Mid-to-High Price Deflationary Trap

Unable to rely on organic volume expansion, retailers have engaged in intense price competition, resulting in a severe hollowing-out of the domestic mid-market fashion tier. To maintain baseline operational margins, production lines have been aggressively outsourced to lower-cost manufacturing hubs, particularly mainland China. This shift has altered industry economics, leaving domestic retail revenue highly sensitive to fluctuations in the yen and global supply chain costs.

4. The Caloric Compression: Structural Volumetric Decay in Food and Beverage

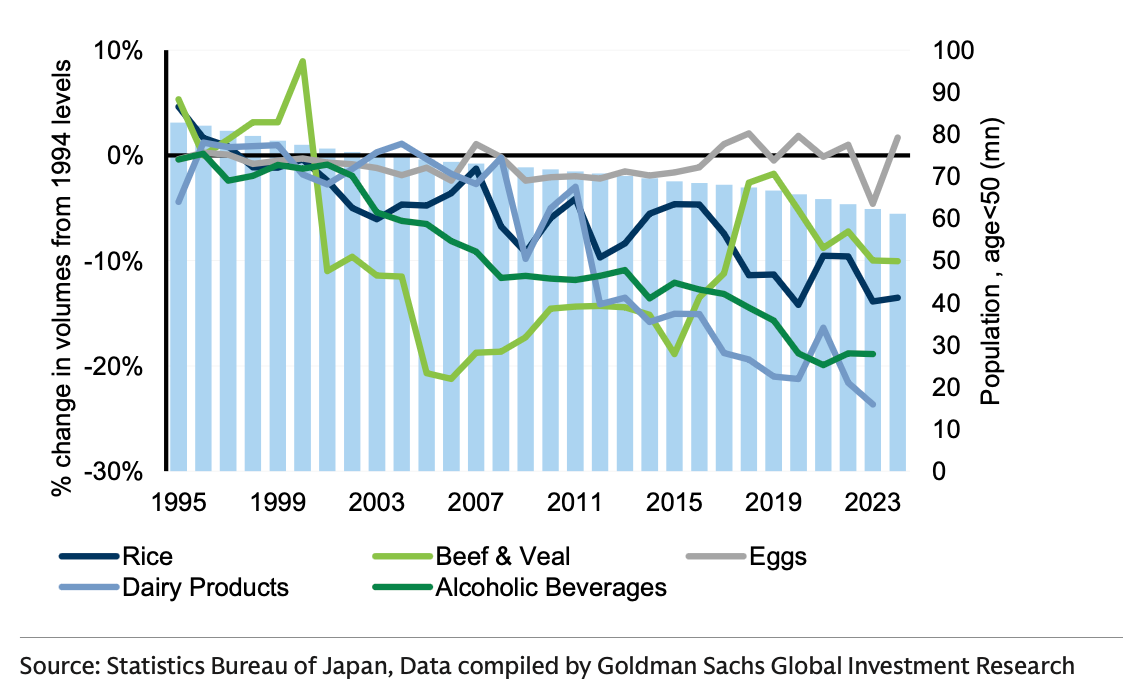

A parallel contractionary dynamic is sweeping across the consumer staples and food and beverage sectors. A population's gross caloric requirement is fundamentally determined by the size and concentration of its active workforce and youth demographics; metabolisms and physical labor patterns mean individuals under the age of 50 consume substantially more calories per capita than retirees.

As Japan’s under-50 population has steadily decayed, the absolute volume demand for major staple categories has contracted. Long-term technical data from the Statistics Bureau of Japan reveals that since 1994, absolute domestic consumption volumes have dropped significantly: rice consumption has declined by 14%, aggregate dairy products have fallen by 23%, and commercial alcoholic beverages have shrunk by 19%. This compression cannot be explained away as a mere shifting of consumer tastes or a trend toward premium options; it represents a structural, volume-driven contraction in the aggregate domestic stomach.

Faced with a structurally shrinking domestic market, forward-looking staples firms are aggressively re-engineering their product portfolios. Companies are shifting production away from high-volume, bulk family packages toward hyper-targeted single-serve units designed for single-person elderly households. Furthermore, research and development capital is being heavily reallocated toward therapeutic nutrition, functional wellness beverages, and medical-grade foods. These specialized categories allow manufacturers to defend absolute margins by capturing higher average selling prices (ASPs) from senior citizens managing chronic metabolic and age-related health conditions.

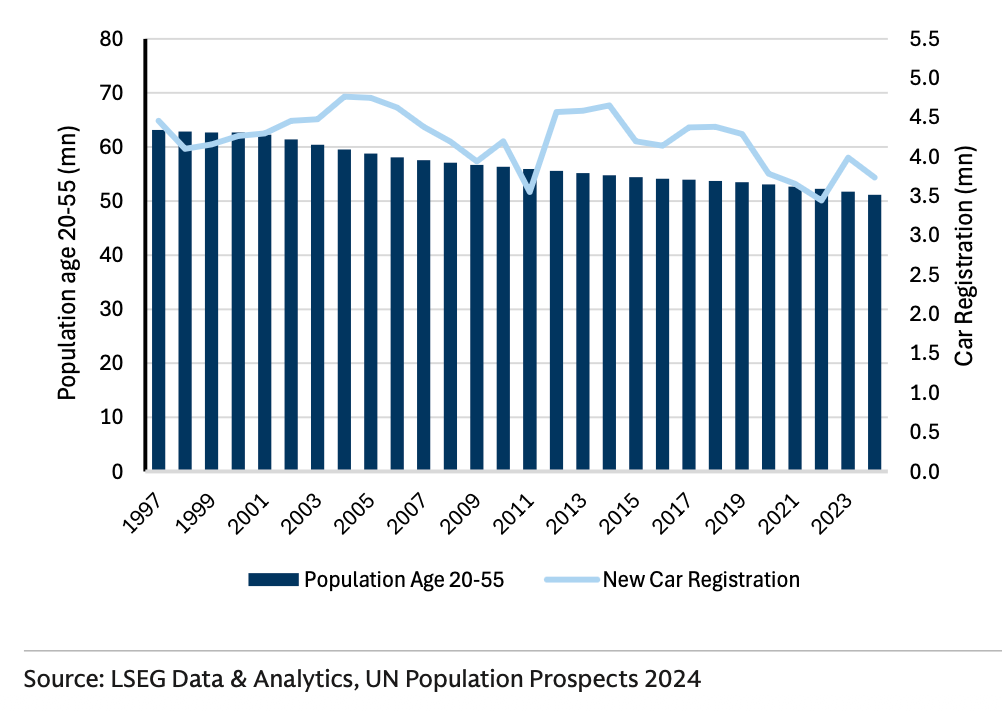

5. The Automotive Crossroads: Falling Vehicle Registrations and Silver Mobility

The Japanese automotive market offers perhaps the most visible indicator of how structural demographic shifts impact big-ticket consumer durables. Historically, the lifecycle of automotive consumption relies on the prime driving-age population—individuals aged 20 to 55—who enter the market as first-time new car buyers and subsequently cycle through lease renewals and trade-ins.

In mature, demographically post-peak markets like Japan and Germany, the contraction of this specific driving-age population has tracked with a steady decline in absolute new vehicle registrations. Long-term registry data from 1997 through 2024 demonstrates an explicit visual correlation: as the absolute volume of the 20–55 cohort contracts, baseline light vehicle sales downshift in lockstep. While cyclical macroeconomic fluctuations create brief periods of volatility, the underlying structural baseline remains downward.

Furthermore, household spending profiles reveal an acute behavioral cliff once drivers surpass retirement age. While Japanese consumers in the 60–69 cohort often exhibit high absolute transportation expenditures—frequently upgrading to premium vehicles using retirement payouts—the propensity to purchase a new vehicle drops off sharply for cohorts aged 70 and older. At this stage, absolute expenditure on vehicle acquisition falls, replaced instead by a rising dependency on auto repair, maintenance services, and public transport options.

To insulate their balance sheets from this systemic volume decline, domestic automotive manufacturers are forced to pivot toward structural and technological remedies.

5.1 Autonomous Vehicles (AVs) as Senior Lifelines

With approximately 70% of senior citizens expressing an explicit preference to "age in place" within their existing family homes, the preservation of mobility is a critical economic hurdle. Automotive engineering capital is heavily pivoting toward advanced driver-assistance systems (ADAS) and full AV robotaxi architectures. Industry projections estimate that the domestic and global profit pools for AV robotaxis will reach $19 billion by 2030, swelling to $45 billion by 2035, driven significantly by senior citizens who require autonomous transport options as they surrender their personal driving licenses.

5.2 Connected-Car Service Monetization

As the active vehicle fleet contracts in volume, major original equipment manufacturers (OEMs) are attempting to transition from transactional hardware sales to recurring subscription services. By embedding digitally delivered experiences, telematics, and real-time remote diagnostics directly into the vehicle's hardware, manufacturers are working to extract a higher lifetime value from a smaller base of users.

6. The Silver Lining: Pockets of Growth in Healthcare and Infrastructure

While the broader domestic landscape presents severe volume challenges, the demographic wave creates clear opportunities for sectors structured to capture senior spending. As populations age, their consumption propensities pivot predictably. Empirical spending data across advanced economies indicates that the 65+ demographic acts as a powerful demand multiplier for highly specific sectors: Home Improvement & Repair (1.92x vs. the median national consumer), Health Care (1.54x), Reading (1.61x), and Residential Utilities (1.34x).

In Japan, where the old-age dependency ratio leads the world, these multipliers create robust secular growth stories. Traditional consumer retail segments are suffering, but home modification providers, residential medical equipment networks, and senior-focused living developers are seeing steady demand. Because older adults spend a significantly larger portion of their day inside their residences, their households exhibit a 55% higher average electricity consumption footprint than households under the age of 45, acting as a reliable top-line buffer for regulated multi-utilities.

However, analysts warn that even healthcare is not entirely insulated from broader demographic pressures. In a technical note titled "The Healthcare Growth Paradox: Decelerating Momentum," researchers observe that while healthcare remains a strong relative growth category, the absolute rate of population aging in mature economies is set to slow relative to the rapid acceleration of prior decades. For example, joint replacement procedures—such as hip and knee replacements—show a distinct two-phase trajectory. Across the G7, the historical entry of the Baby Boomer generation into peak surgical years drove a powerful 1.9% to 2.1% annual volume surge between 2000 and 2025. Over the next twenty-five years, however, as the senior population plateau stabilizes, this pure demographically driven volume growth is projected to moderate to a CAGR of just 0.6% to 0.7% through 2050.

7. The Corporate Antidote: Geographic Re-Orientation and Capital Flight

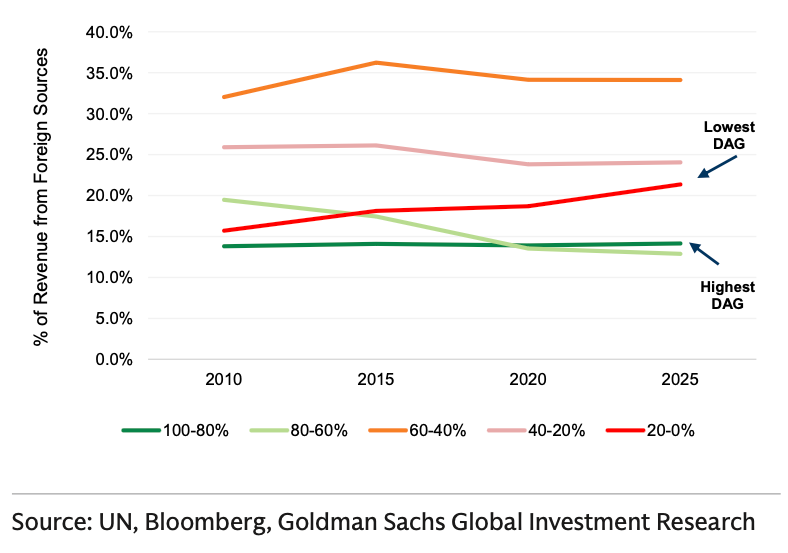

Faced with these structural domestic realities, the ultimate differentiator of corporate survival in Japan has been the execution of outbound geographic expansion. Over the trailing fifteen-year period, equity tracking shows a powerful divergence in corporate behavior dictated entirely by a firm's demographic profile. Companies positioned in segments with the least favorable domestic demographic outlooks have engineered the largest systematic increases in their share of foreign revenue. Conversely, firms operating in demographically insulated niches have maintained flat foreign exposures, comfortably "riding the demographic wave" at home.

This outbound rotation of capital has completely redefined the Japanese corporate footprint. Domestic companies have transformed into sophisticated global asset managers, utilizing dependable domestic cash flows to aggressively acquire high-growth brands and operational infrastructure in younger, demographically favored regions, particularly the United States and India. For global investors evaluating corporate performance, the conclusion is clear: an entity's nominal listing on the Tokyo Stock Exchange is increasingly secondary to the precise geographic distribution of its underlying revenue streams. In a graying world, corporate survival belongs to those who successfully outrun the domestic contraction through strategic international expansion.