SBI Shinsei Bank Breaks Records as 'Fourth Megabank' Strategy Offsets Rate Pressures; MTMP Targets Moved Upward

The integration of SBI Shinsei Bank into the SBI Group has catalyzed a fundamental shift in the institution's trajectory, marking the end of a decades-long focus on public fund repayment and the beginning of its tenure as a high-efficiency market leader. This evolution into a core pillar of the "Next-Gen Finance" vision is now bearing significant financial fruit. By leveraging the SBI Group’s vast ecosystem, the bank has moved beyond traditional structural recovery toward a performance-driven model that diversifies revenue streams at an unprecedented pace for a Japanese lender.

The achievement of a 10.4% Return on Equity (ROE) represents a watershed moment. Reaching double-digit ROE is rare in the Japanese banking sector, and this sector-leading performance validates the group's disruptive strategy. It signals that SBI Shinsei Bank has successfully optimized its capital to generate superior returns, harmonizing the stability of a traditional bank with the high-velocity agility of a fintech ecosystem.

Key Strategic and Financial Highlights

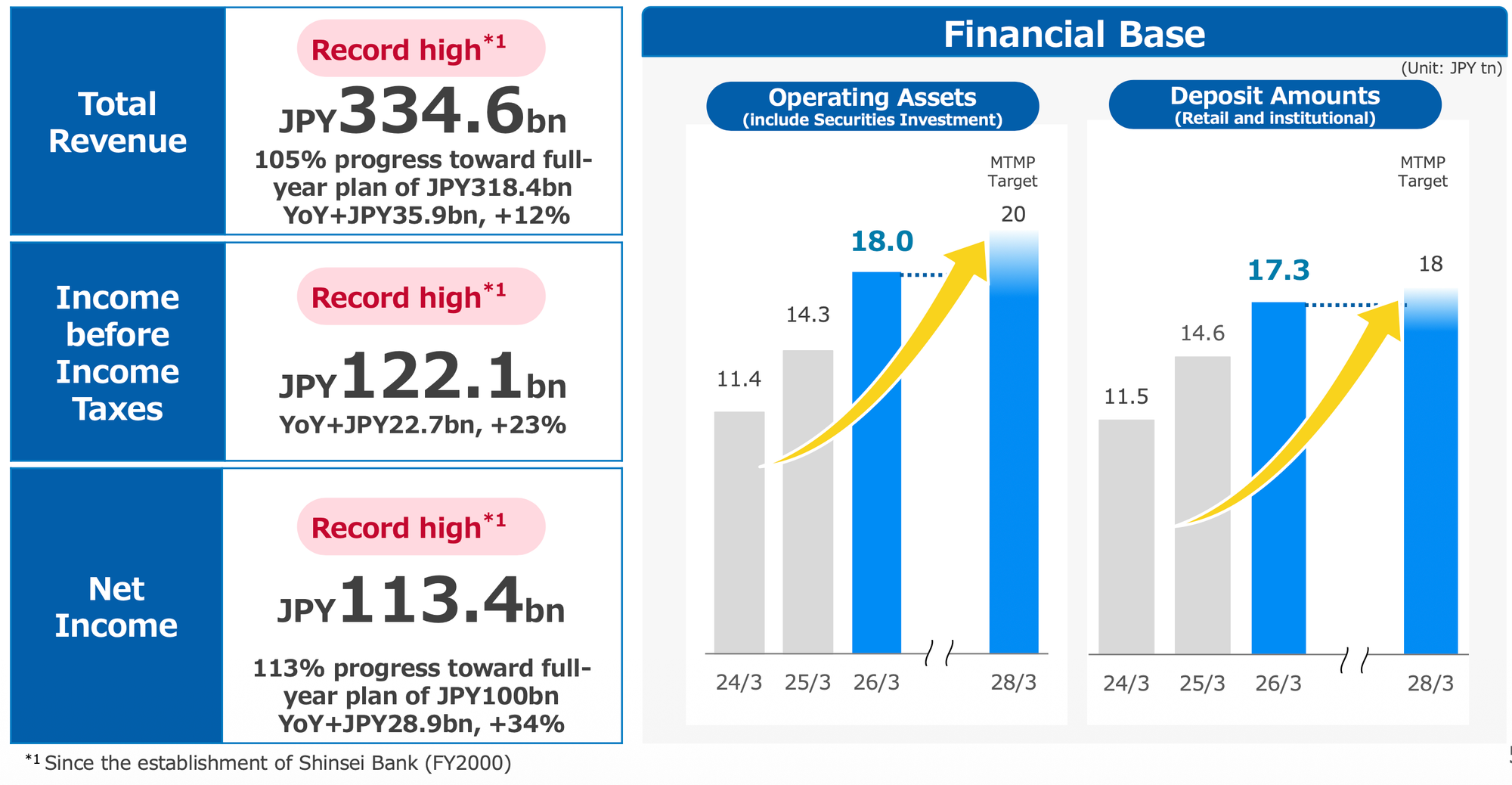

- Record-Breaking Financials: The group achieved record highs in Total Revenue, Income before Income Taxes, and Net Income since the bank's establishment in FY2000.

- Structural Evolution: Following the full repayment of public funds, the bank successfully relisted on the Tokyo Stock Exchange Prime Market, restoring its status as a premier public entity.

- Operating Asset Expansion: Robust growth in Operating Assets (including loans, leasing, and securities) to JPY 18.0tn, supported by a deposit base of JPY 17.3tn.

- Enhanced Capital Efficiency: A significant jump in RORA (Risk-Adjusted Return on Assets) from 0.96% to 1.23% year-on-year, underscoring a shift toward higher-margin business lines.

The underlying strength of these record-breaking figures becomes even more apparent when analyzing the bank's core profitability metrics and its resilience against a shifting macroeconomic backdrop.

1. Financial Performance Review: Analyzing the Recurring Growth Engine

The fiscal year 2025 results reveal a bank in peak health, where profitability is driven by sustainable organic expansion rather than accounting anomalies. While the nominal growth in Income before Income Taxes is impressive, the "underlying" growth story is even more compelling for institutional investors.

Analytical Deep Dive: Yield and Spread Expansion

A primary engine of this profitability is the 10-basis-point expansion in the interest rate spread, which rose to 0.55% by March 2026. This expansion reflects a disciplined "Strengthening Profitability" strategy focused on active yield improvement and volume growth in core lending. Despite this aggressive growth, the bank maintained a consolidated capital adequacy ratio of 9.68%, comfortably exceeding its 8.5% target.

Dividend Policy

Confident in this recurring earnings momentum, management has revised the dividend policy upward. The dividend forecast increased from JPY 34 to JPY 42 per share. This 23.5% hike signals a robust commitment to shareholder returns following the bank’s return to the Prime Market and aligns with the bank's goal to scale dividends in lockstep with net income.

This financial momentum is fundamentally powered by the "Open Alliance" model, a core differentiator that separates SBI Shinsei from the "closed" ecosystems of Japan's traditional "Big Three" megabanks.

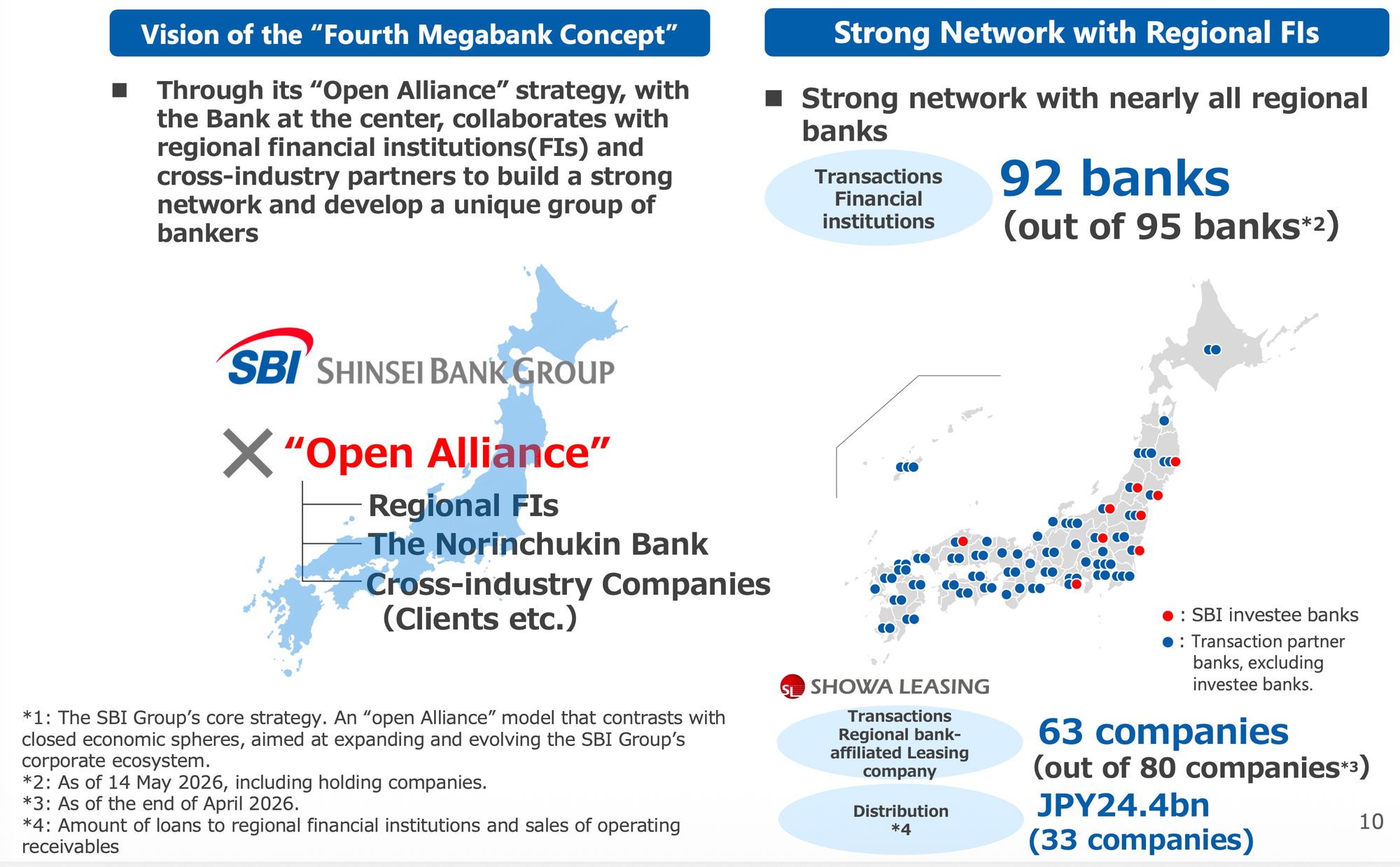

2. The "Fourth Megabank Concept" and Regional Collaboration

The "Fourth Megabank Concept" positions SBI Shinsei Bank as a disruptive hub in a nationwide network designed to revitalize regional economies. Unlike traditional competitors, the bank employs an "Open Alliance" strategy, offering its infrastructure and sophisticated products to regional financial institutions (FIs) rather than competing for their local turf.

Network Evaluation

The scale of this "Open Alliance" is now nearly exhaustive, encompassing 92 partner banks (out of 95 in Japan) and 63 regional bank-affiliated leasing companies. This network provides the SBI Group with a massive, indirect corporate footprint across all of Japan's prefectures.

The Three Collaboration Pillars

- Product Supply: The bank provides sophisticated financing solutions that regional FIs cannot easily originate alone. Recent successes include a JPY 15.0bn syndicated loan for NYK Line involving six regional banks and a JPY 2.0bn hotel development loan for Sun Frontier Hotel Management in Akita.

- Regional Industry Creation: Through Shinsei Business Succession, the bank provides equity capital to solve the SME "successor crisis," preventing the hollowing out of local industries while participating in large-scale local infrastructure and energy projects.

- Management Support: Perhaps the most disruptive element is the provision of a cloud-based, API-enabled "Next-Generation Banking System." This allows regional banks to escape "vendor lock-in" and high fixed costs. Notably, The Sendai Bank, Kirayaka Bank, and The Towa Bank have already announced the adoption of this platform.

While the regional network provides a massive corporate funnel, the bank’s retail innovation—specifically its digital-first deposit strategy—provides the low-cost funding base necessary to fuel these regional assets.

3. Retail Banking and Housing Loan Growth Drivers

The bank’s retail division has successfully transitioned into a high-velocity, digital-first growth engine. By seamlessly integrating banking and investment through the SBI Group's infrastructure, the bank is maximizing Customer Lifetime Value (LTV) and capturing market share from traditional retail incumbents.

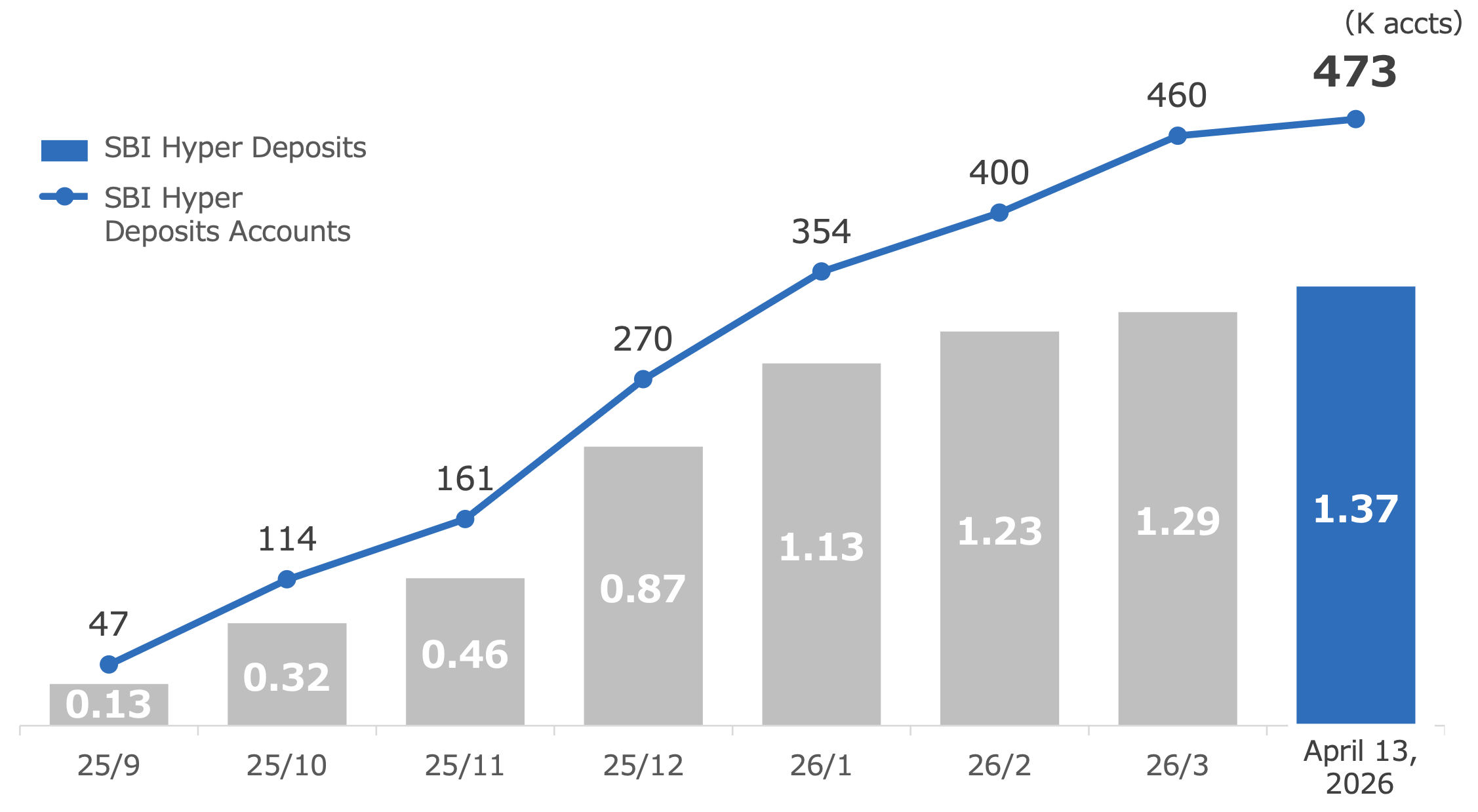

The "SBI Hyper Deposits" Velocity

The launch of "SBI Hyper Deposits" has redefined the bank's funding base. By April 13, 2026, balances had surged to JPY 1.37tn with over 473,000 accounts. The velocity of this growth—reaching these levels within approximately six months—demonstrates a "virtuous cycle" where linked accounts with SBI SECURITIES encourage a "shift from savings to investment." Crucially, 65% of these balances are new fund inflows, rather than internal transfers.

Housing Loan Operational Efficiency

Housing loans have emerged as a high-capital-efficiency pillar, with balances reaching JPY 2.3tn (up JPY 1.1tn since March 2024).

- AI-Driven Productivity: The implementation of AI scoring has revolutionized the back office. The bank now processes 4.5x more volume than in early 2024.

- Human Capital Optimization: Most impressively, this volume surge is managed by just 8 approvers, compared to the 14 reviewers previously required—a key metric for operational leverage.

Asset Management & AUM

Total retail Assets Under Management (AUM) expanded to JPY 2.7tn, a JPY 1.3tn increase since March 2024. This growth is anchored by the "SBI Wrap x SBI Shinsei Bank" service, which reached JPY 102.0bn. The synergy with SBI SECURITIES has been the primary catalyst, as the bank captures the wealth management needs of an expanding customer base that now totals 4.33 million accounts.

The success of these retail and regional initiatives provides a stable foundation for the bank’s entry into the next frontier: the commercialization of digital finance.

4. Future Outlook: Next-Gen Finance and MTMP Acceleration

SBI Shinsei Bank is moving aggressively into the commercialization stage of blockchain technology, distancing itself from traditional banking peers. By leading the development of digital currency ecosystems, the bank aims to redefine settlement and payment infrastructure in Japan.

Digital Innovation Roadmap:

- JPYSC: Preparations are underway for the launch of a Japanese Yen-denominated stablecoin issued by SBI Shinsei Trust Bank.

- DCJPY: The bank has completed successful proofs-of-concept for Delivery Versus Payment (DVP) settlements using tokenized deposits, aiming to link blockchain efficiency directly to its core deposit base.

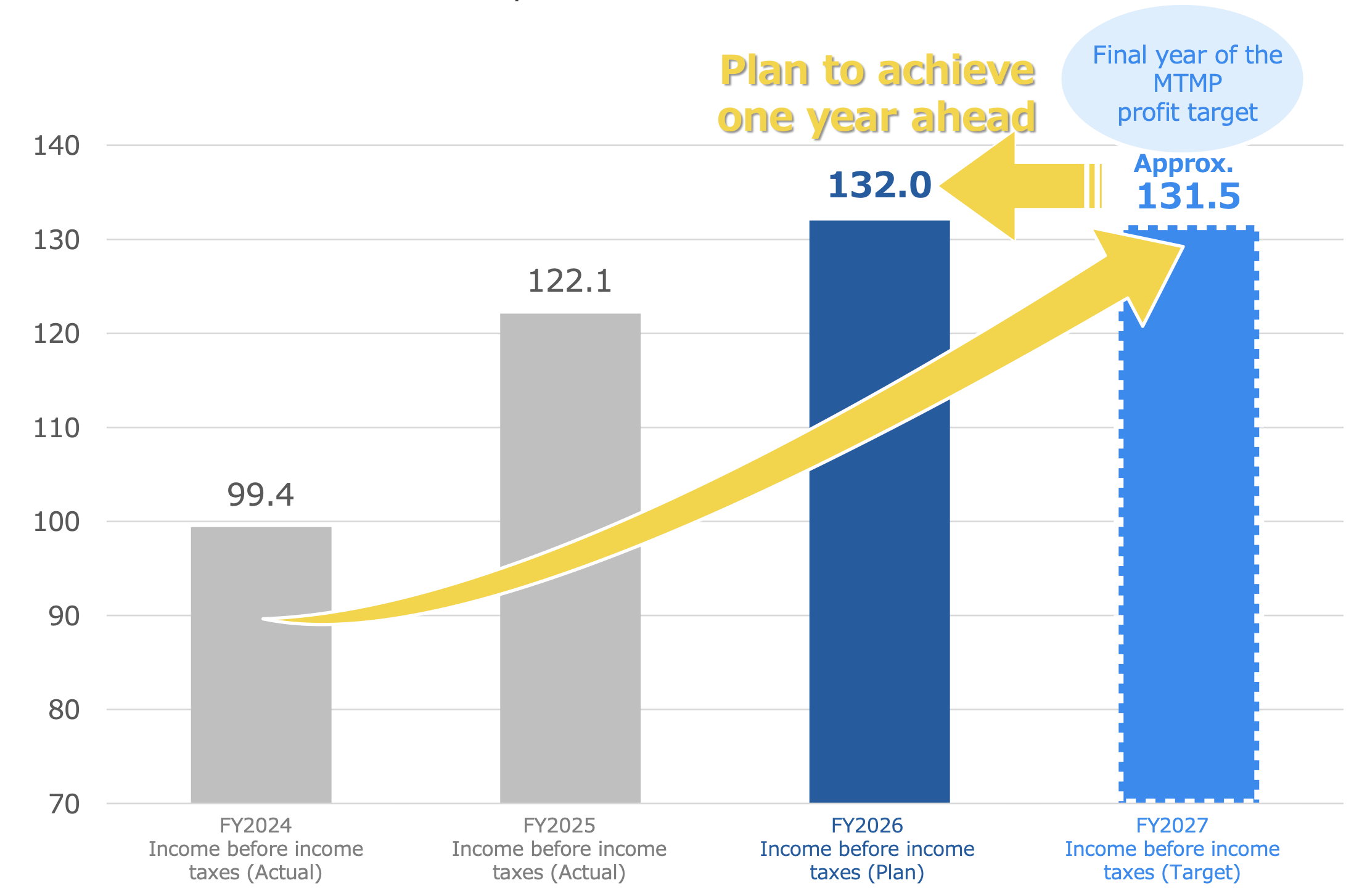

Strategic Goal Acceleration

The bank’s most significant forward-looking announcement is the acceleration of its Medium-Term Management Plan (MTMP). Originally, the bank targeted an Income before Income Taxes of JPY 131.5bn for FY2027. Given current momentum, management now expects to hit JPY 132.0bn in FY2026—one full year ahead of schedule.

This acceleration is supported by favorable macroeconomic tailwinds. The bank's FY2027 targets assume a BOJ policy rate of 0.75% (up from 0.50% in FY2025) and a 1.50% 10-year JGB yield. As interest rates "normalize" in Japan, SBI Shinsei's yield-sensitive "Operating Assets" are positioned to capture significant margin upside.

Final Summary

SBI Shinsei Bank has completed a historic turnaround, emerging as a powerhouse of profitability within the SBI Group. By hitting record profits, scaling the "Fourth Megabank" network with specific regional adoptions, and pioneering digital currency commercialization, the bank has solidified its position as the vanguard of "Next-Generation Finance." With its medium-term targets now within reach a year early, SBI Shinsei is not just participating in the Japanese banking sector—it is redefining its future.