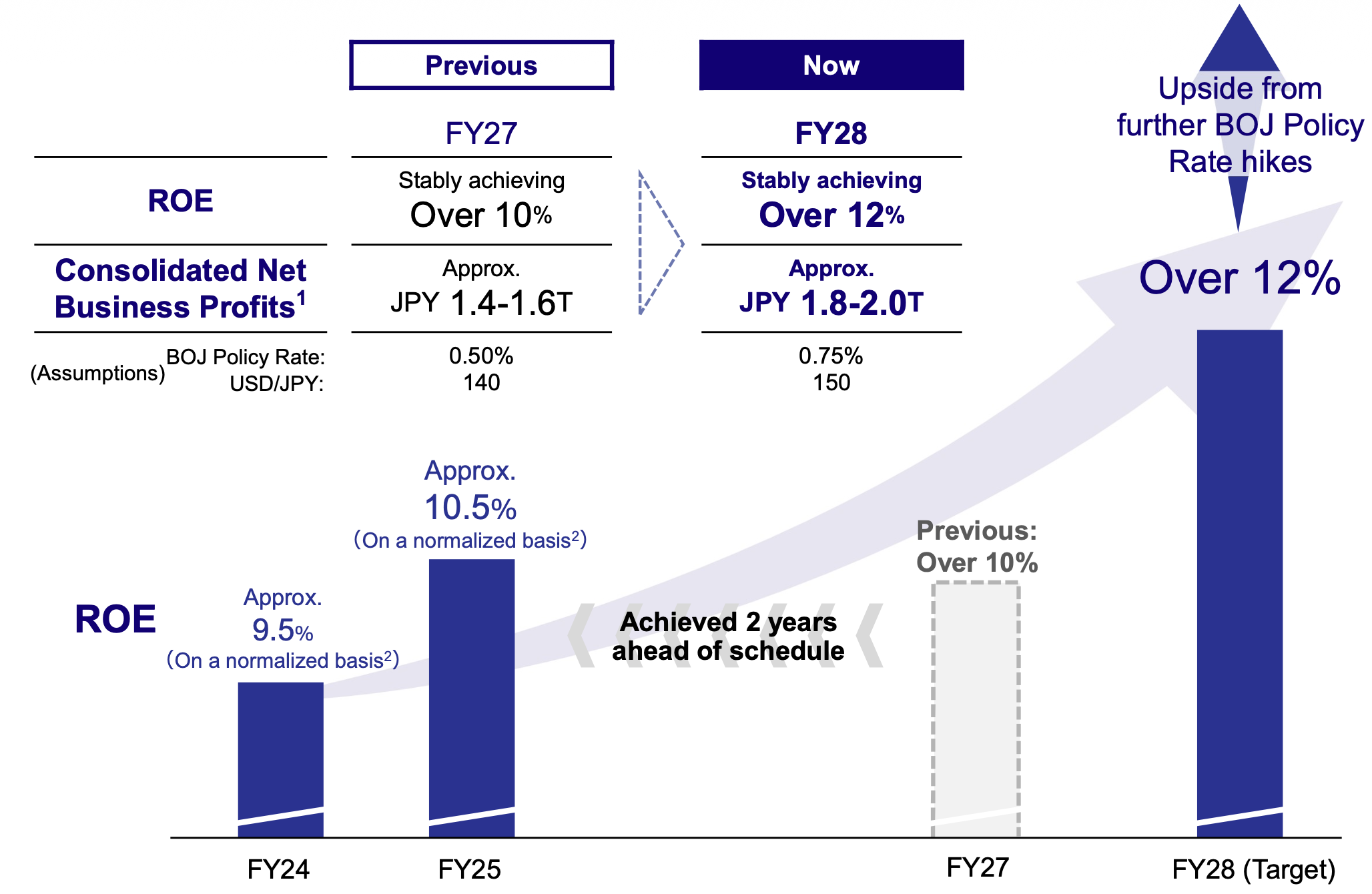

Mizuho Hits Targets Early; Sets Aggressive FY28 ROE Goal After Record Profits

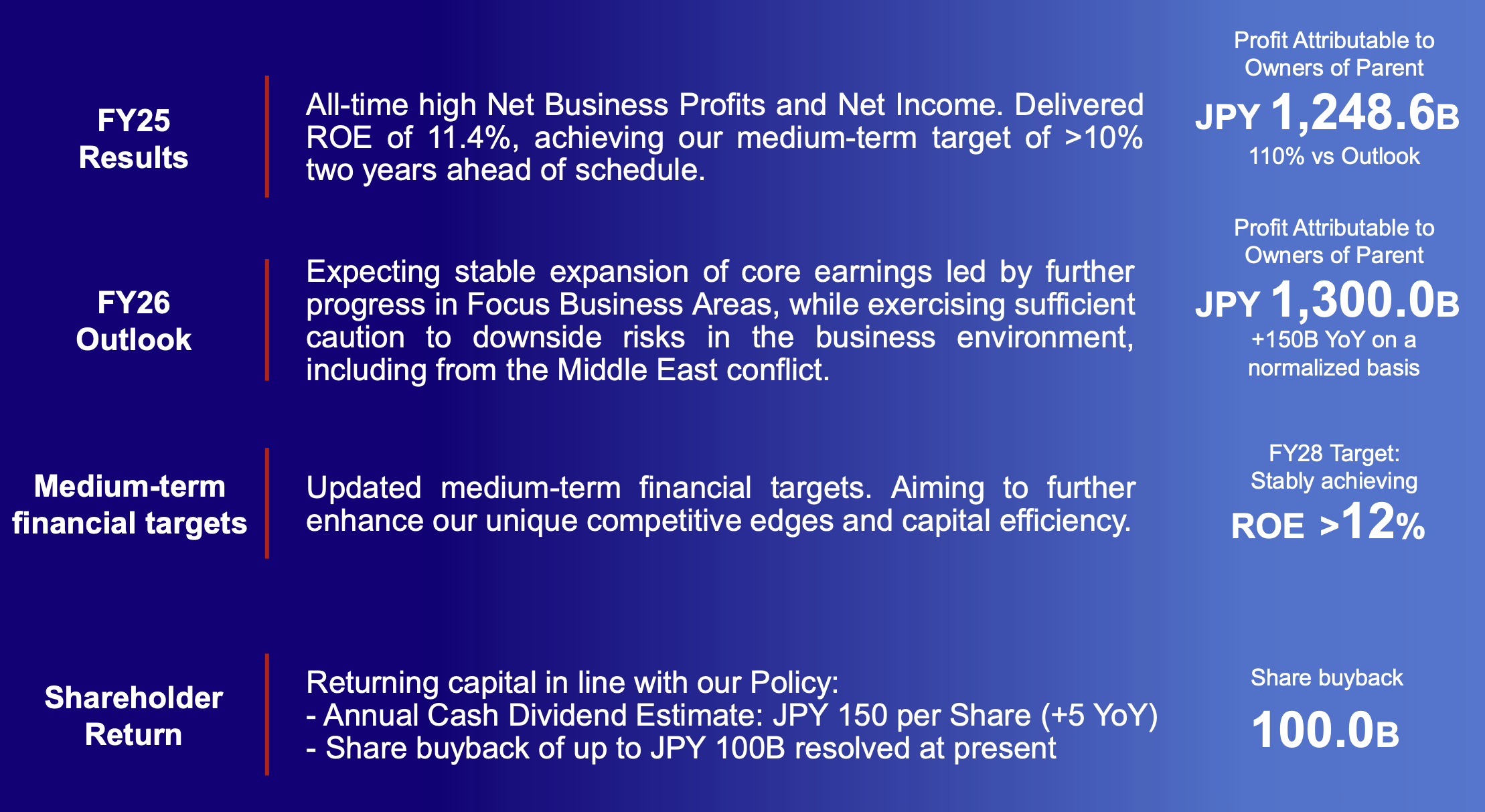

Mizuho Financial Group has shattered its historical earnings records for the fiscal year ending March 2026 (FY25), completing a transformation from its "legacy of challenge" to what management defines as a "circle of rich fruition." By delivering a return on equity (ROE) of 11.4%, the group reached its medium-term profitability target of over 10% two years ahead of schedule. In a shifting Japanese macroeconomic landscape, Mizuho’s early success signals a fundamental reset of its capital efficiency, allowing the bank to front-load shareholder returns while setting a new, more ambitious profit ceiling for the end of the decade.

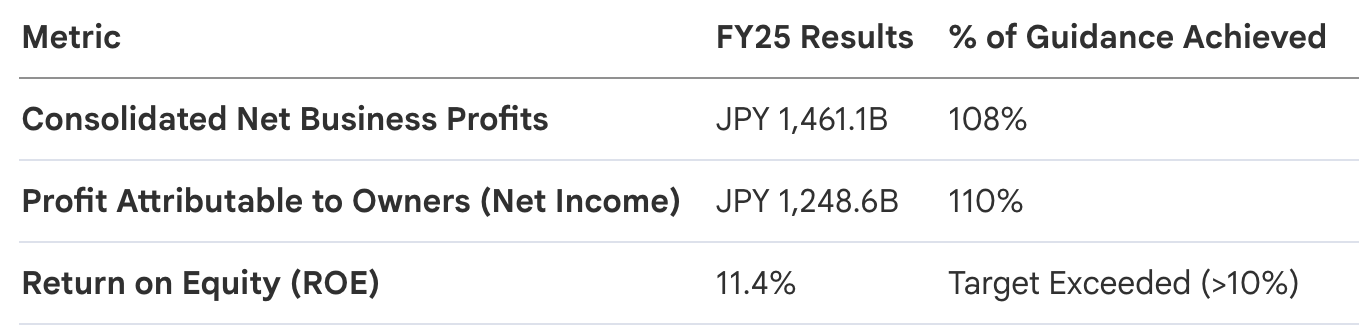

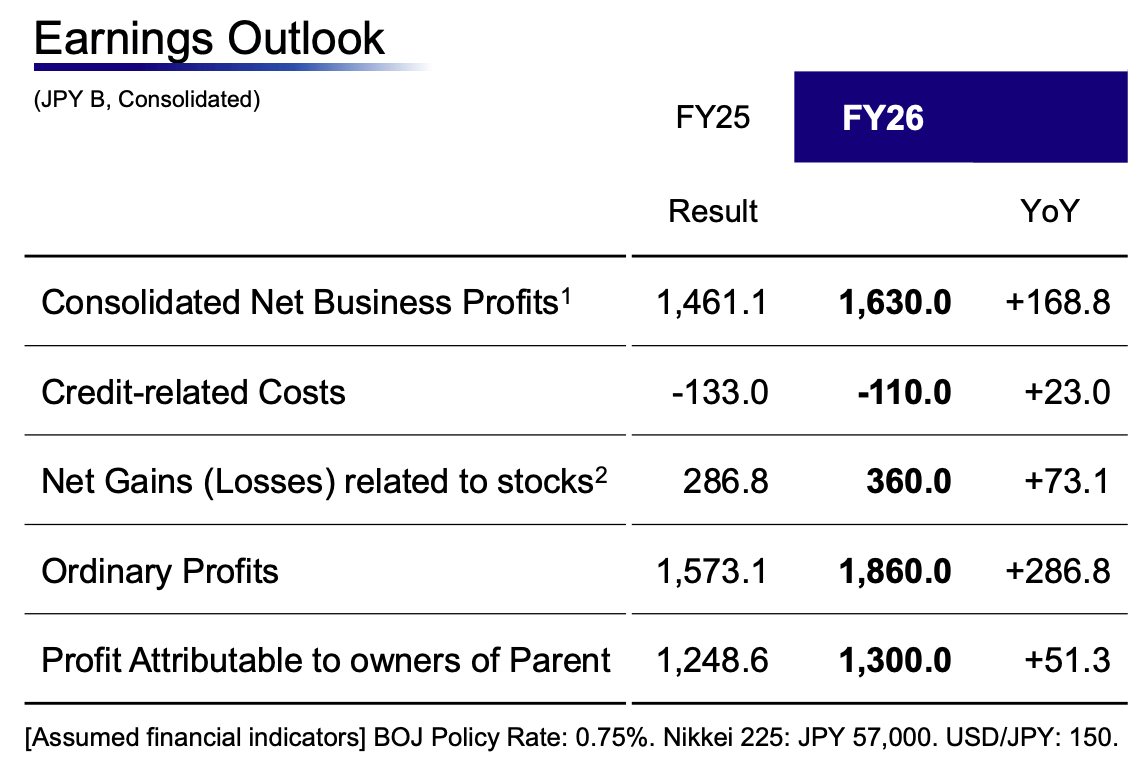

The group reported all-time highs with Consolidated Net Business Profits of JPY 1,461.1 billion and Net Income of JPY 1,248.6 billion. This performance overshoots the market’s perception of Mizuho as a laggard in capital efficiency, moving it toward a leadership position as Japanese interest rates begin their long-awaited ascent. Management is now pivoting toward an "aggressive" FY28 target range of JPY 1.8–2.0 trillion in net business profits.

1. FY25 Financial Performance: Breaking the Record

Mizuho’s FY25 results were underpinned by an integrated group model that successfully captured high-margin non-interest business, particularly within investment banking and real estate. The group demonstrated significant operating leverage, driving the expense ratio down to 59.4%—successfully breaking the 60% threshold while maintaining strategic investment levels.

Analysts view the JPY 1.25 trillion net income as a "boosted" headline, as approximately JPY 100 billion was driven by one-off factors, including aggressive sales of deemed shareholdings and favorable tax expenses. Stripping these out, Mizuho’s "normalized" profit level stands at JPY 1,150 billion. This underlying base is the true benchmark for the bank's core earning power heading into the next fiscal year.

2. Forward Guidance: The FY26 Outlook and "Low-Balled" Growth

For FY26, Mizuho has issued a net income forecast of JPY 1,300.0 billion. While the headline year-on-year increase of JPY 50 billion appears conservative, the figure is actually a "low-balled" estimate. The bank’s projections assume a modest Bank of Japan (BOJ) policy rate of 0.75% and deliberately exclude potential upside from further rate hikes.

On a normalized basis, the bank expects approximately JPY 150 billion in year-on-year profit growth. This "normalized" trajectory is the primary metric of success, reflecting core business expansion in a rising rate environment rather than non-recurring gains.

To de-risk against external volatility, Mizuho has proactively padded its defenses. The bank recorded JPY 133.0 billion in credit-related costs, including additional forward-looking provisions specifically tied to the Middle East conflict. This strategic buffer ensures the group remains "supple in the face of change" even if global geopolitical conditions deteriorate.

3. Operational Deep-Dive: Tactical Bond Losses and Segment Divergence

A granular look at the operations reveals a bank aggressively cleaning its house to prepare for higher interest rates. Notably, the "Banking" segment realized JPY 150.0 billion in losses during the year—a proactive move to offload lower-yielding bond portfolios and improve future flexibility.

- Retail & Business Banking (RBC): Net business profits surged as deposit-loan yield spreads widened following domestic rate hikes. However, net income saw a slight decline due to the non-recurrence of prior-year asset sales and increased credit provisions.

- Corporate & Investment Banking (CIBC): Net profit was "substantially boosted" by gains from the sale of deemed holdings. While loan spreads in this segment saw a "temporary move" downward due to specific large individual names, management insists the broader trajectory for corporate lending spreads remains upward.

- Global CIB & Sales and Trading: Performance remained steady, though net income dipped slightly following higher credit costs associated with "single-name" factors.

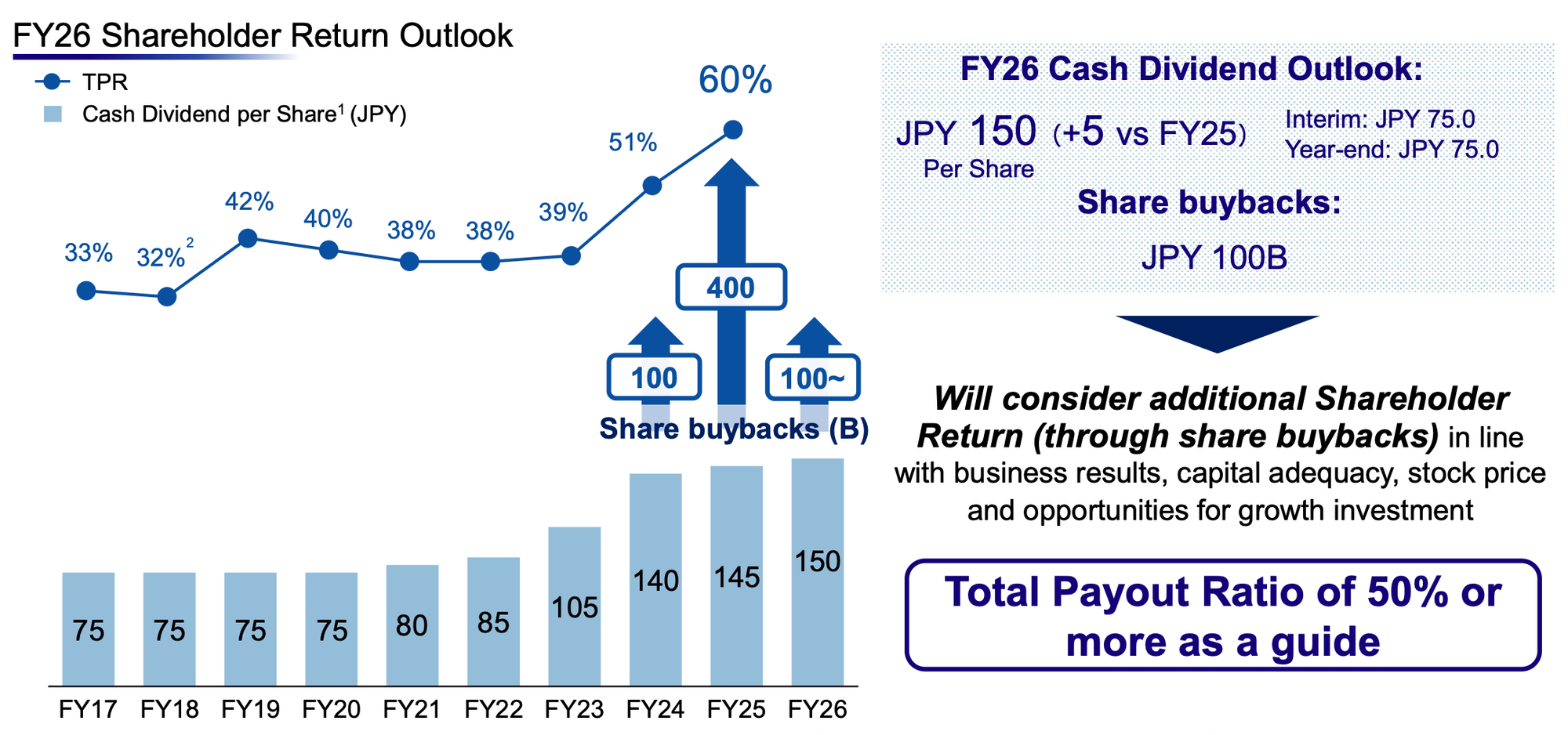

4. Capital Policy: CET1 Ratios and Aggressive Shareholder Returns

Mizuho’s capital position remains robust, though its Common Equity Tier 1 (CET1) ratio declined slightly to 9.9% (from 10.3%). This dip was a calculated result of Risk-Weighted Asset (RWA) growth as the bank expanded its lending book to meet surging domestic financing demand.

Mizuho is leveraging its early target achievement to pivot toward a high-payout strategy, committing to a Total Payout Ratio of 50% or more.

- Dividends: Estimated annual cash dividend of JPY 150 (+JPY 5 YoY).

- Buybacks: Resolved share buyback program of up to JPY 100 billion.

- Cross-Shareholdings: The bank is accelerating its exit from corporate ties, targeting a JPY 350 billion reduction in the three-year period ending March 2028. It has already beaten its initial outlook by reducing JPY 200 billion in deemed shareholdings in FY25 alone.

5. Closing: The "Circle of Fruition" and the JPY 2 Trillion Target

Mizuho’s record-breaking year represents more than just a financial milestone; it is the realization of the group's "Purpose" to innovate for a sustainable future. In collaboration with the Tokyo University of the Arts, the bank visualized this transition through the artwork "Circle of Fruition," symbolizing a firm core that breathes life into society.

With the original medium-term goals in the rearview mirror, Mizuho has set its sights on an "aggressive" FY28 ROE target of over 12%. By aiming for JPY 1.8–2.0 trillion in Net Business Profits, Mizuho is positioning itself as the primary beneficiary of Japan’s structural economic shift, leveraging its record earnings to co-create a more abundant and sustainable social landscape.