Rakuten Bank Hits Record Profits as Rate Hikes and Ecosystem Synergy Fuel FY2025 Surge

In an environment defined by rising interest rates, Rakuten Bank emerged as a primary beneficiary, reporting record-high profits that underscore the potency of its digital-first model. The bank’s ability to capitalize on the BOJ’s policy rate hike—reaching 0.75% by December 2025—while simultaneously deepening its integration within the massive Rakuten Ecosystem, has propelled the institution to new heights of profitability and capital efficiency.

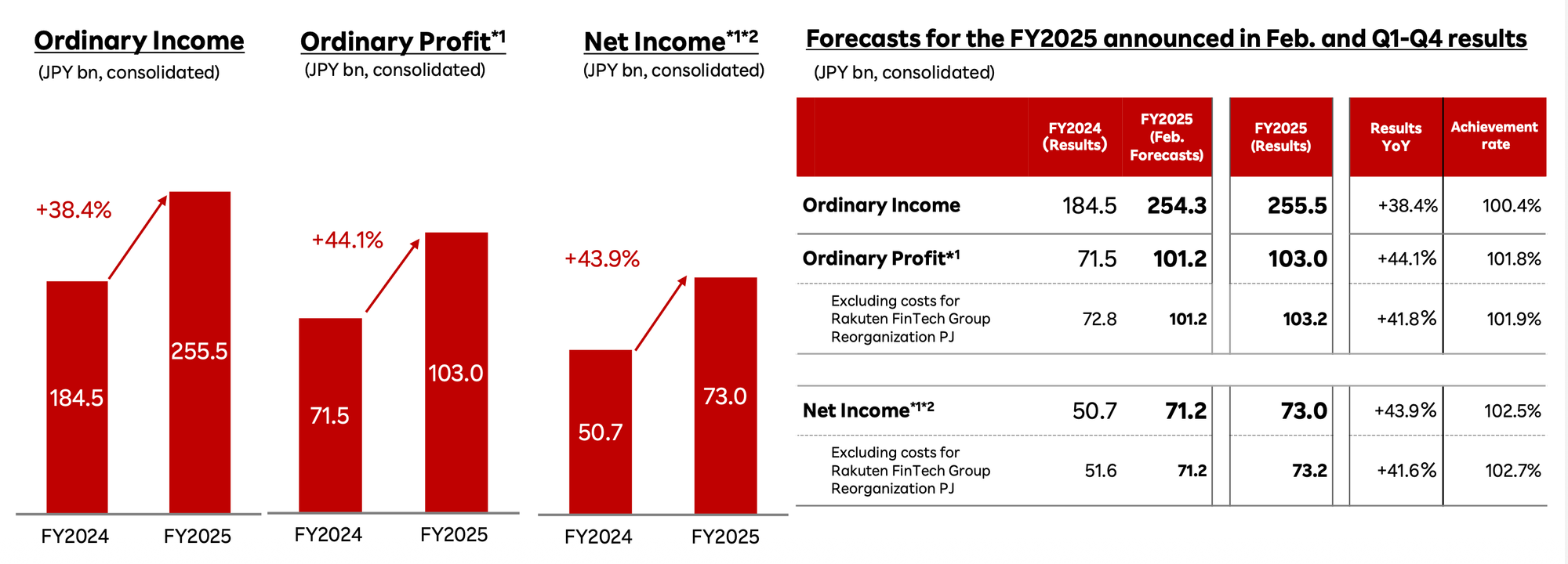

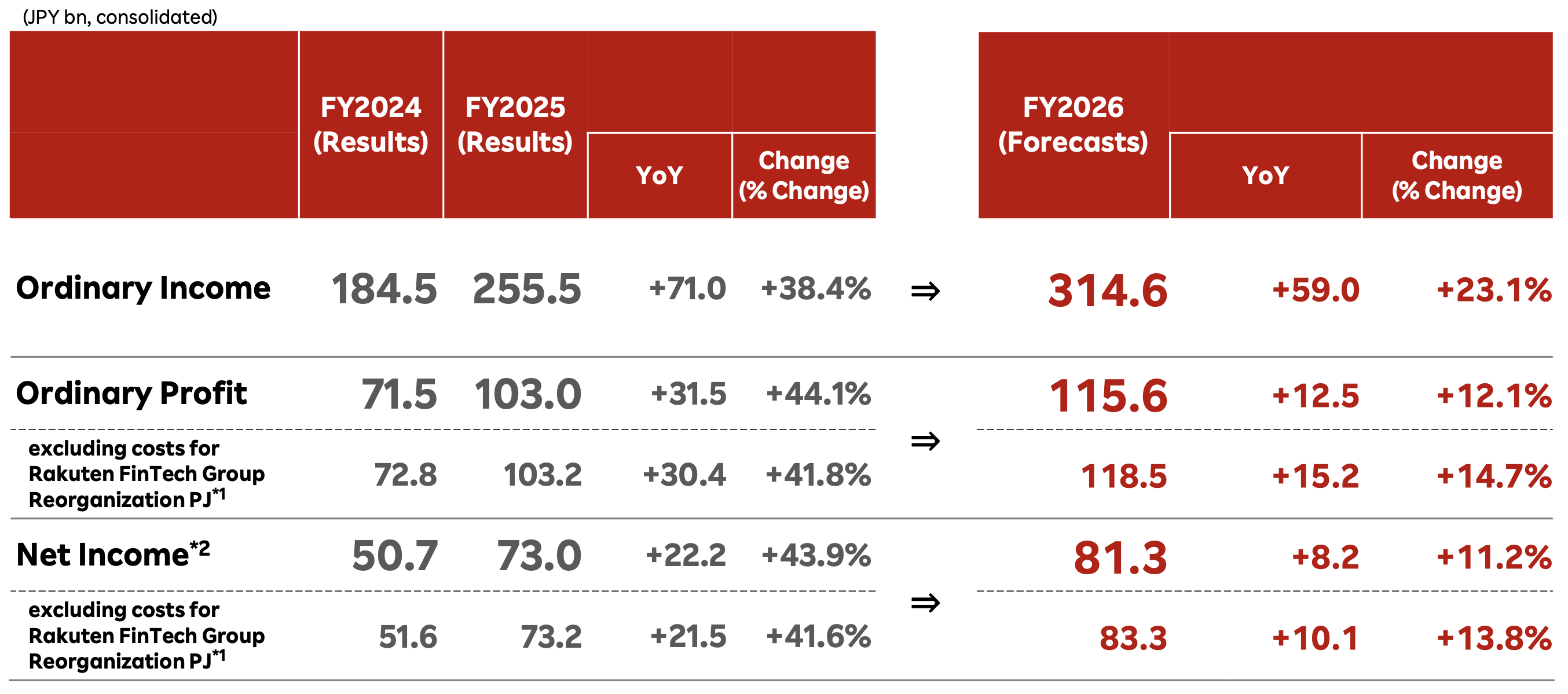

The consolidated operating results for the period reflect a surge across all primary earnings categories, with ordinary profit crossing the ¥100 billion threshold for the first time. This performance was driven by an aggressive expansion in interest income and continued improvements in management efficiency.

The bank’s profitability indicators reflect exceptional capital efficiency, with Return on Own Capital (ROE) rising significantly to 21.7%, up from 18.0% the previous year. This high ROE demonstrates the bank’s ability to generate substantial returns on its equity base even as it continues to build capital. Meanwhile, the Ordinary Profit to Total Assets ratio improved to 0.6%, highlighting disciplined balance sheet management in a shifting macroeconomic landscape.

This record-breaking financial performance was fueled by specific operational drivers that expanded the bank's customer base and deepened its "lock-in" within the broader Rakuten Group.

1. Operational KPIs: The Engine of Growth

At the heart of Rakuten Bank’s success is its "Main Account" strategy. By positioning itself as the primary settlement hub for the Rakuten Ecosystem's 100 million+ members, the bank creates a self-reinforcing cycle of deposit acquisition. The ecosystem acts as a low-cost acquisition funnel, allowing the bank to scale at a pace that traditional competitors struggle to match.

The bank’s key performance indicators (KPIs) show significant momentum:

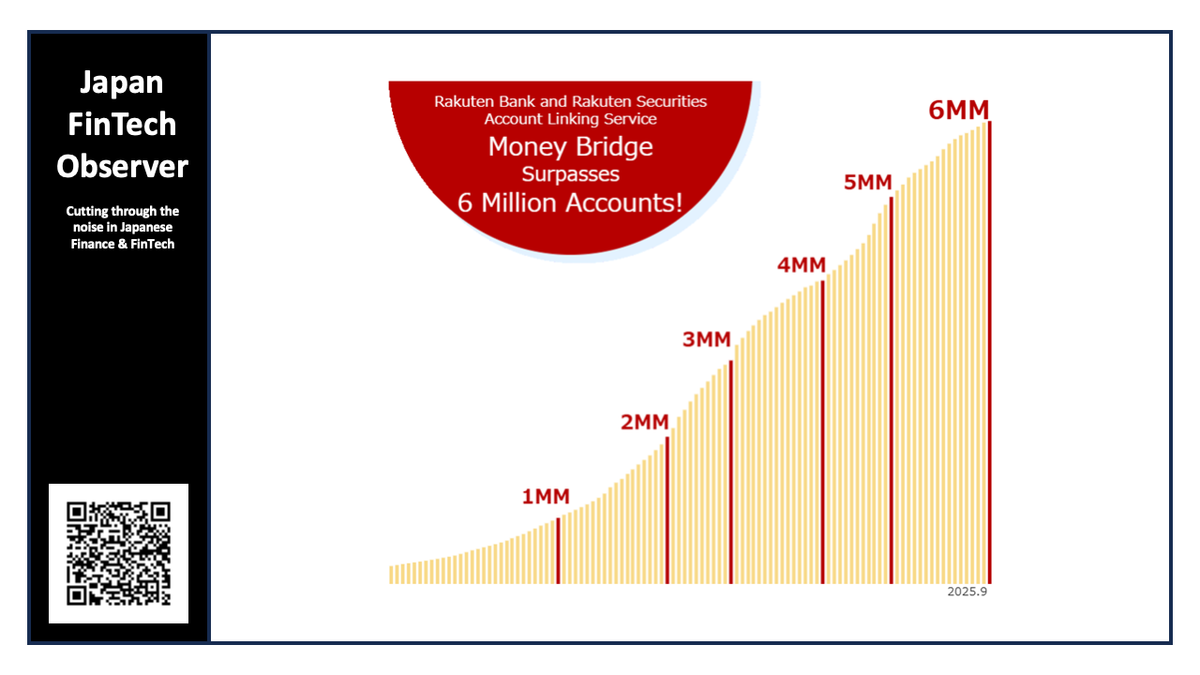

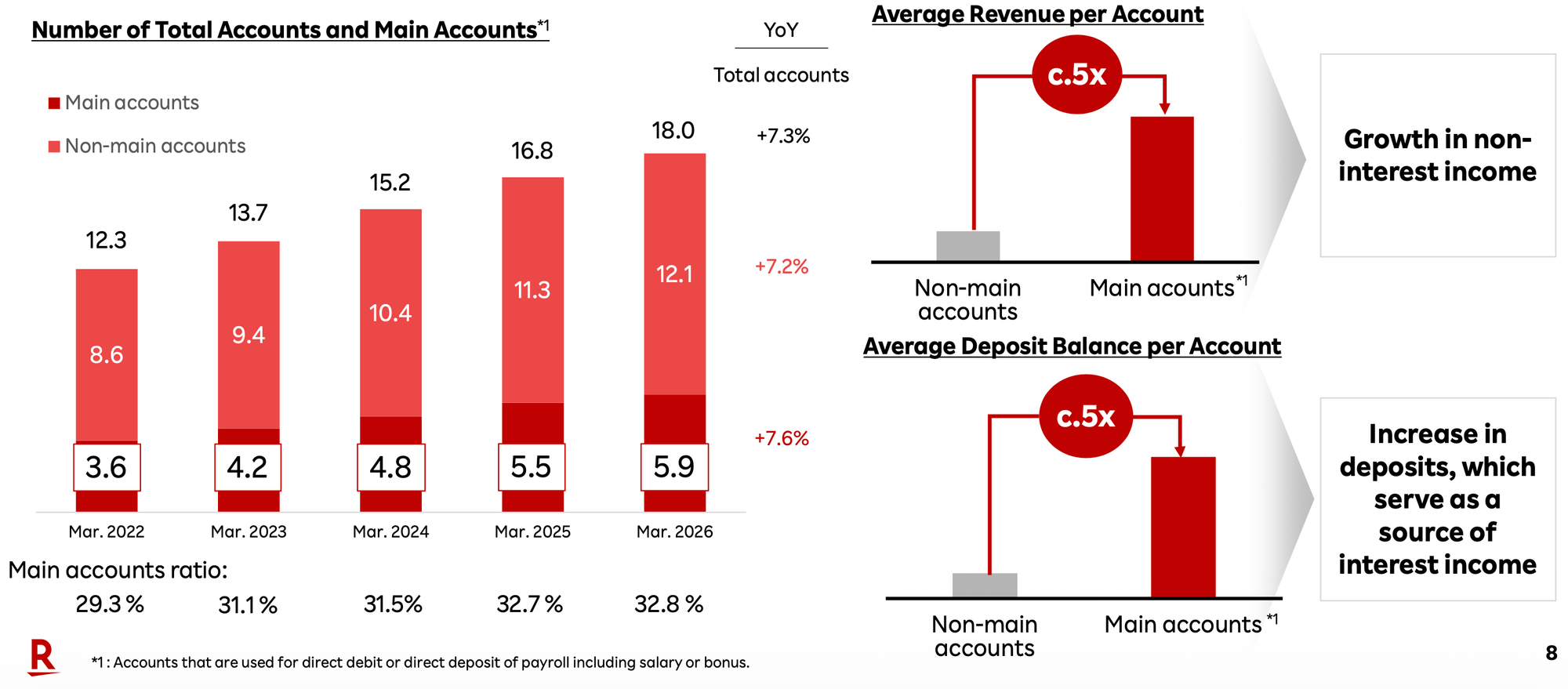

- Total Number of Accounts: Surpassed the 18 million mark to reach 18.07 million as of March 31, 2026, maintaining a growth pace of over 1 million accounts annually.

- Deposit Balance: Reached ¥12.96 trillion (non-consolidated), a robust 12.9% YoY increase. This growth is particularly impressive given the downward pressure from the New NISA annual investment quota reset during the January-March period, which typically drives funds out of deposits and into securities.

- Main Account Ratio: Now stands at 32.8% (5.9 million accounts). This metric is crucial; main accounts represent users who direct-deposit salaries or connect multiple direct debits, creating high "stickiness."

Technical enhancements and the "Mobile hook" have been pivotal to this acceleration. In January 2026, the bank launched a partnership for bank agency services with Rakuten Mobile, introducing the "Rakuten Mobile x Rakuten Bank Bonus Interest Rate." This service, combined with the December 2025 launch of the "Smartphone ATM" service, incentivizes ecosystem loyalty. Furthermore, UI/UX renovations now allow users to track their "Bonus Interest" status directly within the app, while the Rakuten Card app now displays Rakuten Bank balances to promote account switching and mitigate the risk of uncollected usage charges.

This increased scale provided the bank with a massive pool of low-cost deposits, which it strategically deployed into a diversifying array of interest-bearing assets.

2. Interest Income and Asset Allocation Strategy

Rakuten Bank’s asset management strategy has successfully transitioned into a "world with interest rates." The bank has shifted its focus toward "middle-risk/middle-return" assets while reaping a windfall from the BOJ’s policy shifts. Reflecting its sensitivity to macro moves, the bank’s simple simulation indicates that for every 25bp increase in the policy rate, there is a +¥14.5 billion impact on annualized net interest income (based on the March 2026 balance sheet).

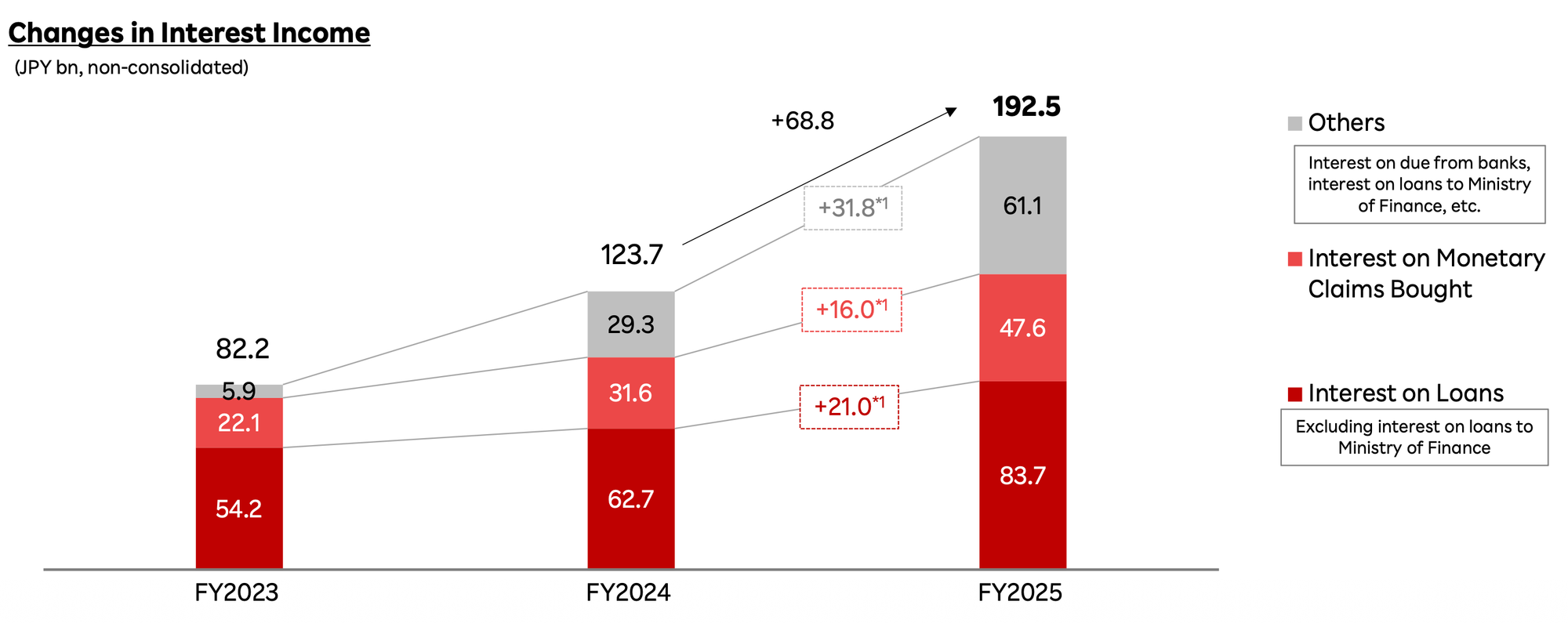

The ¥69.4 billion increase in consolidated interest income (totaling ¥197.6 billion) was driven by three categories:

- Interest on Loans and Discounts (+¥21.0 billion): Driven by quantitative expansion in risk-diversified segments.

- Interest on Monetary Claims Bought (+¥16.0 billion): Derived from securitized assets and Rakuten Card receivables.

- Investment Yields from BOJ Rate Hikes (+¥31.8 billion): Reflected in "Others," this includes yields on surplus fund operations and deposits with the BOJ.

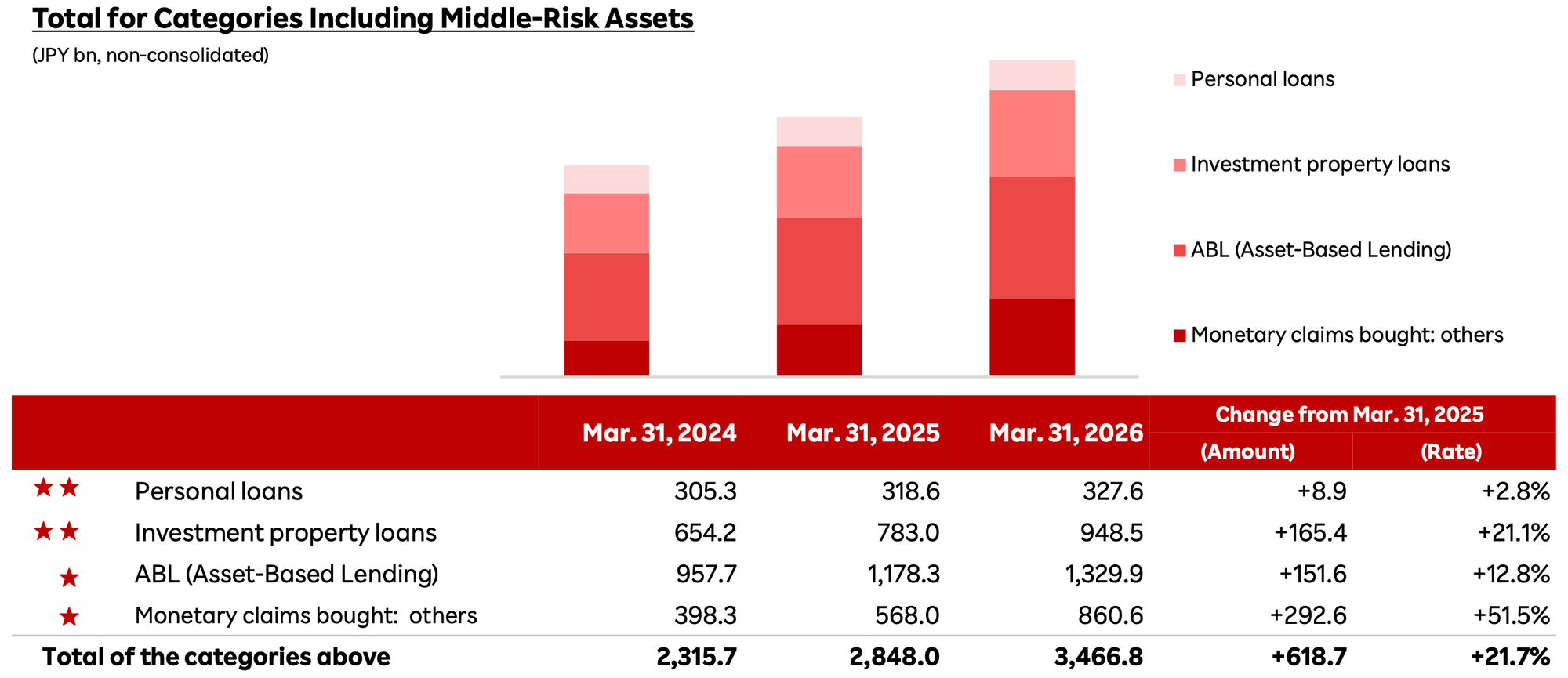

The expansion of middle-risk assets has been aggressive and diversified. Notable successes include the "Rakuten Bank Securities-Backed Loan," which surpassed ¥10 billion in balance within just four months of its June 2025 launch, and the "Rakuten Bank Reverse Mortgage (credit-line type)." The bank has also begun trials in mezzanine and equity portions of securitized projects to enhance spreads.

This aggressive asset growth has been managed with a keen eye on operational efficiency and the bank's underlying credit health.

3. Financial Health: Efficiency, Credit Costs, and Capital

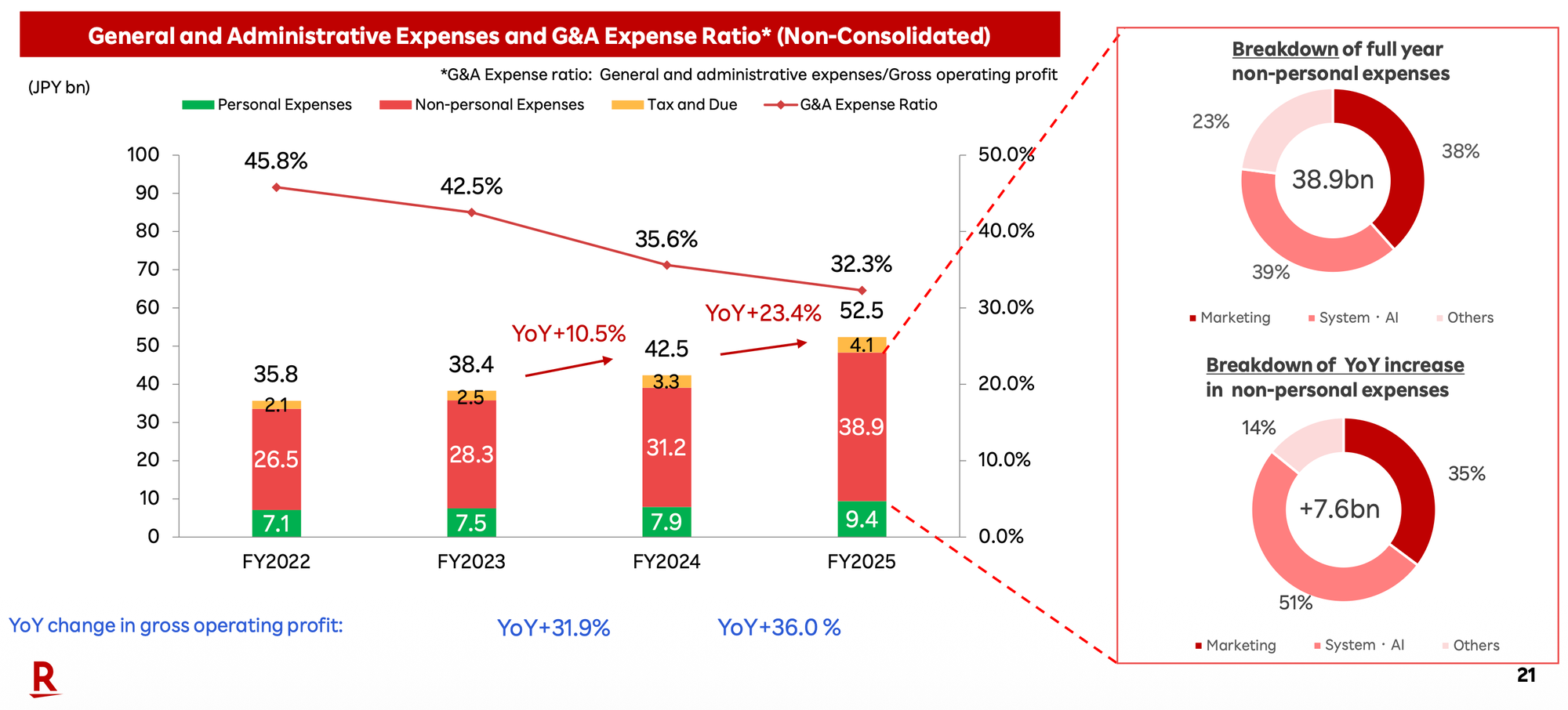

A defining characteristic of Rakuten Bank is its ability to maintain a lean operation while investing for the future. The bank’s Overhead Ratio (OHR) improved to 32.3%, a 3.2 percentage point decrease from the previous year. This efficiency was achieved despite a 23.4% increase in non-consolidated G&A expenses to ¥52.5 billion.

Management strategically directed this spending toward GPU servers and AI integration, specifically intended to accelerate data integration. This technological foundation is designed to lower overall funding costs across the FinTech business by optimizing resource allocation and customer targeting.

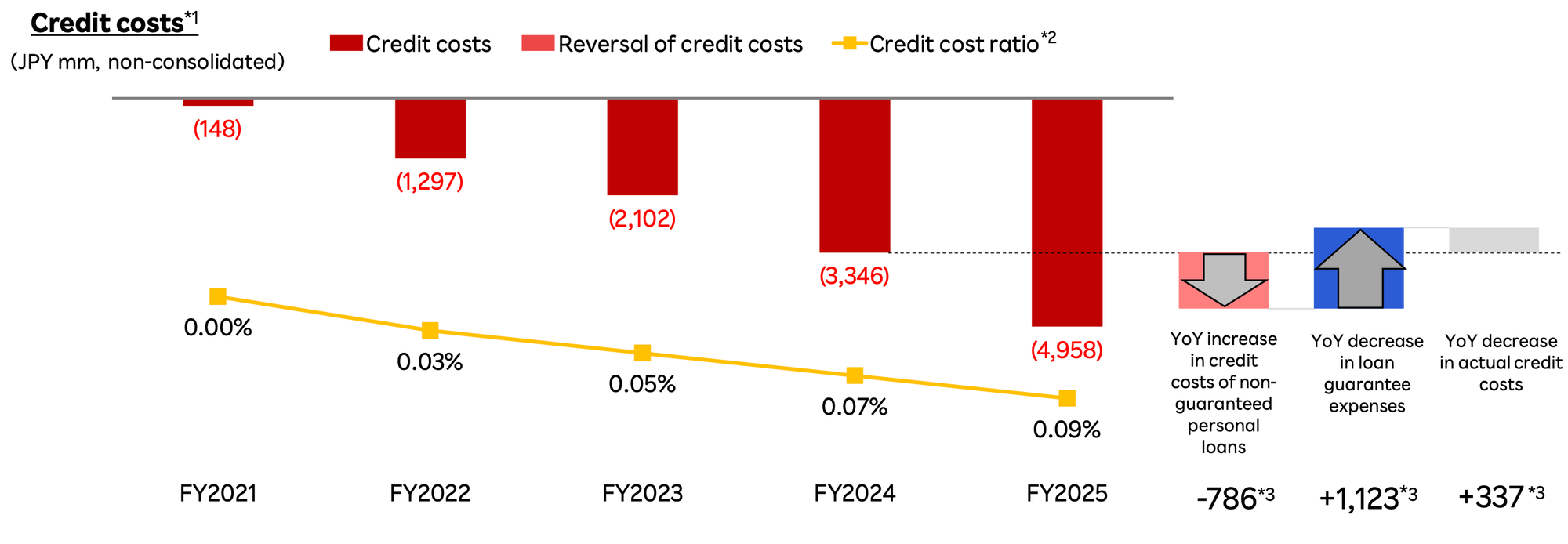

The credit cost profile remains healthy. While the absolute amount of credit costs increased to ¥4.9 billion—largely due to the assessment of specific securitization projects—the "substantial credit cost" (the sum of credit costs and payment guarantee fees) actually decreased by ¥337 million YoY. This indicates that as the bank shifts more lending in-house, its risk management remains superior to external guarantee-reliant models.

Capital adequacy remains a pillar of "disciplined management." The consolidated capital adequacy ratio stood at 10.74%, while the Own Capital Ratio was 2.2%. These figures provide a sound buffer as the bank pursues higher-yielding risk-diversified assets.

4. Strategic Roadmap: Reorganization and FY2027 Outlook

In February 2026, Rakuten Bank and Rakuten Group re-commenced discussions regarding a reorganization of the FinTech Business. The goal is to form an "integrated FinTech company" by bringing banking, card, and securities operations under one management structure to accelerate decision-making and AI utilization.

However, one must note the cautious nature of these discussions. The Memorandum of Understanding (MOU) sets a target implementation of October 2026, but the participation of Mizuho Bank and Mizuho Securities—who hold 14.99% of Rakuten Card and 49.00% of Rakuten Securities, respectively—remains "undecided." The plan is also subject to rigorous supervisory licenses and could be modified or discontinued.

These forecasts are built on conservative assumptions, including a 0.75% policy rate (with no further hikes incorporated) and a conservative deposit beta estimate, accounting for increased depositor interest rate sensitivity.

5. Shareholder Information and Dividend Policy

Rakuten Bank remains in a "business growth phase." Management maintains that reinvesting 100% of earnings into the expansion of the middle-risk asset portfolio and high-tech infrastructure is the most effective way to drive long-term shareholder value.

Consequently, the bank has declared no dividend payments for the current fiscal year and forecasts no dividends for the fiscal year ending March 31, 2027. This strategy prioritizes the "So What?" of corporate value: by retaining capital, the bank funds the scale necessary to dominate the digital banking market, aiming for a long-term rise in stock price over immediate cash yield.

Rakuten Bank enters the 2027 fiscal year as a highly efficient institution, successfully navigating the return of interest rates to Japan while leveraging the nation's premier digital ecosystem for sustainable growth.