Japan’s Financial Landscape in Transition: Market Restructuring and the Dynamics of Monetary Normalization

The Japanese financial ecosystem is currently navigating a profound structural realignment, driven by a pincer movement of regulatory and monetary shifts: the conclusion of the Tokyo Stock Exchange (TSE) transitional measures and the Bank of Japan’s (BoJ) move toward interest rate normalization. For nearly a decade, the market operated under artificial "transitional" protections for corporate listings and "abnormal" negative interest rate policies. As these temporary regimes expire, the structural boundaries of the Japanese capital market are being aggressively redefined. For global institutional investors, understanding the synergy between these forces is the prerequisite for navigating a regime where capital is finally being priced by risk rather than policy.

This transition is defined by three converging structural themes:

- The Finality of Listing Standards: The terminal phase of the TSE’s 2022 market restructuring, where firms must validate their "Prime" or "Standard" status through rigorous governance and liquidity benchmarks.

- The Endogeneity of Deposit Generation: A fundamental shift in the macro-supply of liquidity, moving from government-led expansion (QE) toward a competitive, credit-driven "Redistribution Structure."

- Heightened Interest Rate Sensitivity: A behavioral evolution where the "stickiness" of funding is tested as depositors move between institutions and asset classes in search of yield.

The following analysis provides a strategic roadmap of this new paradigm: Section I examines the "moment of truth" for corporate governance via the 2026 delisting deadline; Section II analyzes the macro-micro dichotomy of deposit competition; and Section III evaluates the evolving sensitivity of depositors in a positive-rate environment. Ultimately, the rigor of these new listing standards and the normalization of funding costs will serve as the primary catalysts for a more efficient, disciplined capital-allocation environment.

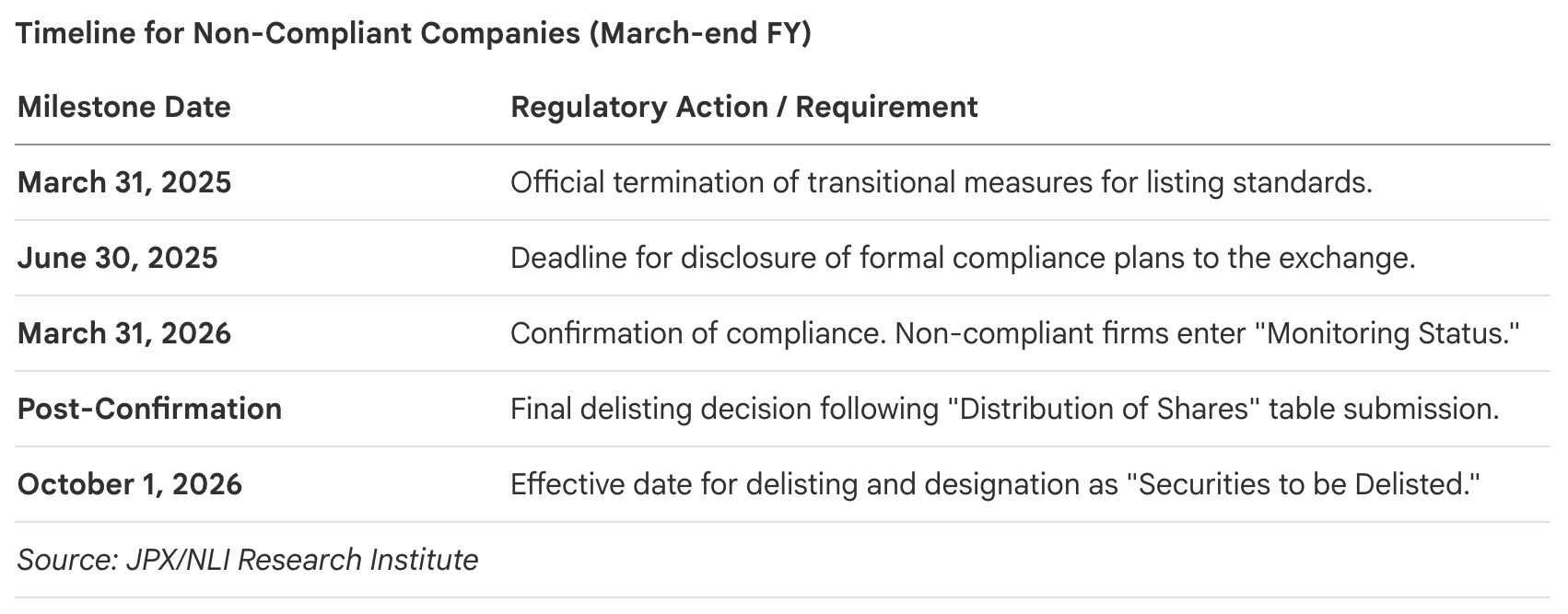

1. The Final Stage of TSE Market Restructuring and Listing Standard Compliance

The TSE’s 2022 market restructuring was a strategic attempt to rectify the diluted value of Japanese listings and harmonize segments with global institutional requirements. However, the initial impact was mitigated by "transitional measures" that shielded non-compliant firms. The expiration of these measures in the 2025–2026 period represents a terminal "moment of truth" for Japanese corporate governance. For the strategist, this signifies the end of the "grace period" and the beginning of a market where listing status must be earned through sustained enterprise value and market liquidity.

For companies with fiscal years ending in March, the regulatory path to the 2026 delisting effective date is now fixed:

Analysis of the 549 companies originally granted transitional measures reveals a significant bifurcation of outcomes. Approximately 50% have successfully achieved compliance. However, nearly 30% recognized the impracticality of their initial tiering and downgraded market segments—primarily from "Prime" to "Standard"—to better align with their scale and liquidity. Notably, over 10% delisted entirely, frequently through Management Buyouts (MBOs) or stock swaps, effectively exiting the public market rather than meeting the heightened rigor of the new standards.

This reshuffling has fundamentally reconfigured market composition. In a significant structural shift, the "Standard" market now exceeds the "Prime" market in total listed entities. This reflects a more accurate categorization of the Japanese corporate sector, where the "Prime" designation is increasingly reserved for the vanguard capable of meeting global governance expectations. This structural discipline in equity markets mirrors the similarly rigorous evolution in the banking sector’s primary funding mechanism: the deposit base.

2. Structural Shifts in Deposit Competition and the Macro-Micro Dichotomy

The pivot from "Abnormal" negative rate policies to a normalized interest rate environment has fundamentally revalued bank liabilities. Under the previous regime, deposits were often perceived as a cost burden due to the expense of maintaining excess reserves. Post-normalization, rising policy rates and interest on reserves have restored the status of deposits as a strategic revenue source. However, this recovery is occurring within a "Competitive Redistribution Structure" that favors active credit creation over passive liquidity.

The Yen settlement system operates as a "closed loop." Macro deposits do not increase because of household "savings" behavior; rather, a household purchasing stocks merely transfers funds from their account to the seller’s account within the banking system. The total pool only expands when the system increases its balance sheet via lending or government spending.

The Shift in Funding Structure

During the QE era, Japan operated under an "Expansionary Structure," where massive government debt (G) was the primary engine of deposit growth. Today, we are witnessing the decline of the Net Residual Rate of Government Debt, which represents the portion of fiscal spending that remains as private-sector deposits after taxes and debt drainage. As the fiscal contribution to liquidity weakens, individual bank growth becomes a zero-sum game.

As government-led liquidity recedes, a bank's ability to maintain its deposit base is now entirely dependent on its own Credit Creation or its capacity to capture existing stock from competitors. This structural shift forces banks to move from passive deposit acceptance to aggressive, competitive strategies to manage their funding costs and balance sheet expansion.

3. The Evolution of Interest Rate Sensitivity and Deposit Retention

As interest rates rise, Asset-Liability Management (ALM) must grapple with the shifting "Interest Rate Sensitivity" of depositors. The stability of Core Deposits—traditionally the bedrock of Japanese banking—is being tested for the first time in decades, posing a significant challenge to Interest Rate Risk in the Banking Book (IRRBB) management.

Dimensions of Deposit Shifts

The "stickiness" of funding is currently experiencing two distinct pressures:

- In-Bank Shift: The movement from ordinary (liquid) deposits to time deposits. During the easing era, the time-deposit ratio dropped at an annual rate of 1.64%. Post-normalization, the recovery is merely 0.66% annually. This asymmetric and suppressed recovery indicates that many depositors still prioritize the "Liquidity Option" over modest yield gains.

- Out-of-Bank Shift: Inter-bank movement has seen a marked increase in variance. Depositors are increasingly seeking better rates or superior digital convenience, causing a redistribution of liquidity away from regional sectors.

Winners and Losers in the Redistribution

Data identifies clear "Outliers" in the current environment. "Other Banks" (internet-only banks) and metropolitan hubs like Tokyo and Kyoto are seeing significantly higher rates of time-deposit migration and fund inflows. Conversely, regional "satellites" and credit unions face stagnant or declining liquidity as funds migrate toward institutions offering higher digital utility or better rates.

Functional Unbundling via NISA

The structural bifurcation of the deposit function is now an undeniable reality. Historically, deposits served settlement, liquidity, and investment functions. Today, the "Investment" function is being externalized to capital markets, accelerated by the expansion of the NISA (tax-exempt savings) system and rising equity prices. Consequently, bank deposits are increasingly being utilized purely for Settlement and Liquidity Options, forcing banks to compete on convenience rather than just interest margins.

This zero-sum environment requires banks to adopt aggressive interest rate strategies and enhanced digital value propositions. If a bank fails to provide a compelling reason for retention, funds will migrate either to internet competitors or directly into the capital markets.

4. Synthesizing the New Financial Paradigm

Japan has definitively transitioned from a regime of macro-liquidity expansion to one defined by micro-level competition and structural discipline. The conclusion of transitional listing measures and the normalization of interest rates are inextricably linked: both represent the removal of the policy "safety nets" that previously obscured corporate and financial inefficiency.

Strategic Imperatives for Stakeholders

- For Corporations: The era of listing "grace periods" is over. Sustained market presence now requires a proactive commitment to governance and liquidity that meets global institutional standards.

- For Financial Institutions: Funding stability is no longer an entitlement. In a zero-sum environment, ALM strategies must account for higher sensitivity, and banks must actively manage credit creation to capture a share of a finite liquidity pool.

- For Investors: Market structure is bifurcating. A clear gap has emerged between high-sensitivity "hubs" (metropolitan and internet banks) and lower-sensitivity regional "satellites." The former are better positioned to maintain funding stickiness through digital dominance.

These structures remain dynamic. While current depositor sensitivity appears suppressed by a long-standing preference for liquidity, these dynamics will shift further if real interest rates move deeper into positive territory or if asset price volatility triggers a massive re-evaluation of the investment function of the traditional bank account.