Japan Government Bond Market Trends and Liquidity Report

The Bank of Japan’s Financial Markets Department provided a comprehensive analysis of government bond market trends and monetary adjustments for the 24th "Bond Market Participants Meeting."

The materials detail the ongoing reduction in long-term Japanese Government Bond (JGB) purchases, showing a planned decline in monthly offer amounts across various maturities, and illustrate the impact of these policies on market liquidity, yield curves, and the central bank's balance sheet composition.

Additionally, the analysis includes results from a Bond Market Survey that captures participant sentiment regarding market functionality and future interest rate expectations. Feedback from financial institutions highlights a general consensus on maintaining predictable reduction plans while monitoring supply and demand stability.

Ultimately, the reports serve as a technical evaluation of the transition toward market-driven interest rate formation and reduced central bank intervention.

1. Introduction: The Context of Monetary Policy Transition

The Bank of Japan's planned June 2026 intermediate evaluation of its JGB purchases marks a well-communicated decision point in its multi-year normalization trajectory. This review serves a dual mandate as defined in the June 2025 policy framework: first, a performance audit of the current reduction plan through March 2027; and second, the establishment of a strategic "tapering floor" for April 2027 onwards. As the Bank seeks to transition from active yield curve management to a more neutral balance sheet, the primary challenge remains the calibrated withdrawal of central bank liquidity without overtaxing the private sector's absorption capacity. This process is inherently data-dependent, utilizing market functionality metrics as the ultimate feedback loop to ensure that the reduction of the BoJ’s footprint does not compromise the "backstop liquidity" required for a stable financial system.

2. Intermediate Evaluation: Performance of the Current Reduction Plan

The initial phase of the BoJ’s tapering strategy has focused on institutionalizing predictability to mitigate duration shocks. Market participants have broadly validated this approach, with the current rhythmic reduction seen as a necessary precursor to genuine price discovery.

- The Consensus for Stability: An overwhelming majority of market participants advocate for "no correction" to the existing plan through March 2027. The prevailing view is that the current scale of reduction is well-digested, and maintaining a predictable "footprint" is vital for ensuring stability as interest rate expectations drift higher.

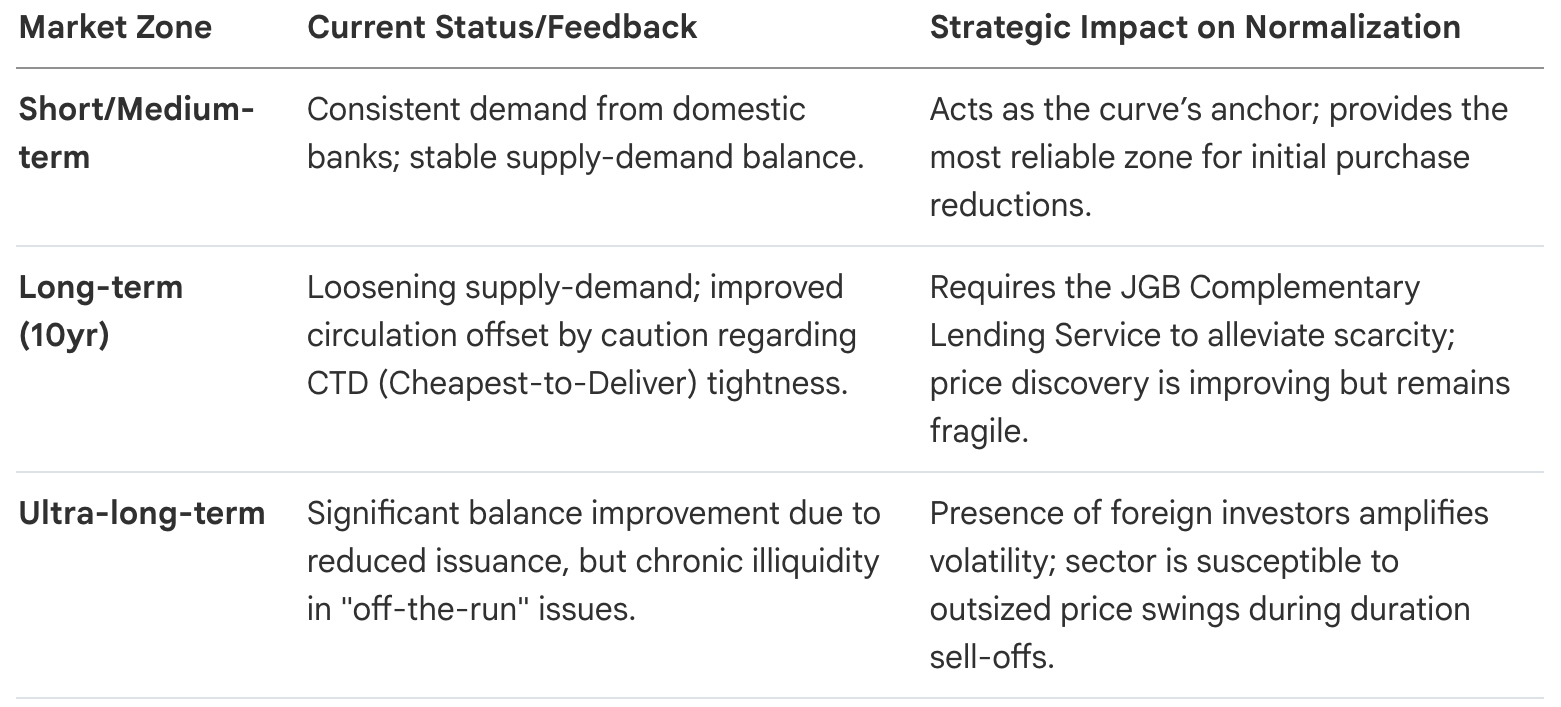

- The "Acceleration" Perspective and the Stock Effect: A minority of professionals propose increasing the reduction pace to 400 billion JPY per quarter. This cohort argues that the "stock effect"—the persistent distortion caused by the Bank’s massive total holdings—remains the primary inhibitor of market recovery. These participants contend that until the BoJ’s holding ratio is significantly lowered, yield formation will remain artificial, particularly in "off-the-run" segments and specific curve zones where ownership is highly concentrated.

- Operational Footprint: While the tapering has been smooth, the Bank continues to maintain a strategic footprint to ensure backstop liquidity. While flow is being reduced, the high stock of JGBs on the BoJ balance sheet continues to create technical distortions, limiting the speed at which market mechanisms can fully normalize.

3. Market Liquidity and Functionality Analysis

Liquidity metrics serve as the primary diagnostic tool for assessing the health of the JGB market during this transition. Current data suggests a "bottoming out" of market pessimism. While the current Diffusion Index (DI) for functionality remains negative at -16 (an improvement from February's -26), the more revealing metric is the "Change from 3 months ago" DI, which swung from -13 to +12. This massive sentiment reversal signals that participants believe the worst of the liquidity drought has passed, even if functionality is not yet "high."

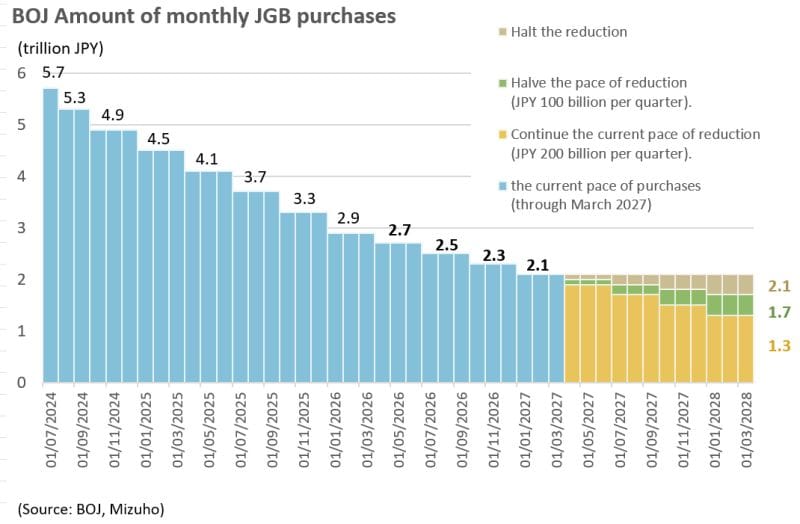

4. Post-March 2027 Strategies: Defining the Tapering Floor

The focus for April 2027 and beyond is the definition of the balance sheet’s terminal size. The current plan reaches a purchase level of approximately 2.1 trillion JPY per month by March 2027, sparking a debate over whether this represents a "neutral" floor or merely a waypoint toward deeper normalization.

- Maintenance at 2.1 Trillion JPY (Neutrality): Proponents argue this "pre-QQE" level avoids distorting yield formation while ensuring the Bank can still intervene if market stress emerges. Staying here limits the "duration supply shock" to domestic banks.

- Gradual Continuation (Toward 1.7T or 1.3T JPY): This path targets 1.3 trillion JPY (the pre-Lehman benchmark). This is the more aggressive normalization target, aimed at a full restoration of market forces over a multi-year horizon.

- Complete Normalization: A "zero purchase" objective is favored by a small minority who prioritize functionality over all else, contingent on institutionalized functionality checks.

Institutional Context: The pace of this tapering is intrinsically linked to IRRBB (Interest Rate Risk in the Banking Book) constraints. Domestic banks are the natural buyers to replace the BoJ, but if the taper is too aggressive, the resulting duration supply could exceed these banks' risk limits, leading to a disorderly yield spike and capital ratio pressure.

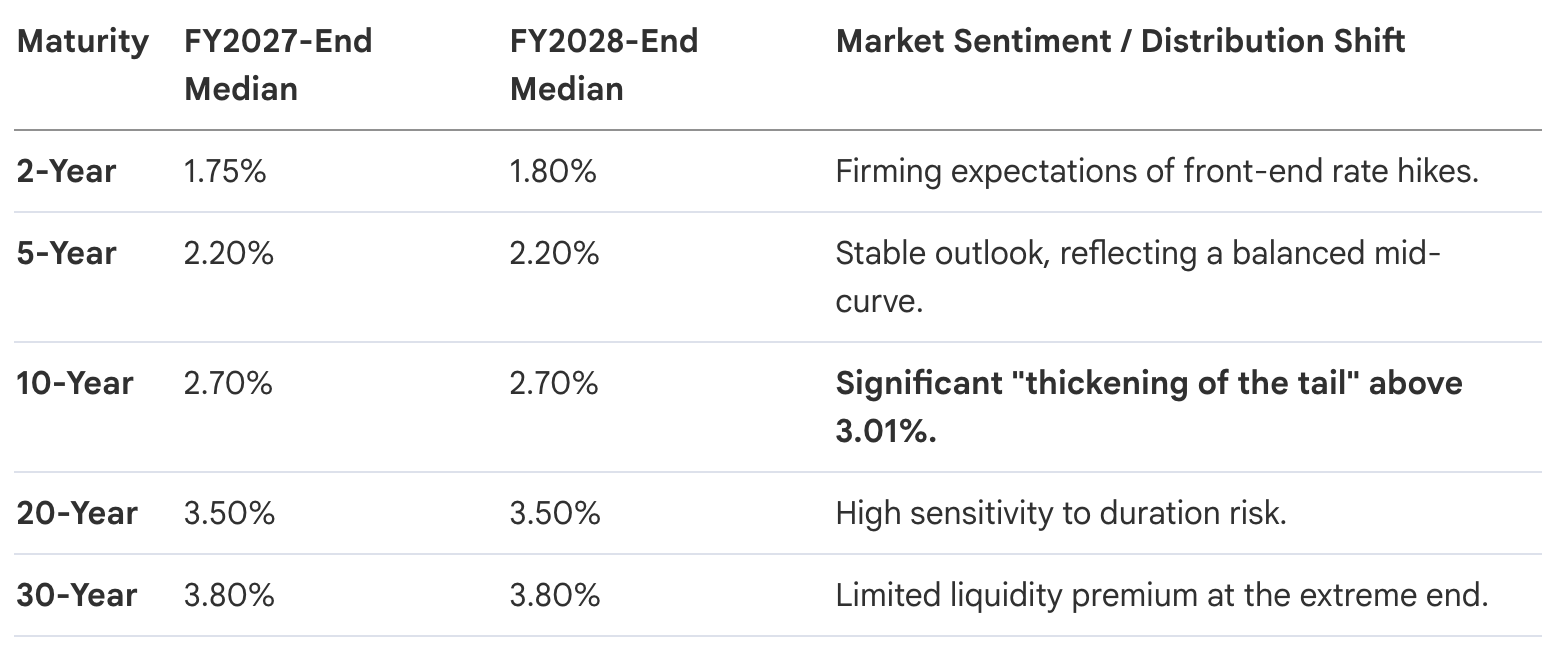

5. Interest Rate Trajectories and Yield Curve Projections (2026–2028)

As the Bank reduces its JGB purchases, market pricing has shifted upward, reflecting expectations of a more aggressive rate hike cycle. External volatility—including Middle East tensions and persistent oil-driven inflation—has served as a catalyst for these revisions.

The "Tail Risk" Analysis: While the median 10-year yield is projected at 2.70%, the probability distribution shift between the February and May surveys is profound. There is a marked increase in the perceived risk of a breach above the 3.0% threshold by the end of FY2027. This "thickening tail" suggests the market is pricing in a higher probability of an inflationary overshoot or a more rapid withdrawal of central bank support.

6. The Stability vs. Normalization Trade-off: Strategic Recommendations

The path forward necessitates a transition from rigid tapering to a more sophisticated, operational approach. To maintain market confidence during this normalization, the Bank should adopt three Strategic Pillars:

- Operational Flexibility: The Bank must maintain the capacity for "temporary operations" or emergency liquidity injections. This ensures that while the trend is toward reduction, the Bank remains an effective lender/buyer of last resort during periods of disorderly volatility.

- Predictable Operational Refinement: Beyond merely prioritizing reductions in high-ownership zones, the Bank should explore merging or changing maturity segments and adjusting purchase frequency as the monthly purchase volume drops. This prevents individual auction sizes from becoming too small to be meaningful, thereby preserving market "depth."

- Communication Transparency: Clarifying the long-term balance sheet target is essential to anchor expectations. Explicitly distinguishing between the 2.1 trillion JPY "neutrality" level and the 1.3 trillion JPY "full normalization" level will allow financial institutions to calibrate their duration risk appetite more effectively.

Market sentiment has shifted from apprehension to a cautious endorsement of normalization. Provided the BoJ remains data-dependent and prioritizes operational predictability over absolute speed, the JGB market appears capable of absorbing the transition toward a more neutral monetary footprint.