Japan’s Great Crypto Migration: Crypto Asset Regulation Shifts to the Financial Instruments and Exchange Act

2026 legislative reforms will transition the oversight of crypto-assets from the Payment Services Act to the Financial Instruments and Exchange Act (FIEA). By categorizing crypto-assets as investment products rather than simple payment methods, the government aims to strengthen investor protection and market integrity. The transition introduces rigorous disclosure requirements for issuers, mandatory registration for trading services, and a comprehensive framework to combat insider trading and market manipulation. Additionally, the new laws mandate audited financial reporting and the strict segregation of customer assets to prevent financial loss. These changes essentially align the digital asset regulatory landscape with the high standards applied to traditional securities. This shift represents a significant evolution in Japan’s approach to fintech governance and financial stability.

1. Overview of the Regulatory Reform and Rationale

Following the December 10, 2025, report by the "Working Group on Crypto Asset Systems," the Cabinet approved a landmark Amendment Bill on April 10, 2026. Market participants should brace for the wholesale migration of crypto asset regulations from the Payment Services Act (PSA) to the Financial Instruments and Exchange Act (FIEA).

The rationale provided by the Financial Services Agency (FSA) is clear: the FIEA is a "cross-sectional investor protection law." While the 2025 Amendment to the PSA (Act No. 66 of 2025) laid early groundwork, regulators now acknowledge that the vast majority of crypto transactions are driven by capital gains rather than "payment" utility. By shifting to the FIEA, Japan acknowledges the "investment nature" of crypto. However, a critical legal distinction remains: unlike traditional securities, crypto assets generally do not represent legal rights to dividends or residual assets, necessitating their status as a unique regulated class within the FIEA framework.

The Bill submitted to the 221st Diet rests on four pillars, including corporate sustainability disclosures and startup funding. However, for the digital asset industry, the "Review of Regulations Related to Crypto Assets" is the undisputed centerpiece, redefining everything from issuer liability to market conduct.

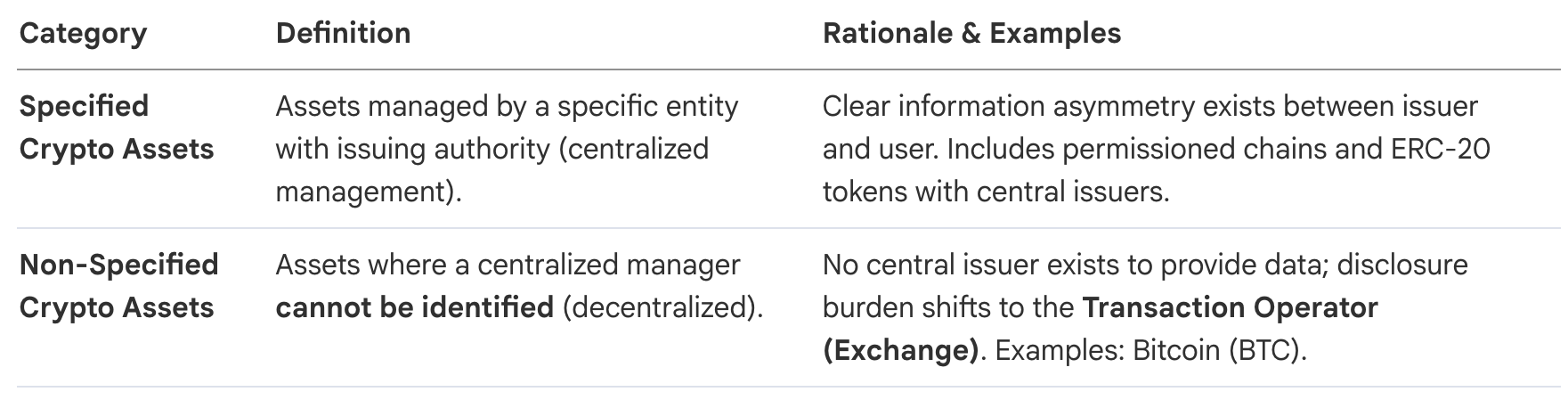

2. The New Information Disclosure Framework

To mitigate the inherent information asymmetry in digital markets, the reform introduces a tiered disclosure system that places the burden of transparency on whichever entity holds the most information.

"Specified Crypto Asset Issuers" are now subject to rigorous, securities-like requirements:

- Primary Disclosures: Issuers are prohibited from solicitation or sale until "Specified Crypto Asset Information" is publicly disclosed via Cabinet Office Ordinances.

- Continuous Reporting: Issuers must file "Periodic Information" (comparable to annual securities reports) within three months of the fiscal year-end, alongside "Extraordinary Information" for material technical or corporate events.

- Audit Requirements: Financial statements must be certified by a CPA or audit firm. Notably, the reform adopts the "Stock-type Crowdfunding" framework for exemptions: solicitations under 500,000 yen per investor or a 2 million yen annual total may waive the audit requirement.

Exchanges face new duties for Initial Exchange Offerings (IEOs) and "Unauthorized" listings (listings without issuer involvement, or Katte-jojo). For the latter, the operator assumes the primary duty to provide "Crypto Asset Information" regarding the asset's functions, supply, and technical risks.

The reform introduces a severe liability framework for false information, specifically designed to protect the "private law" rights of investors:

- Violation of Pre-disclosure Solicitation: No-fault (Absolute) liability for the violator.

- False Primary Disclosure (Issuers): No-fault liability regarding false information.

- False Primary Disclosure (Officers/Auditors): Negligence liability with a shifted burden of proof—directors must prove they were not negligent to avoid liability.

- False Periodic/Continuous Disclosure (Issuers): Negligence liability with a shifted burden of proof.

- False Periodic/Continuous Disclosure (Officers/Auditors): Negligence liability with a shifted burden of proof.

3. Expansion of Business Regulations for Operators

The scope of "Crypto Asset Transaction Business" has expanded to eight distinct types. Crucially, the reform now includes "Crypto Asset Borrowing" as a regulated activity, closing a significant previous loophole.

The "Last Bastion" of user protection is reinforced through mandatory safeguards:

- Trust-Based Segregation: Customer money must be managed separately from the operator's assets via Trust Companies (信託会社), a significantly higher bar than simple separate bank accounts.

- Cold Wallet Mandate: Operators must manage customer crypto assets offline. "Hot Wallets" are strictly limited to 5% of customer holdings.

- Fulfillment Guarantee Crypto Assets: For assets held in hot wallets, operators must maintain a reserve of "same type and same amount" (同種・同量) of their own crypto assets. These "Fulfillment Guarantee Crypto Assets" ensure immediate liquidity and user compensation.

Aligning with traditional finance, operators must now calculate a Capital Adequacy Ratio and establish Financial Instruments Business Liability Reserves based on transaction volume to cover potential security breaches or operational failures.

4. Comprehensive Unfair Trade and Insider Trading Regulations

Regulation now applies to three classes of parties possessing "Material Facts":

- Specified Issuer-Related Parties: Officers, employees, and major shareholders.

- Transaction Operator-Related Parties: Exchange employees with knowledge of impending listings or delistings (Katte-jojo).

- Major Buyers (Massive Traders): Parties planning transactions involving 20% or more of issued assets (a projected threshold to be finalized by Cabinet Order).

Material facts include technical specification changes, service disruptions, security breaches (unauthorized transfers), and corporate alliances.

Market Integrity Prohibitions

- Market Manipulation: Direct prohibitions on "pegging" or "fixing" prices to stabilize or manipulate the market.

- Stealth Marketing: Any party receiving compensation for expressing trade opinions must disclose the relationship. An exception exists for professional advertisers/broadcasters where the content is clearly identified as an advertisement (広告として表示する場合).

- The Private Law Effect: Contracts for "Unpublished Crypto Assets" made by unregistered operators are legally void. The burden is on the operator to prove the transaction was not "prejudicial to customer protection" to uphold the contract.

5. New Regulated Entities and Specialized Roles

A new "Crypto Asset Management Related Business" category governs third-party wallet and system providers. These entities now face notification duties and strict safety management standards to mitigate systemic risk.

The reform extends "Investment Management" and "Investment Advisory/Agency" scopes to include "Spot" (Physical) Crypto Assets. This is a major win for traditional firms, allowing them to enter the space without the legal ambiguity of the PSA era.

Crypto brokerage is now integrated into the "Financial Instruments Mediation Business," replacing the "Electronic Payment Instruments/Crypto Asset Service Brokerage" previously managed under the PSA.

6. Implementation Timeline and Transitional Measures

While the expected enforcement date is in 2027 (within one year of promulgation), existing operators face an immediate "compliance sprint."

- 2-Week Notification: Within two weeks of enforcement, existing operators must notify the regulator of their trade name, address, capital amount, and names of officers.

- 3-Month Information Deadline: The duty to provide "Crypto Asset Information" for all existing handled assets must be met within three months of enforcement—a massive operational hurdle.

- Registration Grace Period: Operators registered under the old PSA have a 6-month window to apply for the new FIEA registration or change. While the maximum grace period for "deemed" status is 2 years, the application must be filed within the first six months to remain compliant.

7. Concluding Summary of Market Impact

This reform marks the definitive "Institutionalization" of the Japanese crypto market. While the transition from the PSA to the FIEA creates a high "compliance moat" due to increased costs for reserves, audits, and management systems, it simultaneously provides the institutional legitimacy required for mass adoption by professional investors.

The industry has moved past the era of "payment experiments" into a regime of rigorous capital market oversight. However, a note of caution for participants: many technical standards—including exact thresholds for "Material Facts" and hot wallet protocols—remain pending through future Cabinet Office Ordinances and supervisory guidelines. The "New Normal" is here, but its final granularity is still being etched by the regulator.