Misconduct at Sony Financial Group

Sony Financial Group and its subsidiary, Sony Life Insurance, have disclosed financial misconduct involving an insurance agent and approximately 30 customer complaints regarding inappropriate activity. In response to these incidents, the company has decided to abolish its exclusive agency system and transition existing branches to general agencies. Sony Life is currently performing a comprehensive review of all customer contracts and expects to release a progress report by the end of May 2026. To prevent future fraud, the firm is enhancing internal controls, strengthening identity verification, and implementing a team-based "Joint Maintenance" system for client oversight. Consequently, the Financial Services Agency has issued an official order requiring the company to submit detailed reports on these issues and their remediation efforts. While the full financial impact remains undetermined, Sony Life is prioritizing customer protection and organizational transparency to regain public trust.

1. Contextual Framework and Regulatory Mandate

The order issued by the Financial Services Agency (FSA) under Article 128, Paragraph 1 of the Insurance Business Act requires a rigorous accounting of Sony Life's initiatives regarding identified misconduct and the ongoing review of customer policy status. As the institution navigates this regulatory intersection, it needs to build a critical bridge between the forensic identification of systemic vulnerabilities and the systematic restoration of institutional trust.

The scale of the challenge necessitates a comprehensive internal response, driven by the following factors:

- Confirmed Misconduct: Validated instances of financial impropriety involving an agent previously affiliated with "Premier Agency," a former exclusive agency.

- Customer Grievances: Approximately 30 independent reports from customers alleging inappropriate conduct specifically related to financial matters and fund handling.

- Universal Scope of Review: Following industry-wide scrutiny, a mandatory review has been initiated covering all contracts and financial matters involving customers for whom both exclusive agencies and direct employees are responsible.

- Systemic Transition: The strategic decision to entirely abolish the "exclusive agency system"—originally established in 2007—to mitigate persistent control-related challenges and transition toward a general agency model.

These external pressures have catalyzed a transformation of the internal structural framework to ensure long-term resilience and transparency.

2. The Three-Line Management Structure

The cornerstone of Sony Life's recovery is the "three-line management structure," a design intended to decentralize risk ownership while maintaining an uncompromising centralized oversight mechanism. This architecture ensures that while risk is managed at the point of sale, it remains visible and accountable to the highest levels of corporate governance.

Sony Life has redefined the roles of leadership to establish clear accountability across the following entities:

- Branch Managers as Risk Owners: As the heads of sales offices, Branch Managers are designated as the primary "risk owners," responsible for the direct execution and maintenance of internal controls within their local jurisdictions.

- Management Headquarters: Situated within the Sales Headquarters of the head office, this entity provides centralized governance and is led by a dedicated Management Headquarters Director.

- Regional Headquarters System: This system provides a granular layer of oversight that allows for the detailed management of branches, ensuring that localized office dynamics are integrated into the broader corporate compliance framework.

The Regional Headquarters System effectively neutralizes the risk of local isolation, standardizes operational rigor across diverse geographies, and interrogates branch-level dynamics to prevent the formation of opaque management silos. This hierarchy provides the structural foundation for the specialized personnel deployed to enforce these rigorous standards.

3. The Role of Field Compliance Officers

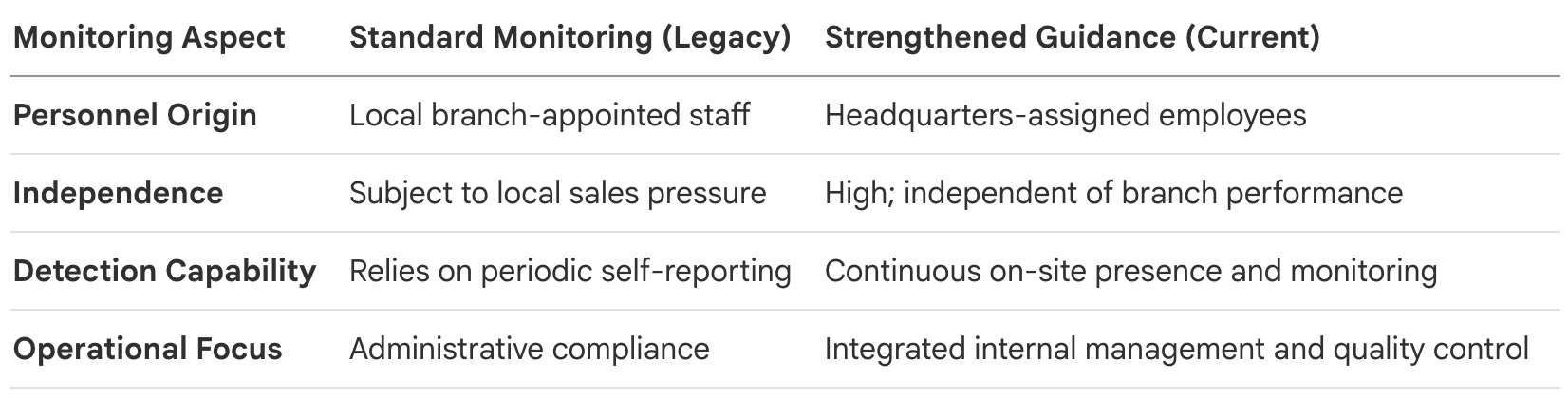

On-site monitoring is a necessity for the early detection of fraudulent patterns that often evade remote technical audits. By embedding compliance expertise directly within sales environments, Sony Life shifts from a reactive posture to a proactive, surveillance-oriented defense.

The deployment of "Headquarters Employees"—specifically compliance officers and quality control personnel—to branch offices and agency locations nationwide represents a significant shift in reporting lines. By utilizing staff who report directly to the Management Headquarters rather than local sales management, Sony Life eliminates the inherent conflict of interest in local self-reporting.

This human-centric oversight is augmented by technical safeguards designed to eliminate the manual opportunities for financial exploitation.

4. Digital Transformation and Verification Protocols

Shifting from manual to digital processes is a strategic imperative in the life insurance sector to eradicate "closed-door" vulnerabilities. Digital protocols create immutable audit trails and remove the opportunities for unauthorized alterations that historically plagued paper-based systems.

Since FY2017, Sony Life has mandated the following technical protocols:

- Paperless Mandate: Application procedures are strictly limited to dedicated sales terminals.

- Discontinuation of Paper Forms: Traditional paper application forms have been entirely abolished to prevent unauthorized data manipulation.

- Mandatory Audit Trails: Digital logs now capture every stage of the application lifecycle.

- Post-Application Cancellation Protocol: If a customer elects to cancel a policy after application, a physical signature is strictly required to provide a verifiable audit trail of the customer’s direct intent.

The impact of these technical controls is most evident in disbursement procedures. By prohibiting the designation of third-party accounts, strengthening identity verification, and lowering policy loan maximums, Sony Life has fundamentally reduced its risk profile. These safeguards ensure that the technical infrastructure prevents the execution of fraudulent transfers even in the event of ethical lapses by personnel.

5. Recruitment and Compensation Reform

Institutional risk is intrinsically linked to the incentives and quality of sales personnel. To mitigate this, Sony Life has overhauled its human capital strategy, shifting the focus from pure sales volume to "recruitment quality" and long-term integrity.

The multi-stage screening process for all candidates now includes:

- [x] Rigorous Loan Status Verification: Comprehensive financial background checks prior to hiring.

- [x] Third-Party History Validation: Independent verification of all employment history declarations.

- [x] Specialized Head Office Interviews: Mandatory screening by specialized head office interviewers for all candidates to ensure alignment with corporate values.

Compensation systems for sales personnel and managers have been revised to incorporate "internal management status" as a core performance metric. To align agent aptitude with organizational safety, Sony Life has introduced multiple career paths, including transfers between systems from sales personnel to head office employees, conversion to fixed-salary roles, or transfers to specialized "Consulting Follow" branches.

6. Organizational Culture and Ethical Governance

A "risk-aware culture" serves as the final layer of defense, preventing misconduct that might otherwise evade formal controls. The governance strategy focuses on embedding ethical standards into the professional identity of every employee and director.

The governance impact is reinforced through several high-level measures:

- Independent Oversight: The appointment of outside directors with specialized expertise in compliance ensures objective governance at the board level.

- Punitive Deterrence: Employee work rules have been explicitly revised to prohibit any exchange of money between customers and employees. Sony Life has mandated strict disciplinary action for any violation of this rule, serving as a powerful deterrent.

- Educational Dissemination: The "Fundamental Principles of Compliance and Risk Management" booklet has been distributed to all staff, with its core tenets integrated into all training programs to ensure the principles are practiced, not just read.

These measures transition the focus toward the most critical relationship: the direct engagement between the institution and the customer.

7. Mitigating "Closed-Door" Vulnerabilities: Direct Customer Engagement

The historically opaque relationship between agents and clients is a primary vulnerability. To dismantle the information monopoly of individual agents, Sony Life has implemented tripartite transparency measures designed to empower the customer.

Key initiatives include:

- Disclosure of Authority (FY2024 onward): At the time of application, agents must explicitly explain which products and services they are authorized to offer and, crucially, which activities they are not authorized to perform.

- Joint Maintenance System: A team-based approach where multiple representatives share customer information, ensuring that no single agent maintains exclusive control over a client’s portfolio.

- Headquarters Verification Protocol: A specialized department at headquarters now contacts customers directly every three years to verify contract details and directly convey precautions regarding the handling of funds.

These protocols, combined with the shift from the exclusive agency system to a more transparent general agency model, ensure that the "closed-door" risks are effectively mitigated.

8. Conclusion: Path Toward Institutional Restoration

The effectiveness of this five-point strategy lies in its operation as an integrated ecosystem—addressing risk through architectural, specialized, technical, human, and cultural layers. This comprehensive approach demonstrates a move beyond reactive remediation toward a sustainable model of institutional integrity.

Sony Life remains dedicated to a "customer-centric" system, with a clear commitment to the ongoing review of policy status and a progress announcement scheduled for the end of May. Ultimately, the institution is guided by its fundamental mission: "To ensure our customers’ financial security and stability by providing reasonable life insurance and high-quality services." Sony Life recognizes its social responsibility to eradicate misconduct and is fully committed to restoring the trust of its customers, shareholders, and society.