Nomura Achieves Record Net Revenue on Global Expansion and Asset Management Pivot

Nomura has delivered a robust set of financial results for the fiscal year ended March 31, 2026, marking a critical step in the firm’s long-term transformation under President and Group CEO Kentaro Okuda. In a period characterized by sharp global market volatility, Nomura has managed to scale its top-line while maintaining structural profitability. These results reflect a deliberate transition from its traditional brokerage roots toward a diversified, globalized fee-based model, anchored by the formal integration of its new Banking division and the scaling of its investment management platform.

The Lead: Top-Line Performance and Net Profitability

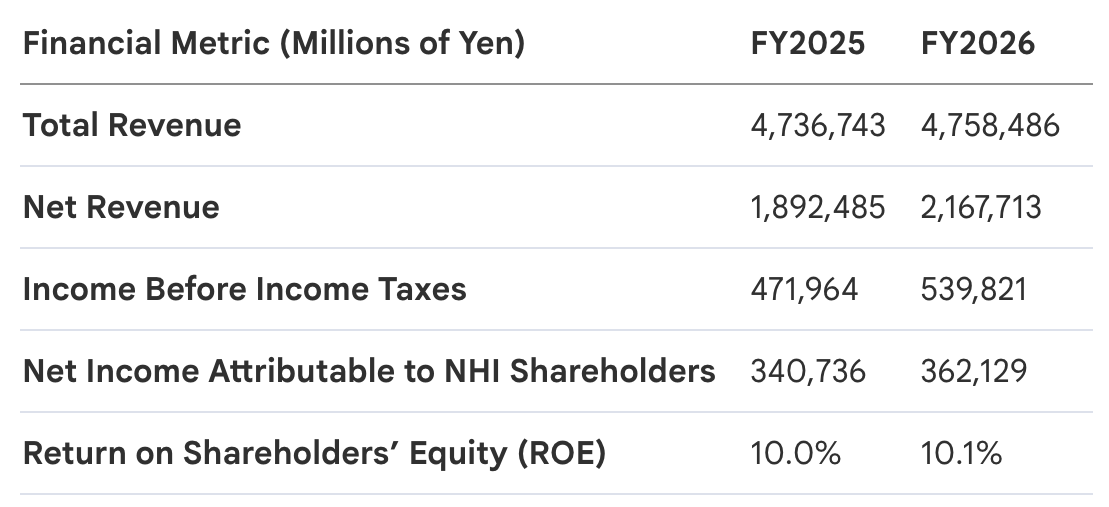

Nomura’s ability to navigate market turbulence was underpinned by a 20.1% surge in net gain on trading, which rose to 696.9 billion yen from 580.1 billion yen the previous year. This volatility capture, alongside a 23.9% jump in asset management fees, allowed the firm to record net revenue of 2,167.7 billion yen, a 14.5% increase. Crucially, the firm’s Return on Equity (ROE) edged up to 10.1%, signaling that CEO Okuda’s strategic pivots are successfully generating incremental value for shareholders.

The 6.3% rise in net income suggests a resilient capacity to convert market volume into profit, though the narrative is nuanced by rising operational costs. While Nomura is successfully capturing value from global capital markets, the firm's ability to maintain these margins as it integrates high-cost acquisitions stands out. This total group performance was fueled by distinct drivers across its specialized business segments.

Segment Analysis: Divisional Performance Differentiators

A granular look at Nomura’s divisional performance is essential this year, particularly following the April 1, 2025, establishment of the Banking division. This reorganization has reclassified revenue streams and created a more complex cost structure across the group.

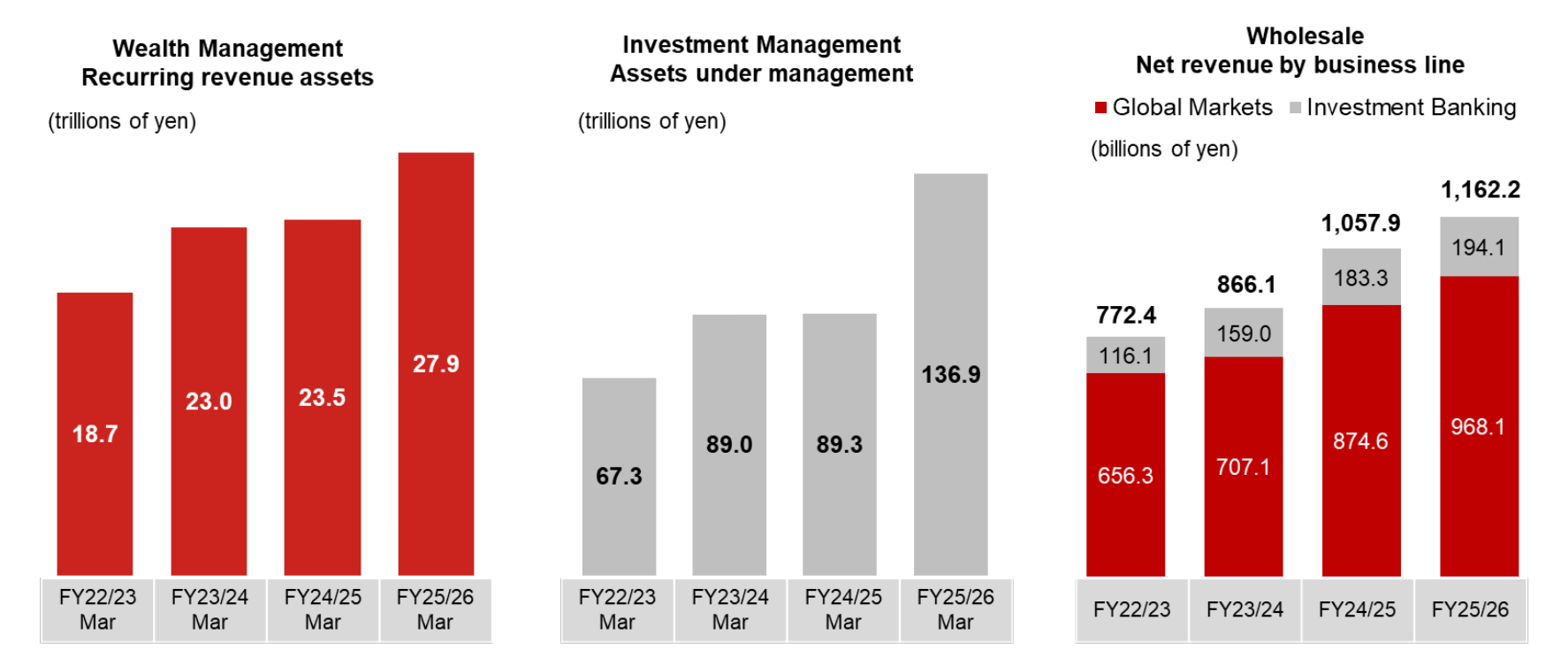

- Wealth Management: A standout performer, this segment saw pre-tax income climb 22.8% to 204.0 billion yen. Strong client engagement and asset accumulation drove net revenue up 12.5% to 487.9 billion yen, benefiting from a favorable interest rate environment and renewed retail activity.

- Investment Management: Despite a 34.3% surge in net revenue to 258.5 billion yen—bolstered by inorganic growth—pre-tax income dipped 1.4% to 88.3 billion yen. The segment suffered from severe margin compression and operating deleverage as it absorbed a 65.5% spike in non-interest expenses related to global platform expansion.

- Wholesale: This division demonstrated impressive efficiency, with pre-tax income rising 20.6% to 200.6 billion yen. Notably, the segment achieved "positive operating jaws," as net revenue grew 9.9% while non-interest expenses were held to a 7.9% increase.

- Banking: In its inaugural year, the division posted 53.9 billion yen in net revenue. However, pre-tax income fell 14.3% on a reclassified basis to 14.0 billion yen, primarily due to a 29.5% surge in non-interest expenses (totaling 39.9 billion yen) associated with the division's formal launch and infrastructure build-out.

- Other: It is vital to note that Nomura’s bottom line was significantly bolstered by a one-off 58.7 billion yen gain from the disposal of office buildings and land in Takanawa, Tokyo. This non-recurring booster provided a critical cushion for the firm’s net income targets amidst rising group-wide expenses.

Strategic M&A: The Macquarie Acquisition Impact

The centerpiece of Nomura’s inorganic strategy was the December 1, 2025, completion of the Macquarie Management Holdings acquisition. This $1.8 billion USD deal (approximately 281.4 billion yen) included equity interests in Luxembourg and Austrian holdings, instantly transforming Nomura into a global heavyweight with 136.9 trillion yen in Assets Under Management (AUM).

The acquisition has left a visible mark on the consolidated balance sheet, with Nomura provisionally allocating a substantial portion of the purchase price to intangible assets and goodwill. While the transaction contributed to a 275.0 billion yen acquisition-related cash outflow, the long-term strategic play is clear: Nomura is securing a stable, fee-based revenue stream to offset the inherent volatility of its trading and brokerage arms.

Financial Stability: Balance Sheet and Cash Flow Dynamics

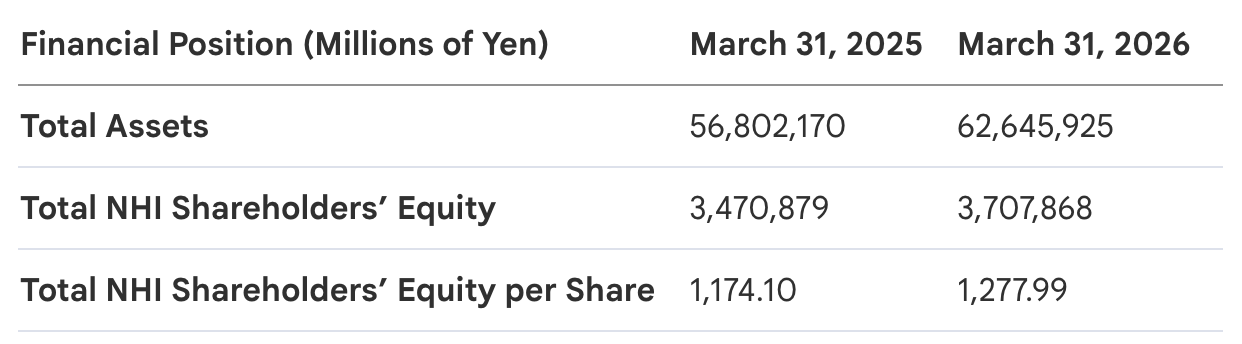

Nomura’s strategic expansion is reflected in its massive balance sheet, which hit a milestone of 62.6 trillion yen in total assets this year. Maintaining this capital base is critical as the firm increases its exposure to international markets.

The firm’s cash flow movements highlight an aggressive funding strategy. Operating activities saw an outflow of 843 billion yen, while investing activities resulted in a 1.5 trillion yen outflow, largely due to non-trading loan originations and the Macquarie deal. These were offset by 2.1 trillion yen in financing activities, driven specifically by 4.6 trillion yen in proceeds from the issuance of long-term borrowings. This heavy reliance on debt to fund growth underscores Nomura's commitment to its global pivot, even as its equity-to-asset ratio narrowed slightly to 5.9%.

Shareholder Returns and Market Outlook

With the conclusion of its 100th-anniversary commemorative dividends in 2025, Nomura has recalibrated its payout structure. For FY2026, the firm declared an annual dividend of 51 yen (27 yen for the first half and 24 yen for the second). While this is down from the 57 yen paid in FY2025, that prior figure included a 10-yen commemorative one-off. Excluding that special payment, the ordinary dividend remains consistent with the firm’s policy of balancing growth reinvestment with shareholder yield.

The forward-looking outlook remains guarded. Nomura has declined to provide specific earnings or dividend forecasts for FY2027, citing "uncertainties" in global capital markets and shifting macroeconomic conditions.

The underlying narrative is that of a firm in deep transition. By sacrificing the short-term dividend peaks of its anniversary year to fund the Macquarie acquisition and the new Banking division, Nomura is wagering its future on structural scale. As Nomura enters FY2027, the firm has effectively doubled down on a global fee-based model, wagering that its expanded balance sheet can weather a market cycle where its traditional brokerage roots no longer offer sufficient cover.